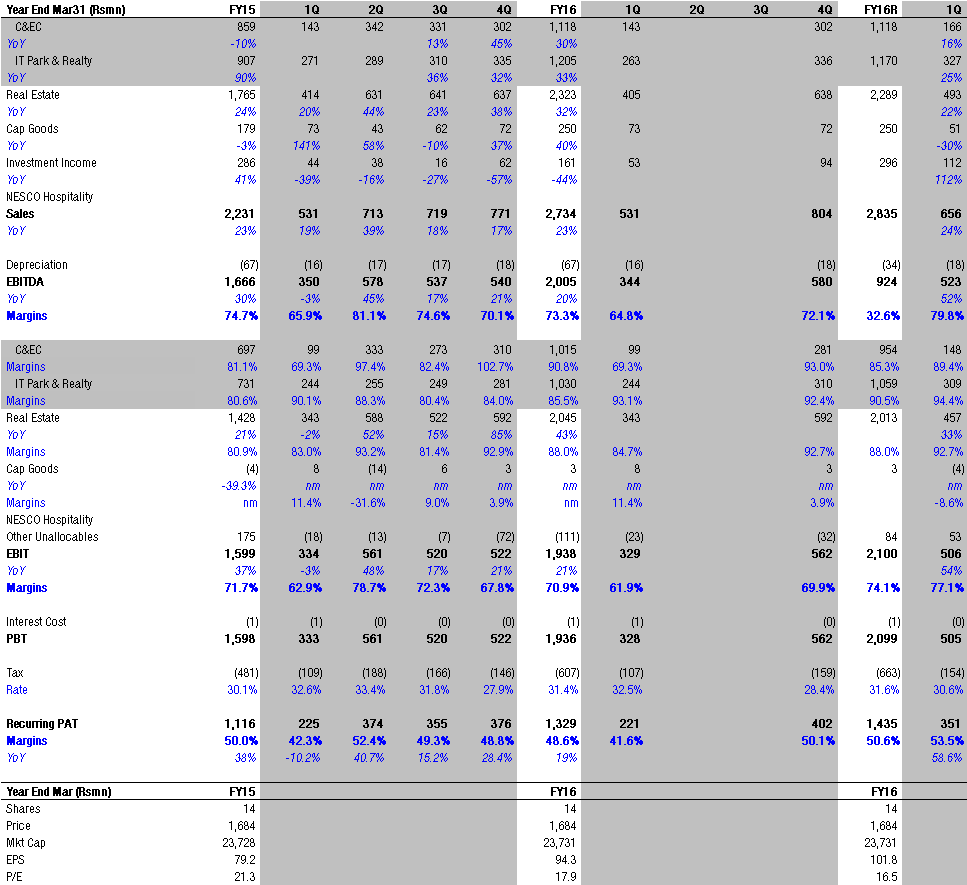

Another great set of numbers by NESCO.

1Q PAT up 59% YoY. Numbers restated due to change in accounting to IND AS. So FY16 EPS revised upto 101.8 from 94.3 earlier.

Hi,

As per a document I had read long back, the FSI for IT Buildings was 5. Could you help clarify the same?

Of immediate interest to us is the IT building 4 which is coming up

measuring nearly 12 lakh sq ft. It should be up in 15 months from now.

Later IT buildings 1 and 2 will be redeveloped. Measuring FSI and TDR is

complicated business.

Definitely. But there should be some number right? The difference between 5 fsi and 2 fsi is huge! Do any of the other forum members know what the actual fsi given to IT buildings in Goregaon is?

full agree. right now I am going by what the management said at the AGM - FSI of 2 instead of 1 for IT/ITES buildings and FSI of 3 instead of 1 for exhibition centres. Management says they won’t be able to load further TDR in addition to the higher FSI.

New development is the metro track along the NESCO property. Some land could be acquired for infrastructure which would permit more FSI to be utilized. Norms for development of property 500 mts on either side of the metro line after payment of premia is also being worked on.

So we have got to wait and watch how this plays out.

1 Like

The current rental rates prevailing around Nesco for IT commercial spaces are around 110-150 per square feet per month.These rates are excluding the common area maintenance which the companies have to pay apart from rent.At times companies also have to pay hefty charges for parking places.

