@lokeshreddy2007 : When are you planning to move from FD to Equity. 20%-30% correction from current level. What if for the next 3 years indices don’t correct , or remains sideways or moves higher. Patience is key to value investing- but any approx level that you think is good level to deploy cash in equity.

True but its also difficult to know what the peak is by just looking at a chart. Ideally lets say there are some who are like Rj who are really really smart and they will try to exit some of their capital although not all. Usually they will try to exit the ones where they are not majority so their exit is not known to others

Basically you want to exit when they exit or around the time

The lone chart doesnt tell when the top will be.

There are no dates on your chart but I see 4 tops

If you hide the benefit of hindsight you would have missed a lot if you would have sold near the plateau after the second top. There was also a small correction so on the way before the way up you would have sold everything

Even if you would have held at that point the correction after the top just reached the line of the plateau

Those who follow technicals like MarkMinervini have existed and are out of market but they are not waiting for a crash. They are only waiting for a right chart setup. If the market doesnt fall and rally over 52 week highs, they will be the first ones to jump in

2 Likes

For what it’s worth, Sensex crossed 52k in Feb this year and it is still hovering around the same range. Of course an index alone doesn’t give the full picture but one can take some comfort from the fact that it has been more or less sideways this year since Feb.

edit: added since Feb.

I have DCF calculated for various companies so whenever they hit the DCF value i will buy whether there is a correction or not. It may be company specific risk as well.

As of now almost all of them are 40-70% overvalued so there are all in watchlist.

Just for the sake of transparency, I have bought a bit during corona crash which i am not planning to sell anytime soon and moreover i do buy in international markets wherever great stocks are undervalued due to short term volatility.

So as of now I read through annual reports and Quarterly transcripts along with fundamental analysis of the stock and I do DCF if it is stable company or EPS projections if it is growth company offsetting for any anomalies like during Covid 19 many pharma companies produced extraordinary results which cannot be replicated.

I keep refreshing DCF/EPS projections QoQ so when they hit the price i have calculated then i will buy. I have basket of 25-30 stocks and plan is to buy 4-5 stocks. Hopefully 5 of them eventually hit intrinsic price sooner than later. So no time frame in mind.

1 Like

@sanjeev_thakur No, Index has given ~15% returns for this year.

@edwardlobo If you have bought shares/ETF at fair price you never sell unless your target is hit or fundamentals are changed

When we buy stock the first question we need to ask is what is my down side risk here - If it is minimal then second question is upside potential - Must be at least 15% CAGR else better off investing in index.

The whole discussion is about deploying cash at the moment - Your downside risk is very high while the upside potential is low - Exact opposite of what we need

1 Like

There is a point when everything does become expensive. Even Warren Buffet when his wealth was not material frequently sold during market tops. He has just been more innovative to disguise his sales.

Historically very very few companies have survived a lifetime. Stock markets have been existing in the current format since atleast 200 years and not one company has survived that long

If you merely add all of warren buffets initial salaries and put it into the companies he held, and never sold, you will never arrive at the figure his networth is counted in.

mate, all value investors take profits now and then

See recently how much scottish mortgage trust sold tesla that they thought had appreciated

I am only pointing what you said about “never” exiting when i first wrote to you

anyway…what you do with your stock is your business

They bought before the hype. Before the hype its brilliant value based on new cars being launched etc. They bought an ex factory for peanuts that itself was a huge net net value

There are still pockets where valuations are still cheap

Look at steel for instance, china has banned steel exports while also banning import of iron. Before Chinese banned chemicals, chemical companies hardly fetched any good valuation on Indian exchanges, likewise api manufacturers. Many api plants preferred not to run operations but are now highly profitable

Its not traditional value investing where you buy high moat companies but sometimes because of change in the industry these companies start making higher margins.

See for instance Manali Petrochemicals, they are the only manufacturers in India for Propylene Glycol, prices have been rising in China, and manali petrochemicals after 2 good quarters at full utilisation are doubling capacity in next 6 months

Also textiles a huge demand is likely to come due to US preferring non chinese yarn because of opression of minority

While some sectors have reached higher valuation and hence nifty looks expensive its not the case accross all sectors

Probably chemicals the valuation is quite high as Vinati results were good but the stock tanked instead of rallying.

5 Likes

It might even reach 20K hopefully by this year end. More and more the bubble inflates the more it falls when it pops.

It is nothing to do with how many IPO’s. IPO’s are side effects of raging bull market specially too many of them come out at the end phase of bull market. Why would anyone come out with IPO when they know they may not get good valuations and buyers.

