Bonus Summary

The last bonus that NBCC (India) had announced was in 2017 in the ratio of 1:2.The share has been quoting ex-bonus from February 17, 2017.

If we buy share today. can we get bonus share or its already adjusted.

Regards,

Bonus Summary

The last bonus that NBCC (India) had announced was in 2017 in the ratio of 1:2.The share has been quoting ex-bonus from February 17, 2017.

If we buy share today. can we get bonus share or its already adjusted.

Regards,

It’s already adjusted.

Yesterday was the last date for the same.

NBCC is planning to start Mumbai’s Dharavi slum re-development. Apart from this it has also started its ~Rs.8000 crore project of building 2,000 flats across Wadala.

Are we seeing good time ahead?

Dear Friends,

Trading at its 52W lows around Rs. 68 today, is NBCC in Buy range now?.. Any views?

Hi,

I think it is still little bit above the fair value. But, we can’t catch the bottom always. So, I think you can buy in SIP. It would have been a great buy at 50-55, but I have purchased 60% at 68 and waiting to go down around 55. But no doubt from 3-5 years perspective it is now attractive. As pointed by fellow members of this forum with these 2 main negative-

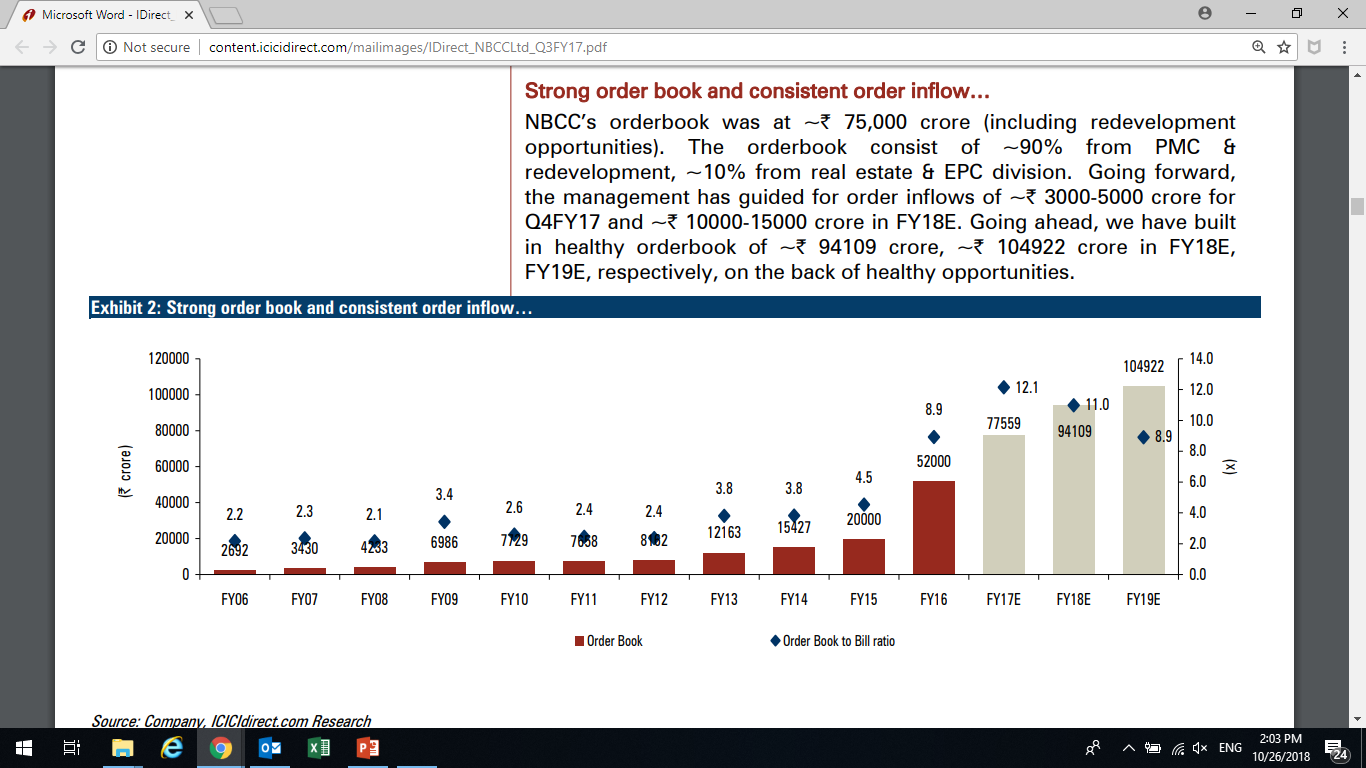

For a company that does approximate Rs 6,000 Cr yearly, does it matter an order book of Rs 80,000. Why is order book important for its intrinsic value?

