Both aspects are true: Property / Real estate ‘will suffer’ and ‘will not suffer’ as well!

’will suffer’ because - perception / sentiment is bigger than reality. so the first reaction of the potential tenants, consultants, investors and every one associated will be to go in a ‘hold mode’. and since stock market are discounting machines, they would show reaction of this sentiment by way of draw-down in stock price.

’will not suffer’ because - eventually, commercial office space has its value - be it data security, identity, not all works can be sent to home (there are many social, psychological, physical space concerns), and not to forget the importance of collaborative environment - and thus it will slowly gain it’s importance back. May be moderate rental management for few months need to be done, may be rentals will not go up for some time, but the one’s who will suffer will be small / B grade commercial office space buildings; better tenants will get aggregated at better buildings, for reasons of better identity, security and sanitation controls and competitive rentals. Plus, the overall social distancing norms, especially norms of the MNC, will increase the ‘per sq ft per person’ requirement from current average norms of ‘80-100 sq ft per person’ to say a 10-15% more. So, eventually it will all balance out. . . . In same way, exhibition will crawl back too; as there’s no way to do exhibitions and trade conferences online, be it for industrial goods or be it consulting seminars; interaction / networking / demonstration / touch & feel can only and only happen in physical world! . . . Likewise, food and catering too will come along.

. . . And not to forget that RE automatically adjusts to interest rates and inflation. with dropping interest rates, and in effect the rising of cap rates, the lost value will get added back to overall asset value.

BUT, what will surely suffer is shared economy - co living, co working and all!

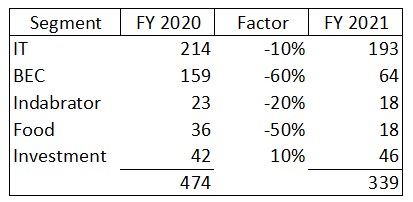

so, in sum, let market beat down the price as NESCO’s business income is going to surely suffer for next two quarters - but this will be opportunity to make most of the crisis!. . . if one believes in story then, NESCO is surely a proxy RE investment to enjoy gradual gain over the years to come!

. . . at 360 - 400 level (assuming nil revenue from BEC and food for 2 quarters), i feel its equivalent to investing in under-construction office or shop that normally smaller investors do; and atop it you get prudent management, experience, quality tenant and all; and all this without any headache of property management, broker’s fee, registration stamp duty, tenant scouting etc. plus the optionalities of empty land / future hotel / more IT buildings and large cash / investments reserves!