Exactly but then let’s not forget the fact that markets were not as over valued as they were today. Liquidity drove the markets forward until 2018 when FED and ECB decided to stop QE and absorb some of the liquidity that’s when markets tanked and continued until end of 2019. Somewhere in the middle of 2019 Fed again announces that they are buying bonds again which triggers off rally in large cap companies and later in the beginning of 2020 there was a rally in small and mid cap companies until corona crisis.

now that Fed has already confirmed that till 2022 there won’t be any raise in interest rates and they would be doing infinite QE to come out of corona crisis there is every chance that rally might continue but that doesn’t mean stock market is cheaper. If you have invested money then let it grow but any investments now may not justify risk adjusted returns.

While i don’t book profits except in small caps with the current run up in stock markets right from 2014 due to massive liquidity when it really plunges not sure how deep the correction would be. In March it plunged 40% in no time shows that investors just don’t have confidence on that current market. It is rather driven by Fed’s assurance so when they back track we are definitely looking for massive correction. Markets will again get back and start moving upwards but then we shouldn’t end up like Nikkei where it is yet to recover to the levels it once achieved even after nice 25 years!

Nikkei didn’t move cause Japan’s economy didn’t move. It’s a country that’s actually shrinking in size and grew at 1-2% in last 25 years. India on the other hand is the fastest growing major economy in the world. Nifty will be upwards of 1,00,000 in next 25 years. That’s why I don’t see the point to stress so much on 20-30% short term corrections. I would rather spend my time researching about companies and accumulating cash to buy whenever market corrects significantly.

Excellent, That’s my theory too but in the past i made a mistake blindly buying companies at higher valuations specially small cap companies. When bear market started they cracked by 50-70% so lessons learnt. If you buy stocks when they are beaten up you get better risk adjusted returns and your chances of higher returns in long run. My theory is “Buy low and hold on as long as you can” but only in case of small cap funds i do maintain portfolios one for long time and one for short time. So short term one i book profits regularly when i feel small caps are getting expensive, maybe they run up for some more time but when they start correcting you do get discounts of 50-70%.

[UPDATE] Just realized Nifty being at 1L after 25 years works out to be CAGR of 7.88% which is too low hopefully it would be much more than that.

Professor talks about partial protection using index options. Can anyone share experience of increasing cash position vs Hedging using derivatives?

I did both during March drawdown last year and derivatives paid off better. When using derivatives, you stand chance to loose the premium you bought for, in cash you stand chance of loosing the upside if there is a sudden uptick like last year. If you have a fairly large portfolio, you would want to consider the premium paid as an insurance. With cash, you need to time the market to reenter back. It paid well for me as i had bought many puts but whatever i exited during March in stocks, they went up so soon i couldnt enter thinking its a dead cat bounce. I guess there is no single answer for this but one should have a mix of both always to save capital and recoupe some losses if things go south.

Post #1729

Hi

I see some interest amongst us on how to ‘hedge’ ones portfolio. Few years ago on this thread around 2017-18 we did have discussions around hedging. Let me share a few thoughts on what I have done. Please note this is something which is a mix of experimentation as well as learning from theory. Also we have to consider money management as one aspect. It is also evolving. My thoughts one year ago would be a tad different from what it is now.

These are only thumb rules!

Most of us are retail investors and get streams of income in terms of cocaine shots called salary at the end of month. This increases our cash pile every month (minus the expenditures). How do we deploy this? Only 3 things can happen - a) do nothing b) deploy everything c) deploy partially (and where - this is stock selection essentially).

A dozen pointers

- If index valuations are below median levels it is highly probable you have a low risk of permanent loss. e.g.: I always deploy to the hilt when there are major crashes (The cash which has accumulated). It does not mean that in tomorrow’s crash this will hold true as every move is random but we take on that risk basis historical data. There is a probability of no recovery mathematically. Say in March we had 2-3 weeks of such scenarios. Even if one closed his eyes and deployed they would get a good profit. It is humanely impossible in my books to time macro so I don’t even think about it much. Yes it is very difficult to put in large amounts in crashes. I only added to existing positions and bought a lot of index. Another example is the ILFS crisis. Crisis is to be used.

