Few opportunities for Nilkamal

@naman_doshi

something you had already published few days ago. However, this time with some pictures to give a better idea.

4 Likes

Notes from FY 2021 AR iro Nilkamal Ltd -

Plastic Division - The most challenging year in company’s history. Overall volume and value de-growth of 2 and 7 percent reported by this division. The division reported a turnover of 1731 vs 1866 cr last yr. The furniture division bounced back from lockdown by growing by 14 pc between Jul 20- Mar 21. This helped the division recover 95 pc of last yr’s sales. The furniture division focusses on 3 verticals -

Moulded Furniture

Ready Furniture

Mattress

Moulded Furniture - company supported the division by additional cash discounts. The division was back to growth mode from Q2 onwards. Company launched 06 new products during the year. All were well accepted by the market. Company focussed on appointing new dealers and increasing shelf space within existing stores. Aim to launch more products in Chair and Storage spaces to fill in product gaps.

Ready Furniture - Dominated by unorganised sector. Division took biggest hit due labour shortage, challenges around imports and working capital shortage. Supply chain issues due higher sea freight and other challenges around imports were highest in this division. Company could do 88 pc of PY sales by appointing new franchises and launching new products. At present, company has 62 company owned and franchise stores. Plans to add 30 more franchise stores in FY 21-22 Some of the new products launched during the year ( work from home focussed ) were - Computer chairs, office tables, office chairs which were well accepted by the market.

Mattress Segment - Grew by 29 pc over PY. Company gained mkt share from both organised and un-organised segments. Added 7 new products during the FY. Confident of growing this segment by increasing reach and penetration on a pan India basis.

Also introduced a holistic sleep solutions brand - Doctor Dreams. Brand offers - Mattresses, mattress protectors, pillows, Beds and more can be accessed by the consumers at the click of a button.

Expansion plans - aims to expand manufacturing facility at Hosur in Metal, Sofa and panel board furniture. Company’s supply chain, 40 plus Depots, 300 plus sales staff gives it confidence to keep growing in double digits.

It was a challenging year for Industrial packaging division ( BUBBLE GUARD ). Company still managed to grow this division by 6 pc.

Material Handling division - Full of challenges due COVID. However - FMCG, Pharma, Dairy, Food processing, sanitation and Hygiene saw a big surge. Key products in this segment include - crates, racks, industrial cleaning equipment and disposal bins. Other big challenge in the FY was surging RM cost due hike in crude oil prices. With continuous cost saving efforts, the segment remained profitable.

Capex in this segment is underway for production of injection moulded pallets at Hosur. The same is being carried out at Jammu plant.

With boom in E Commerce and company’s good relations with these companies, the segment should do well in future. The pandemic is further pushing the unorganised to organised push in this segment.

@HOME ( lifestyle furniture, furnishing and accessories division ) - Registered a revenue of Rs 157 cr despite first Qtr being completely washed out and tough challenges in importing goods due supply chain disruptions and rising freight costs. @HOME registered online sales of 37 cr. Company closed the year with 27 stores with a total retail space of 3.4 lakh sq ft. Out of these, 09 are franchise stores. Five new stores are lined up at Hubli, Shimoga, Hyderabad, Erode and Hosur. Another five stores are planned for FY 22. Total floor area addition should be around 80k sq ft

Financial results -

Sales - 2092 vs 2257 cr

EBITDA - 256 vs 284 cr

PAT - 150 vs 182 cr

EPS - 75 vs 95

Disc: initiated a tracking position

Views may be biased

Regards,

Ranvir Dehal

1 Like

@ranvir : Incase Nilkamal’s business still in your radar, I seek your synthesized and evolved views for the same.

Nilkamal Ltd -

Notes from FY 23’s AR -

FY 23 financial outcomes -

Sales - 3131 vs 2730 cr, up 14 pc

EBITDA - 312 vs 224 cr , up 37 pc ( margins @ 10 vs 8 pc )

PAT - 134 vs 83 cr

Declared a dividend of Rs 20/ share

Material handling division grew by 14 pc

Furniture division grew by 16 pc

Bubbleguard business grew by 62 pc

Company acquired 70 acres of land at Hosur for Greenfield expansion into continuous foam mattress and ready furniture. Expected to go live by Q1 FY 25

Company makes a variety of plastic, steel furniture. Also make Sofas, Office chairs

New capacity iro Bubbleguard business shall also go live in Q1 FY 25

Ready furniture - comprising of knock down furniture in Wood, Steel and Glass remains a key focus area for the company. Company has been working hard to establish robust retail channel for this business so as to be able to showcase its entire range to the potential buyers. Company now stands at 100 dedicated retail stores with retail space of 4 lakh sq ft. Intend to add another 2 lakh sq ft retail space in near future ( inside 1-2 yrs )

The mattress business could not grow in FY 23. They have put in an action plan to get back to high growth path

E-Commerce continues to be a high growth channel. Currently delivering to 12000 PIN codes in India

