Did anyone write to Navneet Education’s CS and get the reason for this investment? In the absence of a very good reason, this investment does seem ridiculously dear.

3 Likes

Earnings Transcript of Navneet’s Q3 earnings call - https://www.bseindia.com/xml-data/corpfiling/AttachHis/eb49a36a-2bfc-48b4-92cb-08e98fdadcfa.pdf

Worth reading, lots of interesting comments by the management on their business vision. Questions were asked about the 75 crore investment in SFA. While I couldn’t get clarity on why the valuation was so dear, the business rationale was explained well.

This is, in my view, now a bet on whether Navneet can execute on the vision. If so, this will be a multi-bagger. But it’s not a short-term investment - a two-year hold at least. IMHO, any short-term up move will depend on the stationery exports growth which is not being spoken about much. If Navneet does not execute well enough on the digital vision, one has to hope the management’s ethics are strong enough not to weaken the parent company’s financials.

4 Likes

I fail to understand why have they bought into this sports business.

This is a loss making entity. Generated revenue of 7.3ce in 3rd year of operation. It will take ages for Navneet to recover this investment.

If anyone of the learned members has any understanding of how this sports business functions then pls share it with us.

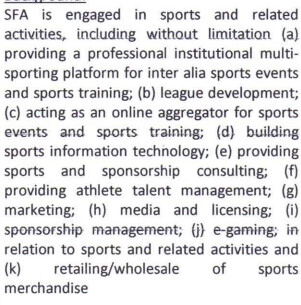

These are the fields of operation of SFA

1 Like

Is there any further update on NEP implementation in Maharashtra & Gujarat board?

While the rationale behind this investment might make sense the valuation is insane!!

500 cr valuation for a co with 7 cr revenue? And it’s rated a 3.1 on Google out of 5, so doesn’t seems like a co which has done something groundbreaking.

A short research report with updated developments.

This report was originally written in FY21 as part of personal investment record. Updates have been made wherever necessary.

Business Overview:

- In the business of publication of books for Maharashtra and Gujarat State board schools and CBSE books under the brand name Indiannica (erstwhile Britannica).

- Cyclical nature of business with bulk of revenues coming in Q1 and Q4.

- Stationary products(paper/non paper), exports of which contribute majorly to revenues.

- E-Learning solutions under the brand name E-sense Learning.

- Managing schools under the brand name Orchid International Schools. (K12-Techno).

- Majority of the revenues is through publishing and stationary business.

Probable reasons for current valuation: - Loss making business verticals

- Significance of publishing business in a digital age (probably a newspaper moment for the business).

- Love and excitement among the people for edtech platforms.

- Has failed to capture CBSE publishing market share(yet).

Reasons why current valuation is wrong (mispricing exists):

-

The drop in revenue for FY21 was caused by the lock down which was announced by the Central Govt. in the last week of March. Most of the revenues are generated by the company in the months of April-May as students buy books for the Academic Year which starts from June. This should normalize by FY22.

-

Revenues have normalized by FY23.

-

There is a virtual monopoly of the company in the publishing business in Maharashtra and Gujarat state board schools.

-

There are approx. 24,000 CBSE schools pan India. But there are more than 24,000 state board schools in Maharashtra itself and new schools keep opening every year to pick up on the schools that have shut down.

-

And the students of Maharashtra and Gujarat schools are captive customers as they are dependent on the books and guides published by the company for exams.

-

Plus, there is high competition in the CBSE space among publishers and to add to that schools have themselves started publishing their own books.

-

On the ed-tech front, the company is venturing into the field and leveraging the long old relationships it has established with the schools to get the product rolling.

-

But the argument against the significance of the company’s core business (publishing and stationary) does not hold up. The reason being, the amount of fees charged by the darling ed-techs (Byjus, Unacademy) is more than the fees of the state board schools (where the company has a monopoly). The parents cannot afford these exorbitant fees charged by the ed-techs.

-

Update FY24- Massive correction in valuation of Byju’s.

-

Plus, the ed-techs are not officially affiliated to any Education Board, while Navneet’s books and guides strictly follow the prescribed curriculum. And the experience and expertise of all these years in the business is an intangible asset which translates into the brand name.

-

The company witnesses a more than normal revenue and profit growth once in every 4-5 years when the syllabus is changed and students buy new books. This will be the case in the next two years on account of the New Education Policy.

-

The company is also trying a pilot project where it will also sell books through its website in a digital medium which if successful will reduce the capex as no physical copies have to be printed. Update – Seems unlikely.

-

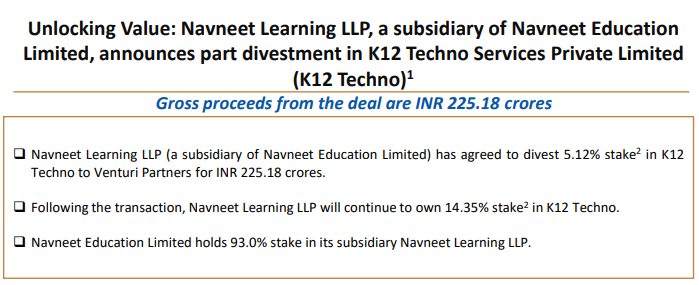

Update – Company has 20% stake in K12 Techno valued at 800 Cr as of Q2FY24.

Some Numbers…

Key takeaways from my crunching of the Annual Reports (not from Screener)

-

Current valuation (as of 04/02/2021) is almost equal to the revenue.

-

Current Ratio>2

-

Negligible Debt

-

ROE & ROCE>20% (presence of moat/competitive advantage as suggested above as a monopoly in Maharashtra and Gujarat).