At prevailing rates, while the new building can easily add around 150 crores to revenue (12 lakh sqft*12 months *120 per/sqft) we should also closely monitor the supply in that area. Adjacent compound (Nirlon), which I believe is hosting premium facilities when compared to Nesco, is coming up with a new IT building (Nirlon Phase 5).At the same time Oberoi Commerz 2 which is not very far from Nesco is ready and almost vacant. Considering these factors , timely execution of IT building 4 is the key.

@vnktshb @Shivkumar - Is there a fixed split (out of the total 70 acre ) between exhibition and IT. Now that we have the new FSI norms we would be able to calculate the total area which can be built up giving us some idea of the runway ahead.

Evaluating the length of runway is important as the business model seems simple where capex is 2500-3000 per sqft to get the new facility online for leasing which is recovered in 2 years (125 per month *24 ).This can only go on till they run out of land/FSI which was acquired long ago at throw away prices.

Once they reach the peak by running out of FSI (though it seems far as of now ) incremental revenue would be mere 5-10℅ which is achieved by increasing rental rates YoY.

Disclosure: Not Invested.Still Evaluating.

I work in Nirlon compound which is adjacent to Nesco.

4 Likes

I agree that a lot will depend on how much the management is able to negotiate rentals. Usually, it takes them six months to a year to fill up a building after completion. So I am looking at full occupancy of IT 4 only by second or third quarter of 2018.

At the AGM management indicated that the exact ratio of IT Park and Exhibition centre would be worked in consultation with the architects during development of integrated plan.

Obviously Exhibition/Convention centres enjoy higher FSI but the unpredictability of the Exhibition business and possible competition from the Reliance Centre at BKC will play big role in the decision.

Revamp of the Exhibition centre will start only from 2018, so things will get clear going forward.

2 Likes

Considering both the space under development and the kind of capex Reliance is incurring for their exhibition facility it looks like their development should be much more advanced than Nesco’s current exhibition centre. Also BKC is a far premium location than Goregaon where Nesco is located.

Below is something that I found on web regarding Reliance exhibition centre coming up near BKC.

"Samsung C&T who has developed famous skyscrapers like Petronas Twin Towers in Malaysia and Burj Khalifa in Dubai is developing Dhirubhai Ambani International Convention and Exhibition Centre (DAICEC) at BKC

The 788,340 square metre Dhirubhai Ambani International Convention and Exhibition Centre (DAICEC) in Mumbai, India will cost US$ 678 million. Samsung C&T expects to complete construction in 2017.

Samsung C&T has won the US$ 678 million contract from developer Reliance Industries Limited (RIL) for the construction of the Dhirubhai Ambani International Convention and Exhibition Centre (DAICEC) in Mumbai, India.

DAICEC will be a mixed use development located within the Bandra Kurla Complex (BKC), a commercial zone in the suburbs of Mumbai. Covering 75,000 m2 of land with 788,340 m2 of useable floor space, DAICEC will house a convention and exhibition centre, auditorium, cultural plaza, serviced apartments and an office block.

Construction is expected to be completed by 2017."

1 Like

Recently I have learnt that NESCO will start organizing events under their own banner. This is a marked change in their approach from being only a B2B player to venturing into the B2C space.

This weekend will be the first such event conducted by NESCO - Paddy Fields.

The next such event will be next year. In all they are expected to do 20 odd events each year.

While I’m not sure how these changes things, here are some thoughts -

- Opportunity to fill out empty days when there are no events, thus leading to better utilization of assets

- Better utilization of cash on books as it is getting invested back in business

- A differentiator as opposed to what competition might not do (w.r.t to Reliance) or may do?

- May impact margins as marketing costs may go up to promote the event (not sure how much this would be). They will also have some additional salaries to pay to pull off the event.

- May positively impact the catering business - more captive audience to sell to

- Impact on valuations should be largely positive as it will be entering into the B2C space

Kindly take this note as a heads-up on developments that may or may not happen. Thought it’d be helpful for the community hence sharing what I’ve learnt.

Discl: Invested

6 Likes

there will be many such opportunities for events here since the catchment

area has a young 20-something crowd. Last year, an organizer had held an

all night party at one of the halls.

Since the hall is completely enclosed, the 10 pm restriction on loud

speakers will not be applicable. Since the exhibition halls are really

huge, these can accommodate big crowds willing dance all night long.

disclosure: invested and hence biased.

