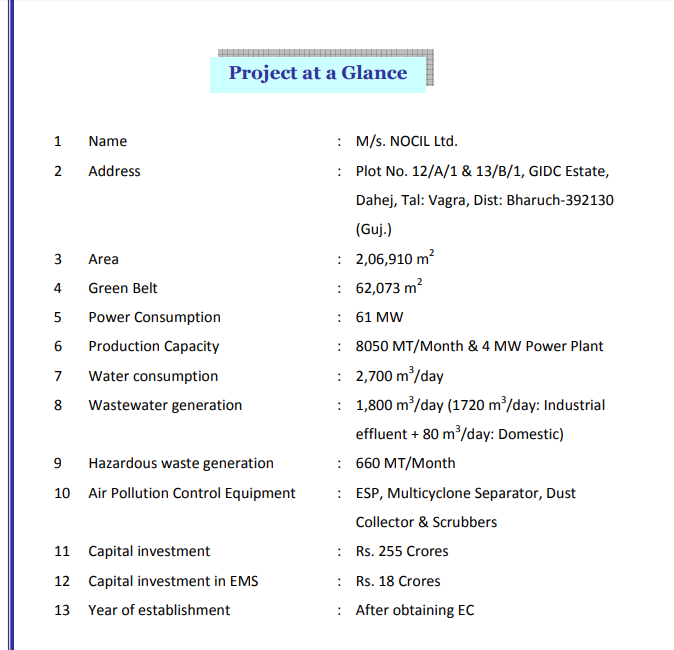

NOCIL has 2 plants : One at Dahej (10000 -15000MT per annum) and the other at Navi Mumbai (40000 MT per annum)

Dahej plant is more focussed towards manufacture intermediates which will then be transferred to its Navi Mumbai plant for converting them into finished products.

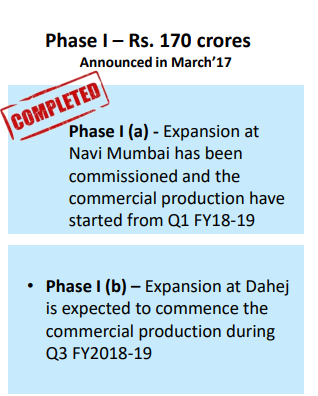

Company did a Capex of around 170 Cr recently in Navi Mumbai and some in Dahej . MOR is most probably manufactured here.

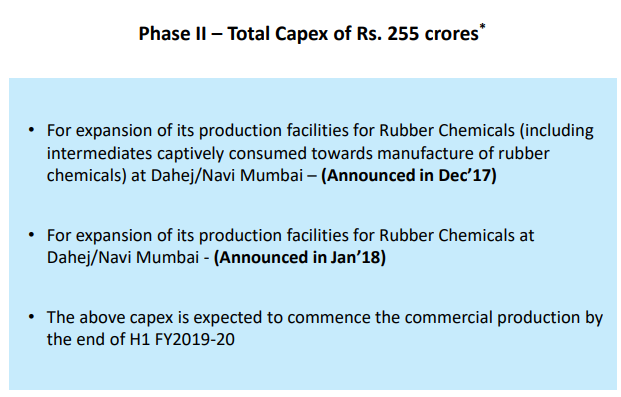

The Navi Mumbai plant has a Capacity of around 42000 MT per annum (3500 MT per Month) where it manufacture finished goods and intermediates. Another Capex of 255 Cr is proposed on this site. After Capex , the Capacity will be expanded to 97320 MT per Annum (8110 MT per Month) for this plant . Majority of Key and Final Products are manufactured here like PX13 , MBT , CBS.

One thing i am unable to understand here is that the Company while filing for Environmental clearance has shown the Dahej Land for Expansion and it showed Capacity of 40000 MT per Year at Dahej Plant while the capacity in my view is at Mumbai. Quite confusing.

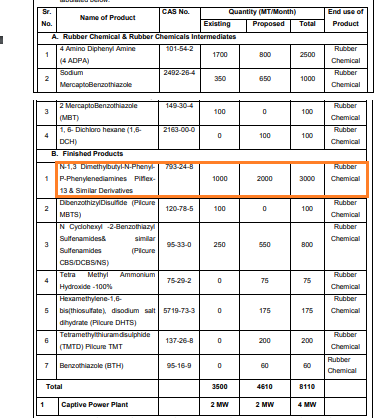

The following Products expansion will be done in this Plant.