-

Intrinsic Value based on DCF of Owner Earnings,

Where Owner Earnings = (Net Profit+ Depreciation&Ammortization - Capex)

Note: did not take working capital changes into account while calculating owner earnings.

Discount rate – 10 Yr G-Sec yield.

Intrinsic Value= 4500-5500 Cr

Update- Could be significantly higher if company unlocks value by selling 800Cr stake in K-12 Techno. Management would think about it in coming 2 years.

- Margin of Safety >50%

- Probable correction of mispricing Q4FY22-Q2FY23 with opening up of schools and syllabus changes which will also give a boost to the ROE and ROCE. Update- Current market cap (September 2023) around 3100 Cr.

- Recommendation – Buy at 3100 Cr levels as well despite run-up in price as Board is highly vigilant as they cracked down on loss making ventures and Management (Gnanesh Gala,MD) is honest about headwinds and tailwinds alike and wants to create minority shareholder value.

3 Likes

Could you please tell why you have discounted risky cash flows with risk free rate of return, which is obviously lower? Effect of this is that your calculated intrinsic value will be higher

2 Likes

Valuation is highly subjective. The cashflows you are considering “risky”, do not seem risky to me. Students are going to buy books year after year in the respective states. Stationary sales are also robust and growing. I have used a very conservative growth rate despite NEP tailwinds and the 800Cr stake in K12 techno which may be sold in the next 2-3 years. That is a direct inflow to profits. One can use RFR and add to it all kinds of premiums (CSRP, Size premium etc., fellow Investment Bankers would be aware of these terms) and find out the WACC but that does not capture risk imo.

1 Like

It’s over 2 years now since I made this comment. Unfortunately, their tech/digital vision did not pan out, while SFA has not made much money yet though they seem to be executing well (based on management commentary). With NEP policy long delayed and at least a year away along with other challenges, publications business has not seen much growth.

Stationery exports should have been the trigger for rerating as I had mentioned then. Unfortunately, they faced some trade restrictions due to US policies and lost a good chunk of potential stationery revenue. Seems to be sorted now. It’s pretty much a stationery exports and to a lesser extent domestic stationery growth play now as the legacy publications business is unlikely to see much change over the next 6-9 months.

I had mentioned this as a two-year hold then, I would say that’s extended further now. That said, their K-12 investment has turned out be excellent allocation of capital. Anything unexpectedly positive on SFA will be a bonus.

1 Like

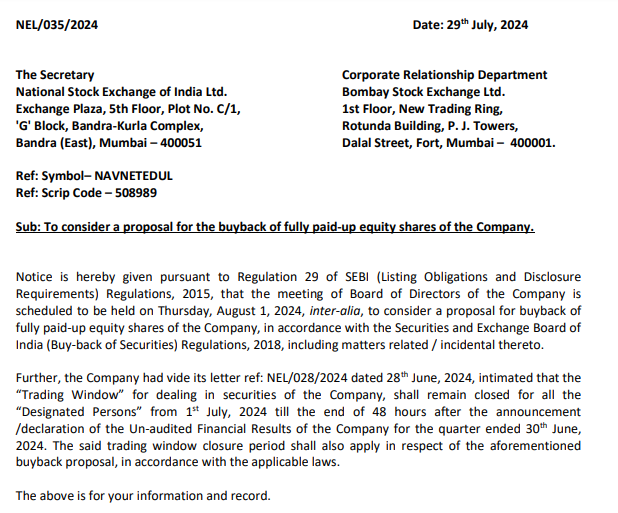

As per today’s announcement, Company has proposed to consider the buyback.

Also, one its peer company, Chetana Education’s shares are about to get listed on SME platform on 31st July. It got subscribed 197x !!! At higher band of Rs. 85, it’s valuation is coming to ~14x P/E. Any one tracking this company / sector?

3 Likes

Board has decided to do buyback of 50lacs shares at 200/- per share, which is premium of ~20% from CMP. Promoter to also participate in this

1 Like

If the opposition party comes to power in Maharashtra, any idea if they would scrap the NEP implementation? I tried searching for articles on web, but couldn’t find any.

1 Like

Continuation of existing government in Maharashtra is positive for the company - NEP implementation should accelerate now.

1 Like

1 Like

Following up on this after another year. The company says all the right things but has kept underperforming. On the publications side, it is not that much in their control as the curriculum changes have not happened meaningfully. So the demand there continues to be muted and with paper prices low, realization is also impacted a little bit. Indiannica (on the CBSE side) has not performed at all. Acknowledged by the management this time. It appears they don’t have a good strategy there. Overall, my sense is that there is a sales leadership gap in the organization at the 2nd level.

On the stationery side, domestic sales and margins have suffered due to paper price decline. That seems to have stabilized now, but don’t think it will change much. Exports has disappointed a bit. I was expecting them to do better than what they had projected, but they have actually underperformed. They are investing and expanding into more categories/products (including non-paper stationery products like file folders and others), but don’t seem to be aggressive enough to maximize the opportunity. Maybe FY26 will be better, but that’s only if they can get 2-3 big export orders. So far, nothing to indicate that will happen. And then, there’s of course, the tariff uncertainty.

On their other minority investments - they have pretty much written off the edtech investments in two companies - Tinkerly (which has shut down) and another which is barely surviving. Given what they said this time about SFA’s profitability challenges, it’s possible that may get written down too at some point. I wouldn’t be surprised if they further monetize the K-12 stake this year. That’s been the only positive (and a significant one) on their non-core investments so far.

Overall, not much to look forward to right now. It will chug along unless exports surprise significantly in either direction.

4 Likes