I can’t predict what happens next but I am certain that market is overvalued and Just looking back at history it is one of the easiest way to loose money because humans can’t bear losses for long time.

When you invest money your first priority is not to loose money and the second priority is to make satisfactory returns. I see neither of them in the current market.

After a never seen run up in the history of stock market if anyone expecting market to run up another 100-200% is just delusional and All i can say the long term returns of Indian markets would be 8% if you invest now and that’s not good enough returns in the Indian context.

4 Likes

For every bull, there will be bear. For every Dmart, there is an ITC. These discussions are endless and each side can present views based both on history and current situation. Each school of thought, each discipline, each choice of investing, has its own merits and limitations. If Marks has said he knows about markets changing their path, Templeton said he does not what happens tomorrow. Bulls get their chance, bears do too.

I also think there exists a middle way which touches both logic. Froth is always froth, but the reasons for froth could be different, right from the participants to the structure of the rally. Unless there is a definitive impact, a mathematical one, not just an instant perception, one that brings the rally to a halt, like interest rate change, incentive removals, elections, the rally could go on. For the simple reason being, activity begets activity, ease of investing, attractive nature of equity, unaware of the forces which govern the markets etc, bring more and more participants. Although at the end, it is always the gullible, who gets the receiving end, so to speak.

One obvious way is to wait out. Some will have the resolve to wait for years. Such resolve demands conviction, which comes from having insights, experience.

Another way is ride out, allocating that part which at any point of time, could be at a loss, quickly. So being aware of the potential loss and potential gain and testing out, even if inexperienced this before is also justifiable. To each his own. Each experience is a lesson.

Or one could simply hunt for bargains, undervalued bets amidst froth and wait till the froth is over when the needles moves their way.

I think, time in the market is precisely this. Experiencing all kinds of market situations is also an opportunity. Because when we are ready to experience anything, we may not get the chance to experience everything. So I guess, gaining experience, the lessons learnt or taught, although at an expense, will also make an investor better. Like a teacher who is harsh, bitter but provides with a lesson, only he can provide. Of course, not everyone needs to be inclined to learn this way. To each his own.

Whichever path we choose, there are bound to be surprises w.r.t the opportunities that will be presented or missed. And whichever would be the result, it will be a rewarding experience, one that could very well be used in the next bull run.

Like I said before, I am both a bull and a bear, I am invested so I would want the prices to go high, and I am a bear because I would buy more if the prices go down. Yet to take a stance, yet to find a path that is mine, one that makes me sleep good and rewarding.

Just my thoughts.

