I have been tracking NOCIL for sometime. I have read somewhere anti dumping duty was effective till 2016 and again it’s extended for another year till oct 2017.

Does anyone has latest info current status of anti dumping duty.

I have been tracking NOCIL for sometime. I have read somewhere anti dumping duty was effective till 2016 and again it’s extended for another year till oct 2017.

Does anyone has latest info current status of anti dumping duty.

this might be useful.

Hi Sandeep

Thanks for the link.

Above article is related to anti dumping duty on tyres. We should be looking about rubber chemicals.

Thanks

Chetan

http://www.dgtr.gov.in/anti-dumping-cases/rubber-chemicals-namely-tdq-px-13-originating-or-exported-european-union-and-mor

check final findings doc it mentions extention of anti dumping duty from announcement date till date not mentioned on 2 products,

check last 2 pages in doc.

Nocil Investor presentation .pdf (2.1 MB)

Company’s presentation

Fwd looking statements seems good.

Analysis done by Dr Vijay Malik http://www.drvijaymalik.com/2017/10/nocil-limited-equity-research-report-analysis.html

Hi guys, in the latest investor presentation they monetioned after expansion asset turnover will be 2x… What do you guys think will it be 2x on the new Capex of 170 cr only or will it be 2x on the total assets in which case revenue potential will be substantially higher… If anyone has any idea please share the thoughts…

According me vehicle industry is bound to grow and increasing dumping from china will put pressure on Indian government as local industries will be harmed. New brands are coming up and there are many new car vehicle launches in 2017.

Tyre makers to invest over Rs 35,000 crore in next 5 years. http://google.com/newsstand/s/CBIwm8ONmTo

This is good news for NOCIL. Holding NOCIL in core PF.

0f3fdfc4-06c4-47f3-831e-130784784665.pdf (2.1 MB)

Investor presentation for Q3. In spite of posting good results the stock got hammered today. Also, the car sale nos for January 2018 are encouraging. (Implied assumption that tyre sales must have increased too).

The company has also announced CAPEX (Phase 3 of expansion) taking the total CAPEX to ₹425 crores being funded entirely through internal accruals and the estimated Asset turnover ratio is 2X.

thanks for the update!! any idea how much yearly revenue in rupee terms after all the expansion… they keep saying asset turnover 2x however how how much is that in annual revenue terms?

Considering CAPEX of ₹425 crore we can assume a revenue of ₹900 crore once the expansion is done. The effects of expansion will kick in through Q1 2018-19 to H1 2019-20. So we can start seeing the impact of revenue next year onwards.

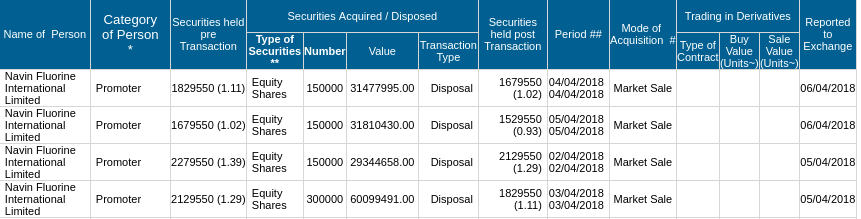

Promoters are selling the share in the open market for the last 2 months. More than 16 lakh share are sold in Jan and Feb 2018. Is it to fund the significant capex plans?

I think They are no longer promoters. Navin fluorine is selling the shares… They used to be co promoters

They are still listed as promoters in the latest shareholding https://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=500730&qtrid=96.00

Nocil has a long run way, not sure about the promoter selling. Maybe he needed some money  . Need to be watched closely.

. Need to be watched closely.

My reasons for investing in Nocil were :

Increase in number of vehicles, will lead to more demand for tyres. That way we ride the Auto sector growth via Niche player supplying to tyre industry

Electric Vehicles would need light tyres, hence would need to change more frequently as compared to other vehicles. This would be a beneficiary of EV boom as well.

Indian govt would for sure protect the interests of its Tyre industry and AD Duty is bound to be there.

Continued expansion plans are other indicator that management is expecting growth and want to be ready for demand.

Almost debt free company, available at decent valuations … to me seems like a compounding story for next few years.

Disc : Invested and views could be biased.

Some observations of different parameters from my end below:

Growth/Industry

Company

Variables

Q4 Results - Strong revenues and profits

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f6682857-a6e0-4039-9d53-0379f39fd771.pdf