Hello everyone,

I’ve recently invested in this scrip and did a bit of research around the company and the sector.

As pointed out earlier this forum, the company is operating as a virtual monopoly given the nomination based orders that it receives.

Current order book stands at a staggering 80,000 Cr. which is a big jump from it’s historical book size.

Now , the company has given a revenue growth guidance of 35% for the next few years, considering the same, the stock looks fairly priced at the current levels.

One downside to the growth is the fact that ~50% of the orders are from redevelopment projects in Delhi which might see some delay due to ongoing issues.

Please contribute to the above analysis and correct where i have been wrong.

Good results from NBCC… EPS improvement is a good sign…https://www.bseindia.com/xml-data/corpfiling/AttachLive/d5a5c458-9ce7-4160-8f53-0c4e3ce89b78.pdf

you still invested? what is your future outlook?

I feel NBCC after a bad 2017-18 going to come out of dark and likely to prove a dark horse, multibagger stock if one can buy is for 3-5 Years, Target Rs.250-Rs.500 and current mkt price is 52 around.

I will appreciate views of others. Positive or negative, except the coversation like if stock is so good then why stock price is not picking up.

It is better to discuss business along 3-5 years instead of giving speculative multibagger targets.

See table below and track it…one day you will agree…

| NBCC PAST AND PROJECTED | FY 20 E | FY 19 E | FY 19 TTM | FY 18 | FY 17 | FY 16 |

|---|---|---|---|---|---|---|

| Year over Growth | ||||||

| Revenue | 30% | 30.0% | 28.8% | -6.5% | 27.4% | 32.4% |

| EBIDTA | -8.2% | 4.2% | 28.7% | 9.7% | ||

| PBT | 6.00% | 20.50% | 11.00% | 4.10% | ||

| PAT | 40% | 32.5% | 4.8% | 0.0% | 22.8% | 4.0% |

| EPS | 3.67 | 2.61 | 2.07 | 1.97 | 1.97 | 1.61 |

| Current Price | 55.05 | 55.05 | 55.05 | |||

| 52 Wk - High | 109.2 | 109.2 | 145.65 | 99.8 | 80.96 | |

| High Date | 18-Apr | 18-Apr | Nov.17 | Oct.16 | Aug.15 | |

| 52 Wk - Low | 47.2 | 47.2 | 85.5 | 58.67 | 46.67 | |

| Low Date | Feb.19 | Feb.19 | April.17 | Jun.16 | Apr.15 | |

| PE Range | ||||||

| PE at High | 41.8 | 52.8 | 73.9 | 50.7 | 50.3 | |

| PE at Low | 18.1 | 22.8 | 43.4 | 29.8 | 29.0 | |

| Current PE | 15.00 | 21.09 | 26.59 |

check here for view on govt. businesses:

Dear Amit,

Stock market is game of patience, NBCC it self gave bumper return between 2014 to 2017. Its not neccessary that all stock should move alongwith performance, that is called behavioural investing, many of us simply discard the stock as no broker is covering , as no big investor has bought, as MFs holdins are low. They all are not clevar guys we will come to know that they have the stock when stock prices get double and they comes out with report to fuel the prices for their exit.

Rest we had posted it and now onlt time will say that after 3 years this stock will be of Rs.250 or Rs.20.

Do we have any news, idea of any reason stock crashed 13% today?

Appreciate your expert advice.

All PSU stocks down…BEL,ONGC,OIL,COAL INDIA,IOC…list is long…didn’t performed during MODI 1 too…merciless dividend stripping,constant disinvestment through CPSE is not shareholders friendly…1.05Lac Cr target(Yr after Yr)…gimmick in the name of disinvestment(Selling HPCL TO ONGC)…obviously market punishing.Learned hard way to stay away from PSU.

Check here for view on PSU:

Was having a few doubts regarding this company’s analysis-

@bheeshma and other real estate experts, it would be great to get your input.