8 Likes

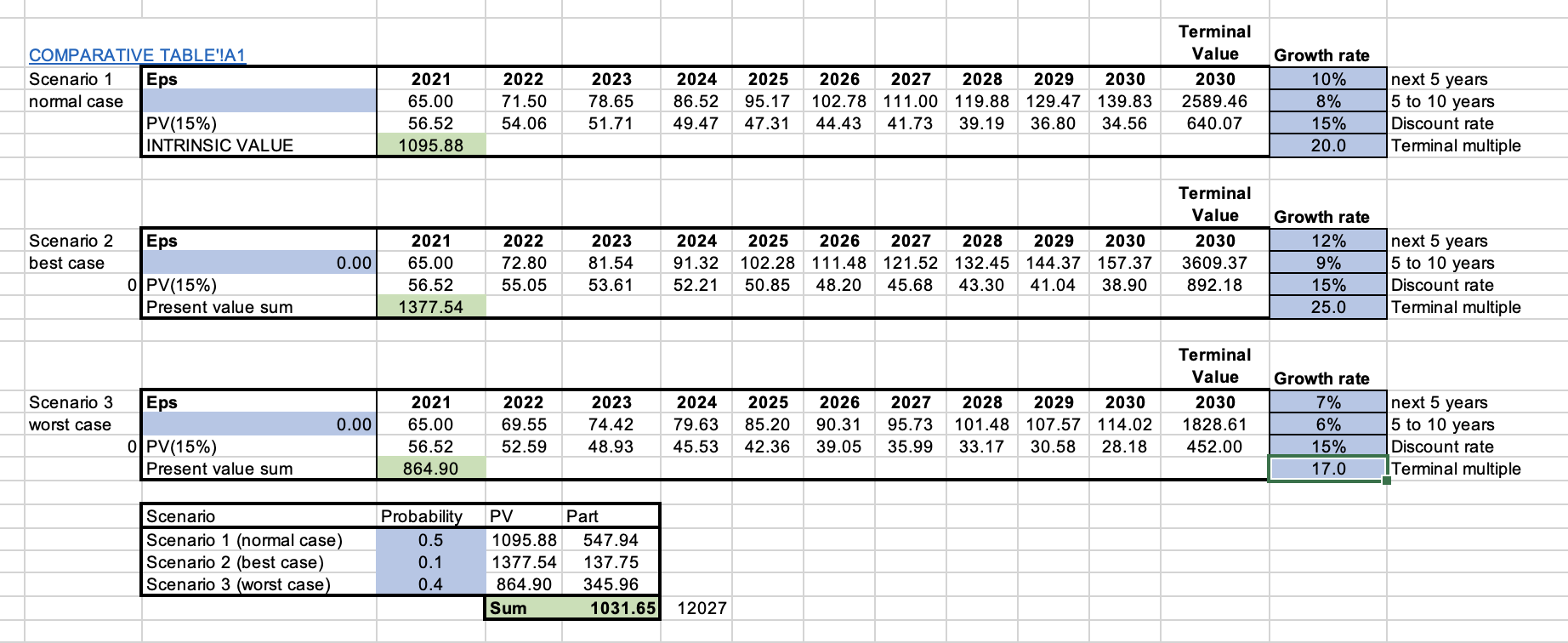

Model doesn’t support 3 digit numbers so treat 65 as 650.

So a simple EPS projection to 2030 which is well above growth rates of Indian GDP (10% for next 5 years and down to 8% there after Considering Nifty PE being 20 in year 2030) we have to buy Nifty around ~11K level to get 15% returns.

In worst case it should be 8600 while the best case being 13700 considering Nifty EPS grows at 12%.

We can make an exuberant estimations like Nifty EPS growing 20% or Nifty PE being 50 in year 2030 but that’s not the way a rational investor should think remember your first task is not to loose money so be conservative with your estimates.

For me by all means Nifty is way too overvalued

1 Like

The more pertinent questions is what kind of connection does one’s PF valuation have with Nifty’s valuation?

I have invested in Nifty and the index is up by 20% since my investment, so if I consider my investment in Nifty to be long term, I would wait for the Nifty to fall so that I could buy more at the price I have invested before. But Nifty could go up by another 20% in a few months, and may fall by 20% owning to different reasons and be at the same level as of now or undergoes time correction. My point is I do not know. If I were to invest now, I would have to look at a lot of things and come to a decision.

And if one is invested in a few individual stocks from Nifty, the overvaluation of Nifty is distributed among the 50 stocks. And even here, the overvaluation is different among the more weighted stocks as they are different businesses from different sectors. Some may have started another leg of their journey like Reliance, Infosys, TCS, L&T etc. So the overvaluation pertaining to these stocks to some extent may be justified.

So looking at index valuation and gauging individual stocks is not entirely correct I guess, there is a connection, but only so much. Historical valuation, median PE, of individual stocks are relatively better measures I guess. Here again, if there is a visibility of growth, sustainability of growth, management commentary, the industry dynamics, all these play a role.

Froth I guess exists in businesses where despite losses, the valuations are high, but here again the argument is, markets are forward looking, the earnings are bound to go up, sunrise sectors, new age companies etc.

And it is also good to see an opposing view, which acts as a reminder of the other side of the coin, the side that should not be forgotten, the side which should be remembered from time to time, that it exists.

1 Like

I didn’t say Individual stocks are overvalued but Nifty is but then the stocks I have been watching are way too overvalued so for me there is nothing to buy at the moment.

PE or Historical PE is never a right measure. Last 30 years is not same as next 30 years so they are meaningless. I prefer to use projections based on FCF, EPS or DCF and see if the current price of a stock in a buy range.

FCF or DCF is not so useful in Indian context since not many companies are doing buybacks or paying good dividend so my go to method is EPS.

Generally Estimated EPS is already available till 2025 so you need to make educated guess for next 5 years and arrive at current buy price.

According to my estimates all the stock which are in my watchlist are priced to deliver 6-8% in long term.(Which is good returns for US/Europe Investors because their banks are paying 0% so anything is better than 0% and their inflation is 2-4% so 6% is real good returns but for Indian investors anything less than 12% is not an acceptable return, 15% is ideal)

Overall market is overvalued but there maybe Individual stocks which are undervalued.If those stocks fit your criteria then you must buy. If market does correct the stocks which are undervalued will fall less and you at least know why you bought certain share.