- More from a chart perspective - Try to deploy everything provided you know where to deploy if N50 is above an EMA of choice. Simple as that. If I don’t have any investing ideas I tend to keep it in the index. And when I have some stock picks to make I use that money. Yes it is volatile but you can test it. I prefer to use 100 DEMA and tend to look at exhaustions in price by way of variance/channel breaks.100 DEMA & even percentage of stocks above 200DMA serves as a trend indicator. I do have knowledge of candelstick patterns as well as chart patterns but they are a hit or a miss. I would also recommend to go through Lance Beggs books on Price Action trading (not that I use it but I am able to gauge in my mind. I am in no way associated with Mr Beggs)

- When the index is below the choice long term EMA and you observe a reversal deploy partially and then fully once it crosses the long term EMA. How do we check reversal? Patterns/2 or 3 very short time frame DEMAs again.

- Have a ‘sureshot’ stock idea - This should supersede everything. For instance you were in 2012-13 and you chanced about a company which makes shrimp feed. What would you do if you were confident in the pick? Have minute positions in many stocks 50-60 but really large in ones as a percentage to your net worth in those you are confident in. It should create some form of discomfort. That discomfort will push you to know more & track more.

- No investible idea + High index valuations + Index below long term EMA of choice - this is the ideal candidate for shorting the index which I did when the collapse began. I avoid options because there are quite a few moving parts. Simple index futures is my choice. I keep minimum 10% cash in liquid always for such situations. Now how it pans out is that we get a crash you short in a day or two. Then index valuations may become cheap you either unwind shorts and deploy if indicator EMA/valuation suggests. No one at least I think so can get this perfectly right. Objective is to make broad choices and have action plans ready. Prefer to write them down. Looks easy to do but is nerve racking with a ton of see-saws. Also there is no such thing as a perfect hedge for retail folks. Stop looking for it. It is very costly to do. Learn to digest drawdowns.

- Buying deep OTM Calls or Puts is like buying lottery tickets. Don’t bet the house on it. I don’t recommend it.

- Suppose you have an equity portfolio value of 1Cr with a beta of 1.2 (say heavy BFSI) you should calculate notional hedge value to know what you are getting into. How much in a collapse will you protect 10L/20L? Know your beta please.

- Get it out of your mind that you are going to make money from FnO. You are going to use it to soften your blow of a drawdown. Screenshots are mostly fake. Twitter is mostly folks trying to milk naive folks. It is for entertainment mostly.

- By default it is better to be always invested, all else are exceptions. Price is the epitome of all factors - macro /fundamental/emotional etc etc. Respect it. As Peter Lynch says - The stock doesn’t know you own it. So treat it that way. Always look for negatives in your stock picks but have a huge barrier to exit. Selling should be multifold more difficult than buying.

- Use only Nifty50 Futures for extreme cases when below 100 DEMA (or whatever you back test). Its very liquid and helps cushion. The thought of gap ups and downs will not let you sleep well. Be warned.

- Do read up some basics of derivatives - John C Hull and Natenberg for Options. I have studied Finance and really loved Derivatives & risk management and thought I would be good at it. I blew up a month of salary in one lunch while I started work post MBA. Be humble.

- Do the work yourself. Make your own rules. Trust your own philosophy. No one can teach this.

All the best to your investing and trading!