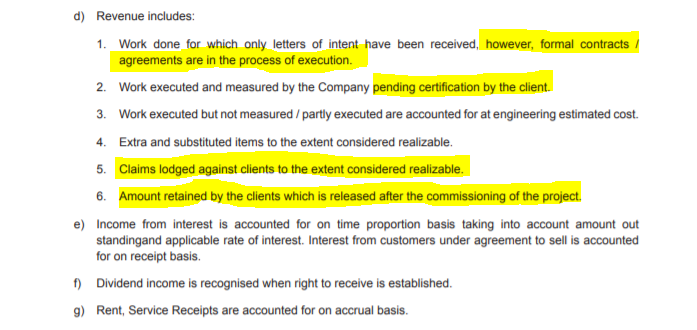

Are these how usually revenues are recognized? Please note that this is a PSU -

In cost plus contracts, how much is the usual cost plus fee rate for a PMC?

The company claims to make 8% as their cost plus rate for the PMC segment.

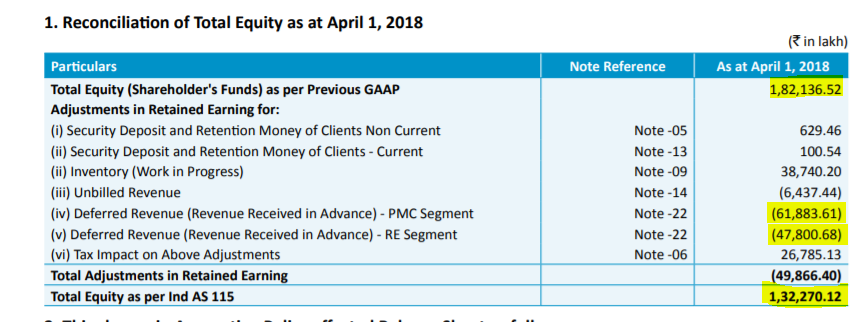

How does one actually analyze the revenues recorded? One can see a huge difference based on the changes in accounting standards -

In such a scenario, what would be a good measure of the avg capital employed in the business?

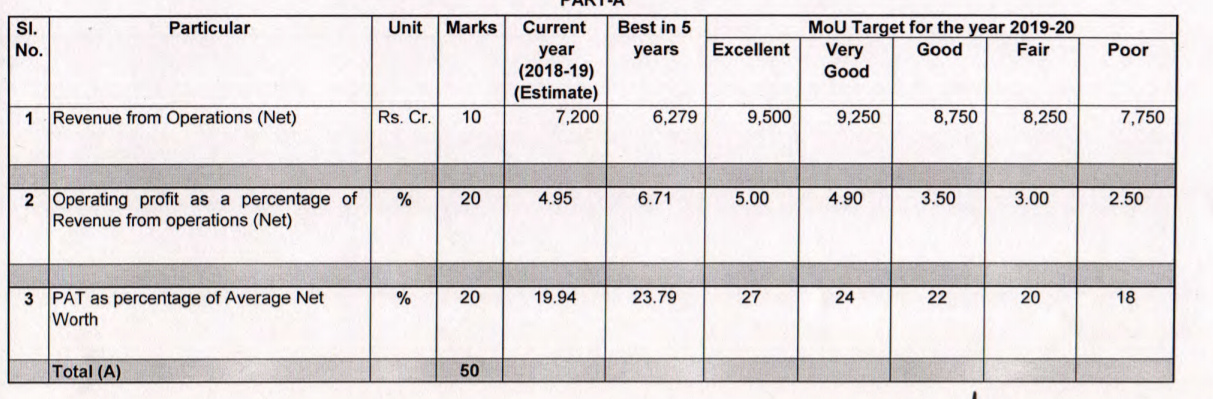

P.S: The MOU with the Ministry of MoHUA states an expectation of max 5% operating margins as an excellent performance target.

NBCC derives most of its revenues (~90%+) from PMC activites and the rest from its real estate development and EPC projects. The revenue recognition articulated above is for EPC and like all other EPC contractors revenue is recognized as and when work is completed as certified by an architect. In real estate projects revenue is recognized when OC is received and in PMC , revenue is recognized as an when the performance obligation is completed.

Generally PMC fees vary between 5% to 10% depending upon the complexity of the project.

Accounting policies in real estate and real estate contracting are painful to understand and i have no clue how to analyze Return ratios and integrity of revenue. The only helpful statement that makes sense is the cash flow statement which seems to be good for NBCC.

That said NBCC has a mammoth order book but how it will translate into actual revenues has always been a overhang.

Best

Bheeshma

Thanks a lot for your input!

@kashif_1461 May you please rename the topic to NBCC if that’s possible and allowed by the forum?

Because people would usually search by that name.