Very good point made by you. Can you please share some links as well. Since I have not found any adverse effect of management decision on Google.

About the fund raising it is mentioned that the fund will be used to manage long term working capital requirement. Which I believe a good move and in fact will improve the capital management where the debt to equity ratio will be balanced.[Since you know most of the capex done till today are debt funded]. So this will not only give a balance to the working capital requirement but also give safeguard to investors money at the current level because the warrant convertible value is Rs 200 per share.

What I dont understand (and the forum can help me with that) is if they did want to convert black to white why issue warrants, why not have these firms buy stock from the market. It is a fairly liquid stock with a lot of floating stock available.

That way they can get this for much lower price and dont have to pay for the 100cr upfront. Any ideas?

PS: No current investment. Tracking and interested.

First, its my personal view on conversion of black to white.

Second, company can buy back its shares from the market and for that company must have cash (which is white). So, how buy back convert a black to white. If you are trying to say, that a third party might start buying from the market, yes likely possible…but the risk of doing that is big…

check this video clip and you will get everything.

Something similar might be the case with this company. Again, see, these are my personal views…Its a bull market and every stock is hot buy…be careful…

Debt is taken under TUF. I dont think management will dilute their stake to improve debt-equity ratio, where in the debt taken is costing them much less than the cost of equity. Think of this, why would they dilute their stake and pay off the debt taken at 1% interest. Do simple google, add word fraud or like to your search and you will get the media reports. You will get atleast one media report every year saying - “Fire in the factory”.

Search fraud + shanti business school. Shanti business school is their arm.

Disc - I had started this thread, and I was positive on this company initially. After my research on this counter was over, my views got changed.

This is helpful. I do think we need to be extra careful in this (or any) bull market - especially in India where it is very difficult to actually find out about the company (it seems US is catching on with multiple scams of their own like Wells Fargo!!!).

But it does not still help clarify why go out and issue warrant when you can do the same by buying stocks from the market at the current price (about 40% less than the warrant) issued. I do understand that there are some shady dealings the promoters might have done but my question is actually independent of that and is more to try and understand why one vs. the other.

I sincerely believe that in companies in which one is not confident about the management’s motives it makes a lot of sense to take away the profits instead of riding it. I was always cautious about this company’s management but some of the happenings in the last few months have weakened my confidence. Also, things are not adding up as far as meeting deadlines with related to expansion plan is concerned. It is very difficult to figure out whether capex is being inflated or not. On reading the annual report one will discover that there are various related party transactions also.

Therefore, I have exited this company. Due to low purchase price, I was able to exit at a healthy return but I am sad because I wanted to hold this company for the next 5-10 years due to the robust prospects of the denim industry for the next 5-10 years.

I wish I had the conviction to ignore all the negatives but as of now I am not able to find enough evidences which could convince me to have a bullish view on this company. Even though we should be reasonable in our expectations of management quality in small companies yet one doesn’t expect an old organization to steep to the level of risking student’s career in the name of education.

Thanks for sharing your views. I continue to hold this counter for now and would only sell it if I see major red flags.

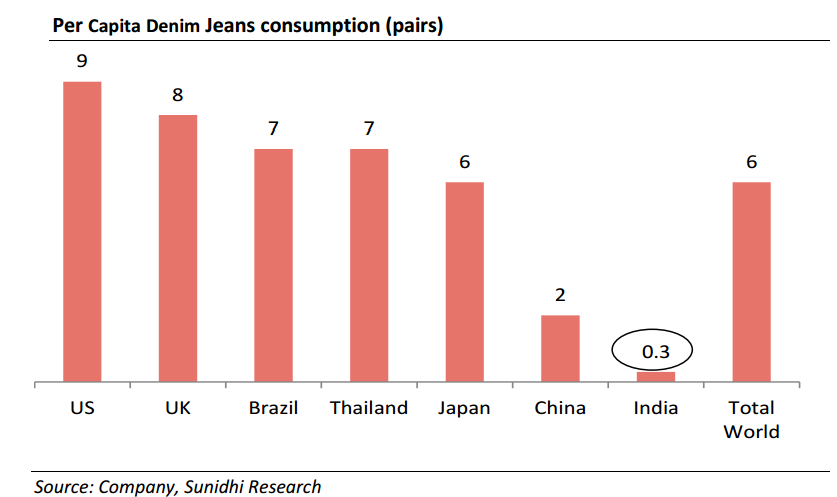

If I look at Denim Macros then India is under-penetrated in terms of denim consumption. With Middle Class rising and more liberalized work culture & dress code environment, I think it would have strong impetus for growth. Denim uses pattern in India is very asymmetric where Top 4 metro cities consume 37% of denim in spite of having only 4% of total Population while Rural India consumes 15% of denim in spite of having 68% of total population. So, with rural to urban migration, denim would have a strong growth.