Rgds

Deepak

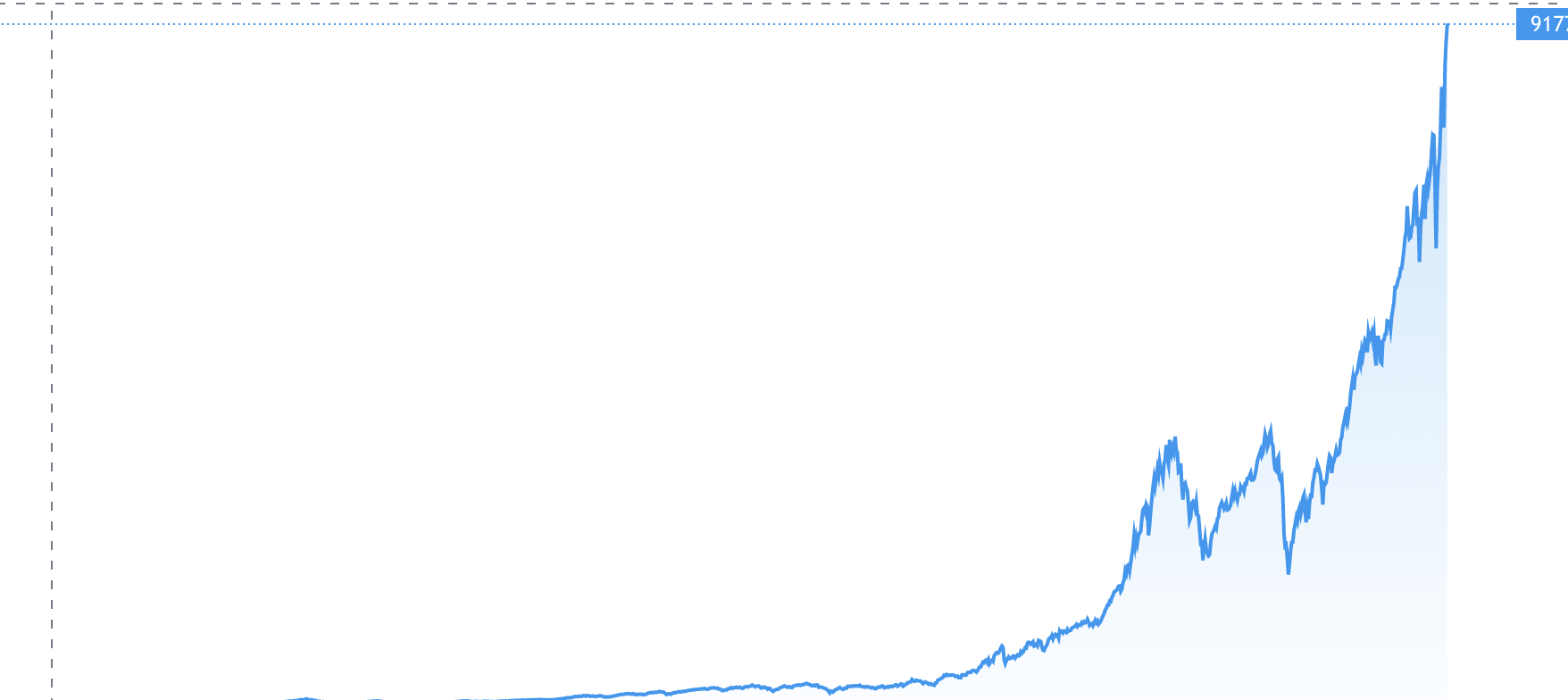

Does this look sustainable?

This is how it ended last time.

One is SPX from 2009 till date and the other one is Nikkei in 1989.

While we may argue that situation is different then and now but fundamentals remain the same.Law of averages will eventually catch up. It should have been by now but then the cheap money from FED is finding its ways into the system.

Let’s see the events that has happened in India starting from 2016:

- Demonitization

- NBFC crisis

- Jet airways fallout

4.Yes Bank fallout - DHFL fallout

- Corona

- Automobile slump.

- Flat earnings growth.

With so many problems we had only one year where we had moderate returns (2018) why? Because FED decided to perform QE tightening.

SO Indian market just does’t care much about domestic events but more about actions of Fed.Fed prints money market runs on steroids Fed stops printing money market starts falling. Earnings, domestic events etc… matters next to nothing.Watch out for Fed. The day Fed decided to do QE tightening market will follow. so watch out for Fed.

@tommy123 Do you buy far dated options as insurance? How do you calculate the right lot to buy vs your total portfolio amount? I was looking at Nifty 16000 Dec Put Options and even one lot is priced at 1 lakh. One lot would hardly be enough of an insurance policy.