Company’s lifestyle retail business -

@ HOME - registered a sale of 230 cr, growing by 29 pc. As of Mar 23, a total of 30 @ HOME stores are operational. 17 are company owned and 13 are franchisee owned

Disc: initiated a small tracking position, may add/reduce depending on company’s performance, biased, not SEBI registered

2 Likes

Not tracking it actively. But a do hold a small investment in the company

Current valuations look cheap to me vs the company’s earnings potential hand hence the potential for higher valuations

One or two good Qtrs and we may be in for some descent returns

2 Likes

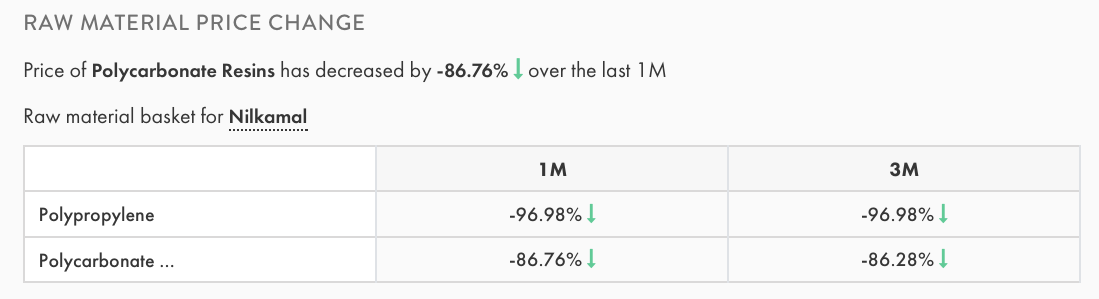

The observed reduction in raw material costs, notably an 86.76% decrease in the price of Polycarbonate Resins over the last month, signals a positive development for the company’s financials. Notably, the company has been engaging in significant capital expenditure over the past two years. Although the specifics of these investments remain undisclosed due to the absence of investor conferences, the potential for these expenditures to enhance the company’s long-term value should not be overlooked. Concurrently, there has been a notable decline in share prices recently, the cause of which is not entirely clear. It would be beneficial for stakeholders to consider both these capital investments and the reduction in material costs when evaluating the company’s future prospects.

2 Likes

Nilkamal Ltd ltd -

Notes from AR 2023-24 -

Financial outcomes -

Revenues - 3196 vs 3131 cr

EBITDA - 294 vs 312 cr ( margins @ 9 vs 10 pc )

PAT - 122 vs 134 cr

RoCE @ 11 vs 13 pc YoY

Some prominent shareholders with their percentage holdings -

HDFC small cap fund - 5.4 pc

DSP small cap fund - 8.6 pc

Kotak small cap fund - 4.8 pc

Seetha Kumari ( famous investor ) - 3.2 pc

FIIs - 1.14 pc

Material handling division grew by 2 pc

Furniture division grew by 8 pc

Company is extremely well positioned in B2B material handling and B2C furniture space

Company is in the process to re-group its furniture business under the following subdivisions -

Nilkamal Moulded

Nilkamal Homes ( including Nilkamal Furniture Ideas and @ Home )

Nilkamal EDGE ( B2B furniture division for schools, offices, healthcare )

Nilkamal ECOM

Nilkamal Mattress and Foam

Regrouping of furniture business shall sharpen the focus on each segment and improve the overall performance of the division

Aims to keep adding more FOFO ( franchise owned, franchise operated ) stores selling Nilkamal’s ready furniture including Beds, Sofas, Wardrobes, Mattresses and Pillows - in the affordable premium and value for money categories

Company’s first phase of Greenfield expansion near Hosur should be over by Q3 FY 25

Company will also commence commercial production of continuous slab polyurethane foam line as a backward integration into Sofas and Mattresses in FY 25 . Will also make technical foam for use is acoustics, automotive Industry, footwear etc

Segment wise performance -

Plastics division grew by 3 pc reporting a sale of 2941 vs 2852 cr. The material handling division is reporting very healthy volume growth but the value growth is restricted by steep fall in RM costs. Company believes that their material handing division is witnessing strong demand from end user industries like - manufacturing and logistics and the same should continue in FY 25

E-Commerce sales stood @ 144 cr, up by 22 pc YoY

The Bubbleguard segment grew by > 30 pc YoY ( for third year in a row )

Disc: not holding, not SEBI registered, posted just for educational purposes

3 Likes

Hi did any1 attend their AGM and if possible can share their notes will be really helpfull

1 Like

No tracking/update on this stock on this forum in last 1 year. Does anyone have any update on FY25 AGM? Company in its statement said that in FY25 they incurred Capex of ₹ 320 Cr with following details -

> Rs.144 crores towards greenfield manufacturing facilities at Hosur for modular furniture and

> foam (total Hosur Capex: Rs. 212 crores).

> Rs.36 crores for rigid plastic packaging units at Puducheny and Noida.

> Rs.23 crores for the BubbleGuard business

> Rs.77 crores across MHD, Moulded Furniture, and other business segments.

> Further, Rs. 40 crores shall be spent in the financial year 2025-26.

2 Likes