Good results. FY16 EPS was 102. If company shows no growth in 2HFY17 the NESCO will get to atleast 115 EPS of. If there is some growth we can expect EPS of Rs120 IMHO. At closing price of Rs1976 stock trades at 16.5x FY17E.

1 Like

I am tracking NESCO for a potential very long term exposure (>10 years). My assumptions are below:

In the long term, I expect the following by year 2036 (20 years from now):

-

Total 70 acres of land fully built up

-

IT buildings: 50 lac sqft leasable area

-

Rental doubles every 7 years. Hence 8 times from today. So rent psft = Rs. 100x8.

-

Revenue = Rs 800x50lacx12 = 4,800 Cr

-

BEC: 1.5m sqft, revenue up 8 times (rental growth) and 3 times on FSI growth from current levels.

-

Revenue = Rs. 2,400 Cr.

-

Net revenue excluding cap goods and return from cash investment = Rs. 7,200 Cr

-

I am assuming they close the cap goods business in the long run.

-

Since the management is conservative, I expect them to take no debt. So they will build up cash before building a new building, which is why they will take a good 15-20 years to fully develop the remaining land bank.

-

Any cash balance after 20 years will be accretive to valuation.

-

Assuming nil cash, and taking a long term EV/EBIT of 10x, assuming 70% EBIT margins, EBIT = Rs. 5,040 Cr and hence EV of Rs. 50,040 Cr.

-

Implied upside: 16.40% CAGR (which is well above average long run equity returns)

In the above case, implied PE is 14x, which is reasonable.

Another valuation approach is as follows:

- Current land value is Rs. 6,000 and they have utilised only 40% of the same, which is earning c.200Cr. This implies a yield of 8.3%.

- Long run yield is ~6.5% for commercial. 3. After 20 years, land value would have gone up 16x. Assuming doubling every 5 years.

- Hence land value = 6000x16=Rs 96k Cr.

- PAT yield = 6.5% x 96,000 = Rs 6,240 Cr.

- Assuming 10x, implies market cap of Rs. 62,400 Cr

- Implied upside: 17% CAGR (which is well above average long run equity returns)

Risks:

- If company starts debt financing, its risky

- Sumant Patel is very conservative, not sure about his son, Krishna Patel.

Upside:

- Persistent frugal running of business may lead to cash surplus.

- Krishna has been innovative in leasing out BEC for B2C events, which is a good start.

Disclosure:

Not invested. Hunting for a long term stock.

1 Like

This is a different and innovative turn. Succession was a worry for NESCO but looks like Krishna Patel is slowly getting in the groove

The station closest to Nesco Ram Mandir (Oshiwara) finally got up and running yesterday after a wait of 10 years.

Nesco is now well connected by road and rail. Not to mention the upcoming metro line on the western express highway which will make it even easier to access the location.

All great developments.

Disc: Invested

8 Likes

Attached is the detailed analysis on future capex plans of NESCO and detailed model. Once we put description into numbers it starts making sense. As such the net income can become 3-4 times (from current levels) in coming years.

NESCO_v1.pdf (1.1 MB)

NESCO_model_v2.xlsx (21.8 KB)

@vnktshb - Thanks for sharing the documents on NESCO. It helped me immensely to build the model.

Disclosure: Invested

14 Likes

Great work Vivek… Low divided is one concern I have with nesco given its cash position and operating cash it’s generating

@pkranthikumar - You need to understand that company is doing capex for next 7-8 years for 1500 Crores with internal accruals and not intending to use debt at all. It has incremental RoCE of >20%. As a shareholder you must be happy that it is not paying huge dividend and deploying money which creates incremental shareholder wealth without dilution.

Disclosure: Invested

3 Likes

Hi vivek

have you considered any probable impact from the reliance convention centre ? is that a risk ?

It is a potential risk. And I think considering the dearth in quality space in India (especially Mumbai), the impact is likely to be minimal. Plus the size caters to different client segment.

Also, if you see on the map, Reliance convention centre is not directly accessible through NH or train. Nesco has this unique advantage.

My view is that upcoming BEC which is 4x the current size is the management’s thought process for countering modern exhibition from Reliance. So, existing BEC can cater to small clients and those who require modern and large space can take new BEC.

On pricing, I think exhibition business is quite inelastic. So, unlikely to have any price war. Let’s wait and watch how it unfolds.

Plus, in the model have considered very conservative estimates including occupancy of new BEC which gives margin of safety.

1 Like