@lokeshreddy2007 Nifty CAGR for last 20 years is 13.5%. At 13.5% Nifty should be above 1.76 Lakh in the next 20 years. Hopefully next 20 years will also give better CAGR of 18-20% since India is now the fastest growing economy in the world.

I wasn’t worried about market rising too much too fast but everyday my portfolio is increasing by more than 1%, this definitely isn’t sustainable. Nifty was at 14000 on 1st Jan (which was still expensive), even if it gives let’s say 25% returns this year from existing 14000 level on 1st Jan 2021, it comes to 17,500. Nifty is already hovering above 15,000 and we still have almost 11 months to go. I am increasingly getting cautious of a bubble in stock markets. Everything is moving up way too fast and it usually is a sign of end cycle of a bubble.

There are companies in US that have gone public via SPAC and suddenly are worth over 50 Billion dollars. This is after CEO of the company has given guidance that they will not make any sales and have zero cash flow for at least next 4 years.

I have decided to buy far dated out of the money put options for Dec 2021 and hedge myself. Happy to lose the premium than face the possibility of a 50%+ correction in my portfolio.

If anyone can help me point to right direction on how I should go about hedging myself, it will be really helpful.

The cleanest option is to reduce your equity allocation rather than get into complicated hedging arrangements. For example, if the equity allocation is 50%, then even with a 50% decline in the market, 75% of your net worth is intact, which is not such a bad thing. You can then decide what to do based on the situation.

If you are buying to protect your capital, you would need to buy something like dec month 12000-13000 pe to capture the downfall in index. Most of the time it may expire worthless but it’s good to have to protect from severe downfall like last year.

Lets say, if you have a portfolio of 40l you would need to buy approximately buy 4 lots of nifty. I. E total portfolio value/nifty contract value.

You can buy at the money option as well, this will be more premium paid from your end though but provides more cushion.

This is strictly to protect against black swan events,not some 10% correction in markets. If market ends at 10000 by dec expiry , you would recover your investment losses from the options you bought. Also suggest you to buy these options when india vix is around 15 so that you don’t pay much for these options.

Thank you, this is very helpful. Unfortunately Vix hasn’t gone below 18 for a while now.

I do want to protect against black swan events and think buying long dated out of the money options is a better way to hedge as opposed to decreasing allocation to equity, at least in my case. I am 20 something, very high income and negligible expenses. I have 2 years worth of expenses saved up as emergency fund and a little bit of walking around money. Rest I am always 100% invested into equity as my investment horizon is 25+ years.

Taleb always advocates to insure against tail risks and hedging now against extremely overbought market seems like a good tail risk to hedge against.

Buying December 2021 PE could be a reasonable hedge. The premium LTP is about 388. Thats about 2.5% and I suppose you then hope to continue riding the market.

Portfolio risk could be higher than Index, depending on how it is structured. So you need to understand how many lots to buy. Maybe do a combo, book some profits and also hedge with the index.

