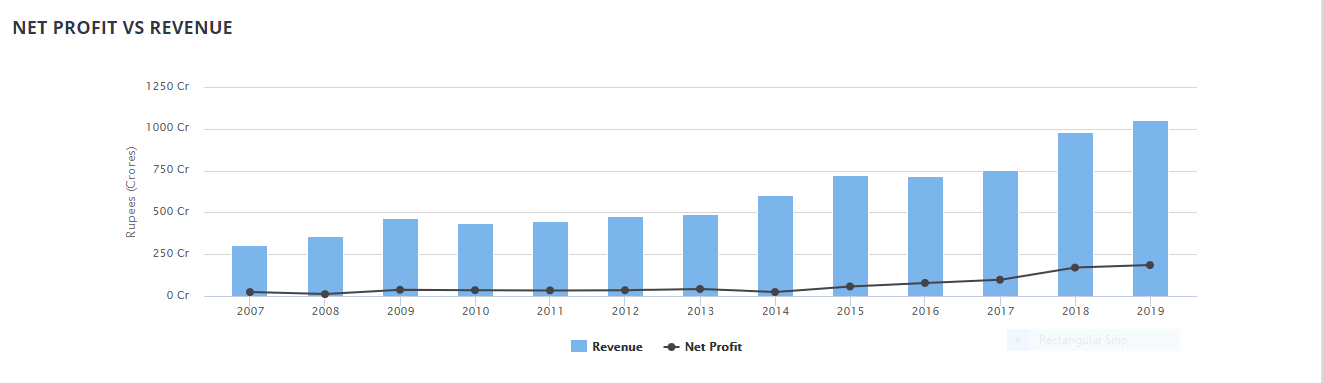

When we see NOCIL from qualitative as well as quantitative point of view with a long term perspective in mind, as a whole it looks as an attractive investment opportunity. The fundamental performance of NOCIL to suffice the argument is its track record of substantial revenue growth that too in sync with the net profit growth in the last 5-6 years :

As we can see from the above chart revenues for NOCIL has a significant uptick in the last five years with net profit also growing proportionately as an indication of improved profitability of the company in the same period. Net Profit Margin for NOCIL during the same period also improved from meager 3.96% to 17.56 percent which indicates healthy improvement as far as its ability to translate a good chunk of revenues into net profit is concerned.

Apart from net profits & revenues, what imparts financial flexibility to NOCIL Limited’s capital structure is the fact that they were able to reduce the burden of debt to minimal levels in the same period, with debt to equity ratio for NOCIL subsiding to zero as visible from the following chart :

The reduced debt burden implies that the company is running its operations purely on-off equity funding. Its recently completed mega CAPEX project for antioxidants and accelerators speaks as a good example for the same.

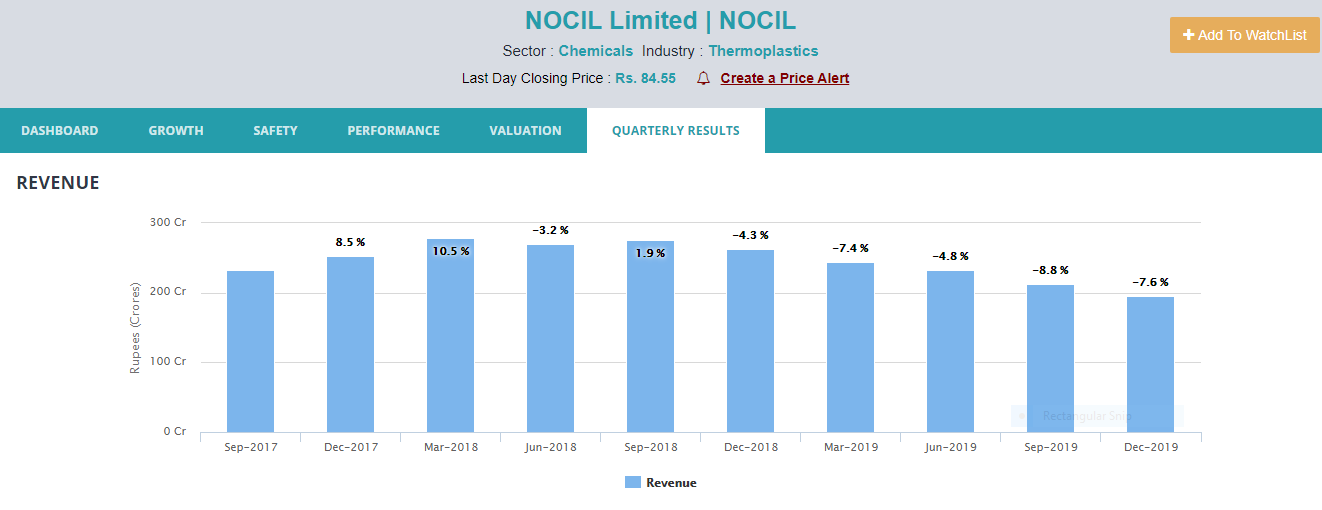

But despite this robust track record, things were not good for NOCIL limited in recent times owing to the significant slowdown in the auto sector. Because NOCIL being a Rubber Chemical player is dependent on the single largest rubber-based industry i.e. the tyre industry, which in turn is directly dependent on the Transportation & Automotive Sector. This slowdown has thus reflected in subdued revenues for the company in the last few quarters :

On the qualitative front, another reason for the downfall was the discontinuation of antidumping duty on rubber chemicals in July last year. To add to that in the last two months, things have become more gloomy owing to the prolonged lockdown arising out of the Covid-19 crisis. The temporary closure of manufacturing operations to go along with the severe demand disruption in the auto sector in the near future present a bleak picture in the near future for NOCIL Limited now. Policy paralysis in import scenarios can also present a cause of concern going forward.

In such scenario key qualitative aspects which should hold the fort for NOCIL (to come out of such desperate times stronger and faster) are: its leading market position, established clientele, sound cost optimization abilities & a better product mix. On a quantitative front, the long term road map for financial flexibility comes from, stronger balance sheet with minimal debt (providing headroom to raise debt should it need to in the future) to sustain and to come out of the timeline of big and prolonged economic crises such as Covid-19.