I recently bought Facebook(Not a buy recommendation) because I feel it is undervalued and great stock to own though overall US market is crazily overvalued

As we are an emerging market, and the percentage of people investing in equities, and in direct equity are less, ours is a fluid market at least for the present. When the tide will turn is anybody’s guess. Even I look for a broad valuation method, as there are few things that are exclusive to our market, like rainfall, incentives, interest rates etc, in addition to the global moves that directly impact the market.

And as we as a market mature, that 12% return will also be hard to come by, particularly with Nifty. And when the breadth and depth of the market increases, the returns will be even less, which I am not sure, considering the financial climate that is present in India. So only a handful of names always make the headlines, are crowded, and are rewarded. And if that happens, foreign money will move to other lucrative economies.

So, while we could borrow the recipe from US, we should add our own ingredients to the dish, to make it complete, which I guess is changing fast or at the least has begun to change.

From a sheer learning and experience perspective, I would like to witness a bear market or a sideways market, so as to know what exactly are the reasons for such environments to exist, and see the up move again. The broad reasons, generalization or blanket statements are not enough. And I for one cannot obviously time the market, and I may have to wait for, I don’t know how long, to have the benefit of hindsight. It could be next month, or it could be next year, or the bull run may very well extend to the next term of the current government.

Even I am baffled and kind of feel unexcited, when I see the indices going up by 0.5% every other day, saying to myself, this should not happen or how can it go up. Monetary gain does not equate to an experience in its entirety, gain or loss is a part of an experience, not the entire experience. When one is not greedy, or when one knows about the volatility, the fall will not be shocking. The extent of the fall, the pace may surprise, but not the happening.

And yes, despite decent EPS growth, or visibility of earnings, some stocks are not favored, as all eyes are on the raging bull.

Filled with doublethink, mixed feelings, inexperience, naivety, so interesting times.

if some stock is undervalued then most often it is for a reason. Mis pricing by the market generally happens when there is uncertainty around company in the near team since most analysts are at most look for few months to a year.

I don’t know about other stocks but ITC is getting punished for not being ESG compliant. Market is expecting them to de-merge which company is resisting. Moreover ITC is not that cheap either. Compared to broader markets and peers yes but if we consider conservative growth estimates then it is slightly overvalued.

1 Like

10% to 8% GDP growth rate is the real rates, right?

EPS growth will correlate with nominal growth rate which is real growth + inflation. Given the money printing, inflation could be a very high number in coming years.

Yes, Nifty EPS grew around 13% from 2003 to 2013 around 9% from 2011 to 2021 which includes massive spike in the year 2020 (EPS moved from 450 to 650) otherwise growth rates are much lower. We have much bigger base now. So I don’t see Nifty EPS growing at an astronomical rates of 15-20%.

Well even assuming a 8.5% growth rate and 4.5% inflation, we get to 13% nominal growth. And I do believe, we will do better than 8.5% because of few reasons:-

-

Tech & Remote working :: Indians are gaining massively and this is showing in IT attrititon pressures as wage costs rise. Lots of startup founders have especially tweeted about talent scarcity and rising costs. From a macro pov, this will a) +vely impact consumption b) increase service exports c) nudge indian cos to go global

-

China + 1 :: Reading con calls of API plus chemical players gives an indication of where the puck is moving. Diversification is slow but it is happening. Because of pharma / API chains reducing dependency on China, we see Indian commodity chemical cos gaining in recent times. This trend will only accentuate and diversify to other sectors in future.

-

PLI :: Benefits will show in terms of domestic value add from next year onwards when companies start meeting their obligations. Also some of the sectors are niche and have high export potential. Eg: drones, EVs.

-

EV Hockey stick :: I personally believe that this decade will see a marked shift away from ICE to EVs. For energy importing country like India, this would mean severely reduced oil import bill and hence lower pressure on fiscal. Increasing public capex or personal tax cuts? Either ways, will positively impact consumption.

I don’t think all of it is fully factored into projects yet especially some structural shifts in chemical / pharma happening on account of China + 1. 15% EPS CAGR growth is very much reasonable and maybe we may end up doing more.

https://trendlyne.com/equity/EPS/NIFTY50/1887/nifty-50-earnings-per-share/

NIFTY PE is currently 27. Post end of Q2 season, this will fall further since a lot of banks, IT included in Nifty 50 will post better nos on account of provision reversal and pickup in loan books. If you see the chart above, you can already see that current EPS doesn’t factor into the recent IT results. Once all of this moves, the PE will go down and Nifty may again chase a 27/28 PE.

3 Likes