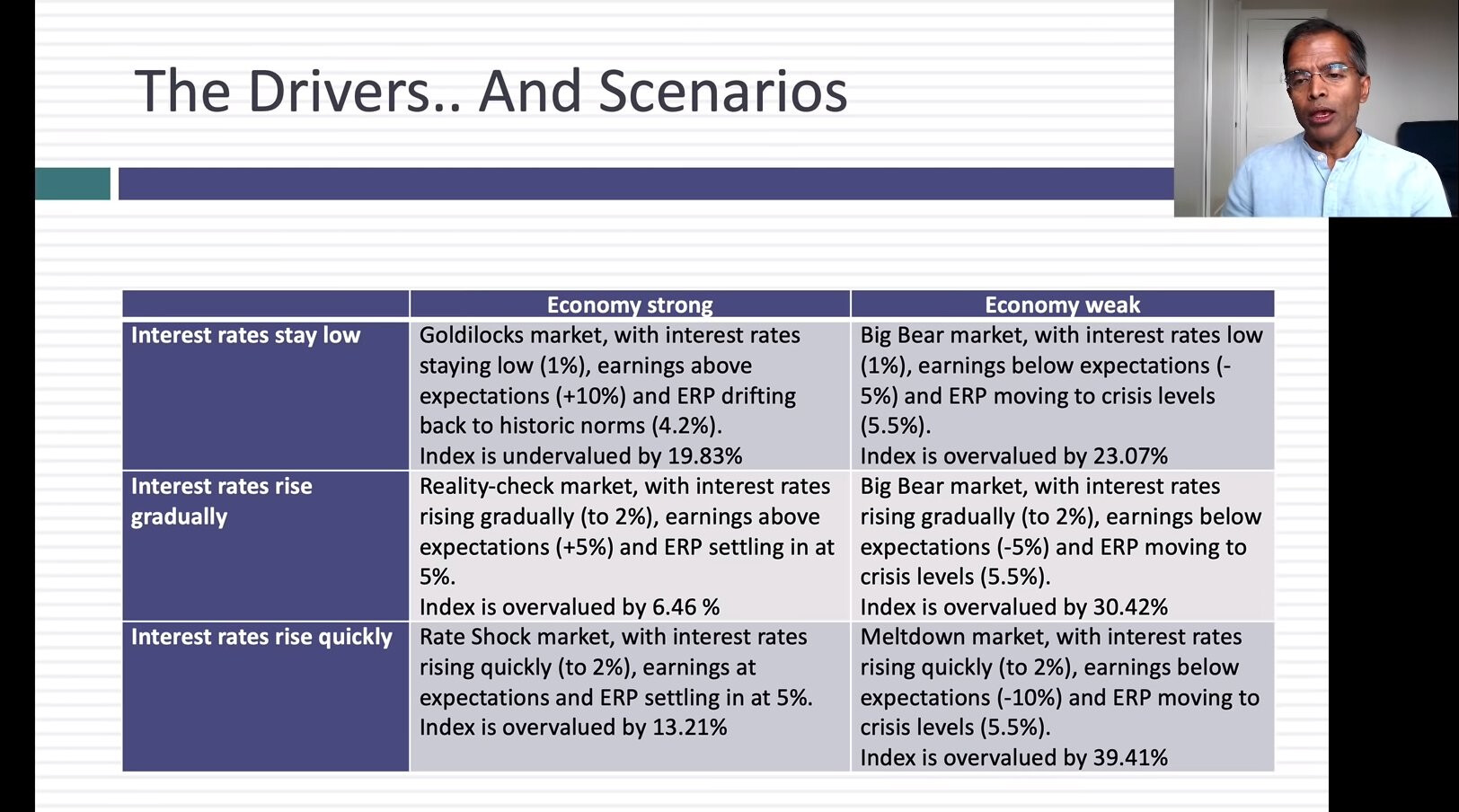

As per Damodaran, market is undervalued in 1 out of 6 cases and over valued in 5 out of 6 cases.