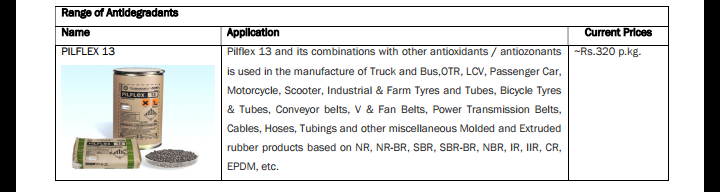

Out of the 3500 MT per Month current Capacity , around 1000 MT per Month is for PX-13 , which is around 30% of Capacity of this Plant . No doubt , it is one of the main products of the company. The management is planning to expand the capacity of PX-13 to 3000 MT per Month. It will either result in lower cost of manufacturing due to large production or can backfire if ADD is removed (Provided their cost of production remains still Higher).

It is difficult to guess what is the existing Capacity for MOR is since it is manufactured at the other site. The prices of MOR and PX-13 are almost same.

(Prices are of somewhere around Year 2016)

The rest of the other Products have prices of around 200 p.Kg on an average. The total Capacity of NOCIL is around 50000 MT out of which around 12000 MT is contributed by TX-13 which comes near 24% of total Production (My assumption is that the PX-13 is only manufactured in One plant and has a capacity of 1000 MT per Month with 100% Capacity Utilization).

Agree…If we compare with the average prices and Sales of other Products along with the capacity , the impact of PX-13 on Top line should be around 35-40% of Total Sales.

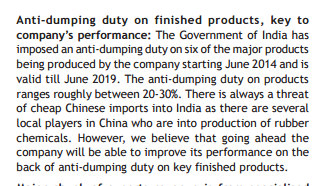

If we compare the MOR Prices , they are around Rs 315 p. Kg for dumped products after ADD (As you posted above) and NOCIL is able to sell it around 320 p. Kg at that time. so yes , Company is able to compete after ADD is in force.

For PX-13 , the Landed prices are around Rs 265 p kg while NOCIL is selling it around Rs 320 p. Kg. Difficult to understand that even after ADD , Nocil selling price was much way higher.

The difference in Data may be due to the fact that you have prices which are for Year 14-15 while prices i got is of 15-16.

The effects of ADD is around 20-30%.

I guess the client stickiness as these tire Manufacturers takes around 18 Months time to approve one’s product So it will be hard to shift suppliers very soon. May be the reason behind no criticism by these tire companies all these years despite ADD being in place from long.

Also Rupee Depreciation may make imports a little expensive and NOCIL Cost cutting measures can make them compete. I am a little Optimistic and biased towards NOCIL.

It is a genuine concern and possibility of it happening can not be denied due to the huge contribution by PX-13 to the Topline.

My Opinions :

- The DGAD while revising the ADDs will carefully watch the current impacts of the Dumping. If Domestic Industry is still at disadvantage , i believe the ADDs will surely be extended. If they find that Domestic Industry is now in a much better position , ADDs can be removed but NOCIL will be able to compete with the dumping.

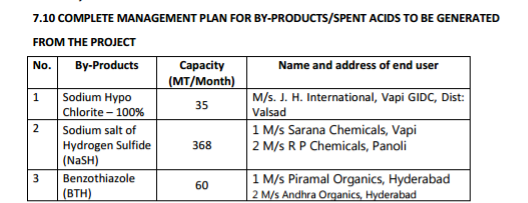

- Higher volumes of production may reduce some cost of Production. Proper disposal of By-Products may also help to some extent.

Management has hardly talked about the dumping effect from EU. Lot of dumping of rubber Chemicals story is surrounded around China and Korea. Good that this aspect is brought up by @phreakv6 . Have to understand more from the Management in upcoming Concall.

Disc: Invested

Sources of some of the Above Data’s and Numbers :

- http://seiaa.gujarat.gov.in/SEAC%20Minutes%20of%20the%20420th%20I.pdf

- http://environmentclearance.nic.in/writereaddata/FormB/EC/EIA_EMP/26052017UH4MORFVAnnexure-EIAEMP.PDF

- http://www.sharekhan.com/Upload/General/Nocil-Jul10_15.pdf

- https://www.dsij.in/productattachment/BrokerRecommendation/NOCIL_BUY_Wallfort_22.01.16.pdf

- https://www.plindia.com/SampleReports/NOCIL-11-4-17-PL.pdf