Results of Q2. Revenue and expenses increased. PAT is flat. EPS is down due to higher equity. details below

Press release. Gives some insights.

disc: invested

Results of Q2. Revenue and expenses increased. PAT is flat. EPS is down due to higher equity. details below

Press release. Gives some insights.

disc: invested

subscription based, hence I cannot see the whole article.

Release some of pledge by promoter entities in last quarter.

will they be affected by d recent court hearing on mosanto patents as dey might bring new generation of bt cotton seeds.

Further reduction of pledge by Ashu Farms and now at 5.53% from 8.68% (out of 10.99% holding) is reported to exchanges. This is a good news.

Nath bio-genes released standalone figures in Q3.

Q3 was muted. Compared to last year PBT is 4.27 C compared to 3.94 Crore. PAT is 3.50 Crore Vs 3.95 Crore last year due to 77 Lakh Tax this year compared to 0 last year corresponding quarter.

Press release comparing 9M performance and reports as a strong quarter compared to last years 9M.

Nath Bio-Genes has been growing both it’s top & bottom lines by 20% over the last 3-4 years. Company’s Market Cap is still under book value. Apart from the pledging by management, can’t see any negatives here (Management has promised to remove the pledges in a recent concall). Any thoughts on this anyone?

We might have a Phil Fisher type stock at a Ben Graham price.

In recent quarter the pledge has increased inspite of decreasing

The recent quarter result have been very poor.

The high working capital with high debtor days leading to given poor valuation despite having similar OPM to market leader KSCL (20-25%) and better than other peers–JK Agri Genetics/Bombay Super Hybrid seeds-(<10%)

Now the top and bottom lines de growth seems to be discouraging.

Anyone having more deeper insights related to the company.??

Any specific reason of horroble Q4 nos.

Anyone who is tracking this company promoters added a lot some months back, can anyone simplify their cotton seed speciality.

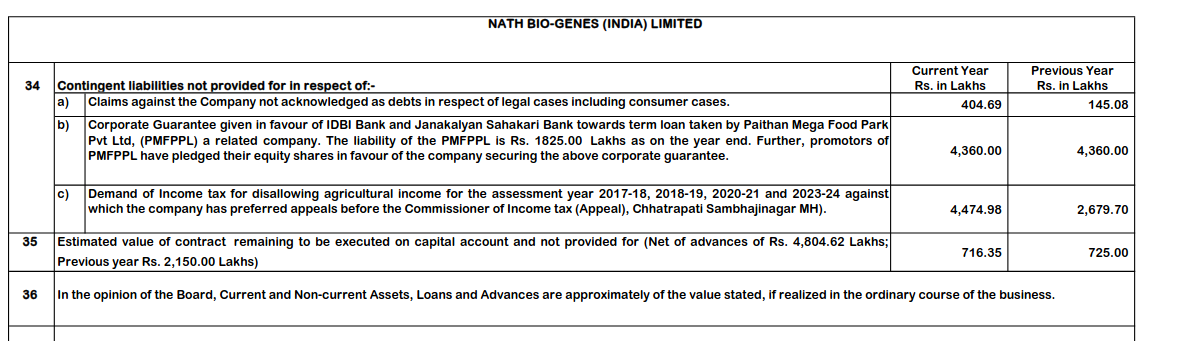

There is an increase in contingent liabilities from about 77Cr to 97Cr. Out of this, 43Cr is income tax demand for disallowing agricultural income.

Why did management not publish any presentation after the Q1 25 result or make any

concall?

Anyone tracking this company? Valuation is quite attractive at 9 TTM P/E. Aditya Birla MF is exiting - hence selling pressure. Guidance of 15% growth seems achievable - reported good growth in other segments. Margin is the only concern to me. Views please.