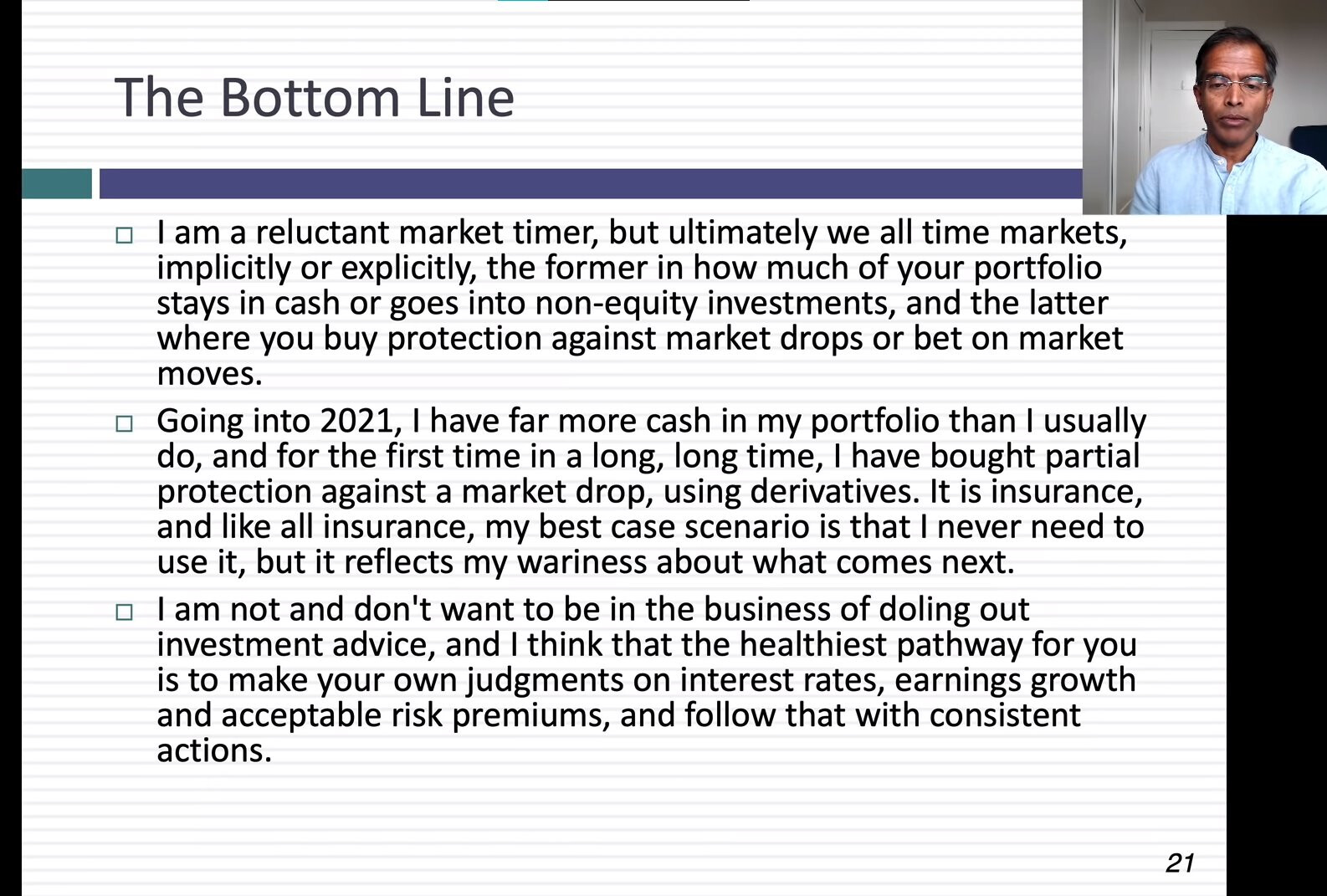

For the first time, in a very long time, he also has bought puts options against the index as an insurance against his portfolio.

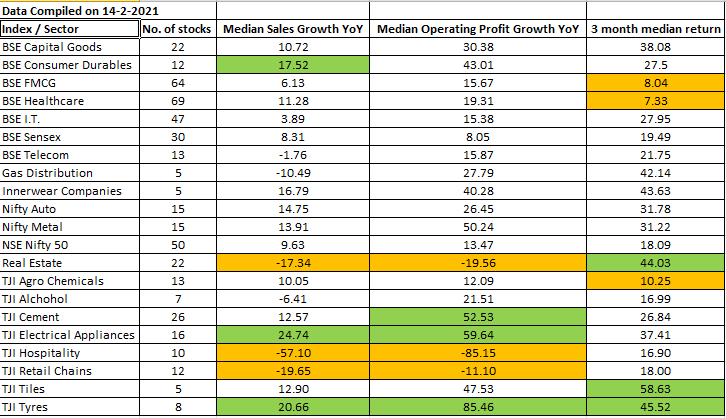

Now that the dust has mostly settled around Q3 FY21 results, it is time to look back on how companies across various sectors have performed. With this in mind, the table below is plotted which gives performance of some sectors of interest to me. It gives:

- Median YoY sales growth for the quarter

- Median YoY operating profit growth for the quarter

- Median 3-month stock performance (i.e. post Q2 results to post-Q3 results)

of companies within the selected indices / sectors as on date.

I have used median values so that the numbers are not distorted by extreme values which occur due to exceptional reasons in one off cases. This approach also removes the distortion caused by differing weightages of individual stocks within the indices. For example, return on the median stock within an index would be different from the index return. 3-month stock performance shows market’s perception about Q3 results vis-à-vis its expectations of Q3 results.

You can draw your own conclusions, but a few observations are given below.

- Most sectors have recovered to their pre-Covid levels (i.e. Q3 FY20) with many of them far outstripping the last year’s numbers. Electrical appliances and Tyres are more than 20% above their last year’s levels. Only 4 sectors are more than 10% below pre-Covid levels i.e. Real Estate, Retail Chains, Hospitality and Gas Distribution.

- Operating profit growth is way ahead of sales growth. So the massive cost cutting and higher capacity utilization is clearly evident.

- Not a single sector shows negative stock returns with even the median Hospitality stock giving a 16% return.

- Flavours of the season have surprisingly not done all that well. For example, median I.T. company showed YoY sales growth of just 3.89 %. Median healthcare stock has returned 7% in 3 months, and is at the bottom of the stock performance list!

These are median values, so obviously half the companies have done even better that this. You can compare your stocks to their sectoral medians to see how they have done. The top 3 and bottom 3 sectors are highlighted in colours.

Hope this is useful.

(Explanatory note: Data in a row does not belong to the same company. For example, median healthcare company in the sales growth column (11.28 %) is SPARC while operating profit growth (19.31%) is Jubilant Pharmova and stock return (7.33%) is for Morepen Labs. So each value in the table has to be read independently.

Source of the data is Screener.

Excellent analysis, thank you.

Only if available and convenient, would you also have a mean analysis for this, rather than the current median one. Just my opinion, but won’t that even give a truer picture of how sectors earnings have performed basis their valuation increases?

Quite intrigued with the data set. While the market becoming buoyant before every declaration of results, stock having stellar run just a week before the result and then continue the journey post declaration of good results. How is it that suddenly every industry and company within it is more or less showing superb runrate and whole Indian market is kind of like turned around in just one quarter. So here are my two cents:

-

Q3 was also a period when Indian market started opening up post COVID days (Oct’20). Thus superb topline growth has considerable element of pent-up demand as well and both Y-o-Y and Q-o-Q comparison becomes kind of irrelevant for me. Each business numbers require special lens to ascertain if real uptick is round the corner or is it just a gap filling of previous lost demand.

-

Profitability had a major element of lower discretionary spend and as economy is opening up - discretionary spend like rent, travel, incentives, discounts - all are going to come back. This will lower the current run rate and thus the earning estimates as well. Q3 has also been unique quarter wherein every result is followed by an earning as well as valuation upgrade just by extrapolating one quarter numbers.

-

New budget guideline will also force major companies to write off majority of their goodwill on the books in Q4FY21 or Q1FY22.

-

Tapering will surprise the streets sooner than the people expectation and thus scenario of lower rates may not stay for long. What is happening in the US and now also in India is something not sustainable. When your housekeeping / driver/ watchman start giving you stock tips and you get a massive FOMO feeling we must agree, the end is not very far. While one must ride the current rally and stay invested, one should also be quick enough to stay hedged as well as keep their mind, eyes and ears open.

-

Banks / NBFCs have not yet started reporting true NPAs and this may bring lot of skeletons out once they start normalizing the reporting practice post the end of Supreme Court ruling.

Having said this, there are certainly new emerging trends driven by COVID led pandemic and this may bring out new set of industry and companies a winner over next decade. Every rally is supported by new sectors and companies and hence once need to re-balance the portfolio as well depending upon individual goals and aspiration.

Happy investing.