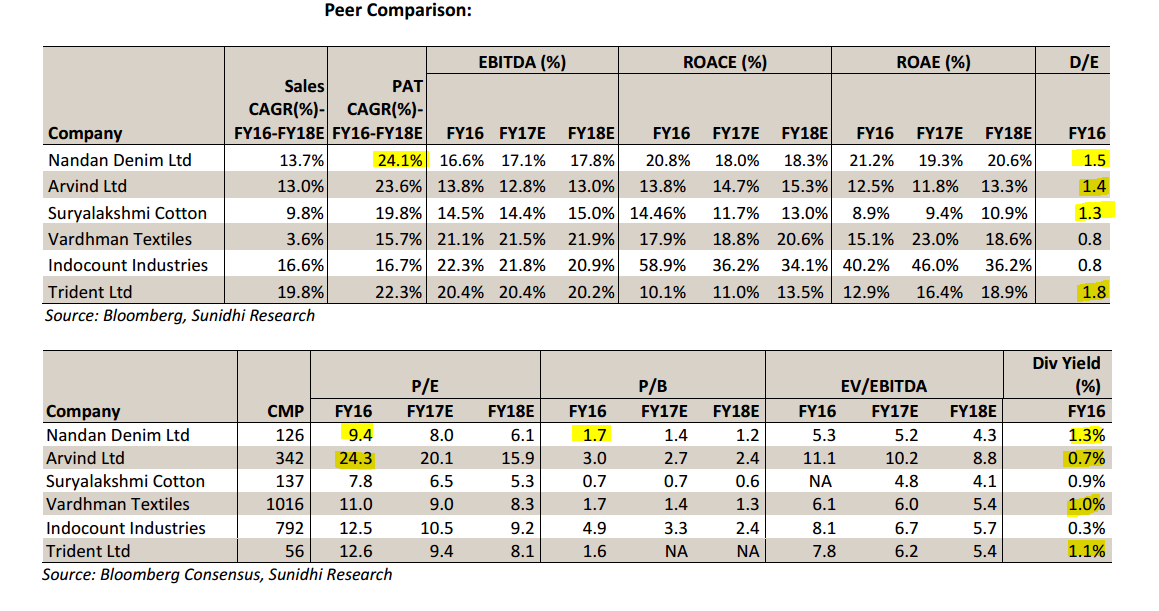

Peer Comparison

Nandan has D/E comparable to 4 out of 6 peers in the group below and trading at a relative low P/E. This is a capital intensive industry. I think Top Line should not only grow in line with Capex but on a more sustainable basis. Nandan is working on Product mix to more Value added products to ensure growth is sustainable. This is not a one or two year story.

There are couple of major risks. One is Management Integrity after some of the red flags raised by fellow members and second is raw material costs as Cotton is a volatile commodity. So, margins are not a guarantee. Any further red flags reported or seen in the press could immediately change my view on Nandan.

I agree the macro picture looks interesting. I thought of digging into this counter only after getting excited with the macro picture.

But two things from my side -

The above mentioned companies are not peer companies. There is no apple to apple comparison.

I saw the report, and shut it down after looking at the target price of 219/-

I wonder how can one forecast so accurate. He could have wrote 210 or 220/- Think over it. Should one then even give a second chance to the quality of the report?

Thanks for sharing this…My observations-

1). Company had already done 99MMPA capacity expansion last year…this year

they had to just add another 10MMPA if I am not wrong…then why was the top

line almost flat…? Only 5% growth…where we know that the industry growth

is 15%…correct me if I am wrong here…

2). Do we have any mutual fund holding here…it’s a 600cr mcap company and

funds like DSP micro cap would have got attracted to this company…this is

a unique co…this is a pure play on denim in india…no other company is a

pure play…this co has got no.1 position now…and the best part is that the

sector is growing at 15%…and the mouth watering part - it’s cheap in the

middle of this bull market…this should attract DSP micro cap or motilal

oswal also apart from the “well known” investors mentioned in the blog…I

have not checked this detail…so will have to check that out…Would just

advice to be cautious…

3). By the way did you search about the fraud that happened in their

educational arm?

4). I would like to share 10 more blogs written on the RJ website in which

the so called famous investors had entered and the stock is no where

now…ya it did went up first…

5). One good thing I learnt is about the art of rejecting…before .com

era, investors used to find it difficult to gather information…after .com

era investors are flooded with excess information…you should no what to

reject and what not to…I am not a master here and am also still learning

this…I would advise you to think over this…the report that you shared few

days back in your earlier comment was simply a summary of what is given in

the company’s annual report…where is the research in their report?

very good point mentioned by @abhishek90 … I was initially very bullish about this company but the top line growth was only 1.7% last 4 quarter so I don’t see it will get a double digit growth this year and with the industry growth of 15% if they are only growing at this space it is definitely cause of concern. Deepak Chiripal told ET that top line growth subdued due to less capacity but I don’t really think this is the case here.

Sharing excel sheet with peer comparison for Nandan Denim. Data for Arvind Ltd. is missing - if somebody has compiled this already please add it here, or I will do so in due course.

All numbers are taken from Annual Reports and ratios computed accordingly. There may be possible errors and members are requested to conduct their own due diligence in this matter.

Disclosure- initiated a tracking position in KG Denim with less than 1% of total portfolio.

So why is now the warrant allotment cancelled?? They say short term poor economic outlook…how will demonetization impact a denim business in long term??

This article says few FIIs invested in Nandan Denim. Are you saying that allotment has been cancelled and the confidence is not like before? Is there a way to confirm if the allotment was done or cancelled?

In Q4FY17, the depreciation was 35.3cr and Interest cost 12.5cr. As per recent concall co will pay around 48cr debt every year for next 2-3 yrs. If you extrapolate then interest and depreciation cost itself will be around 190cr in FY18. Where as FY17 EBITDA was 190cr. So FY18 PAT could be lower than FY17.

i) Any issues with this calculation?

ii) How much various subsidies that they have got will reduce interest cost which will impact above calculation?

Promoters are buying the shares from open Market in Nandan Denims. Astute investor like Dolly Khanna also holds 1.25% stake in the company.

Company is done with major capex recently and has shown good numbers in Q1FY18. Company is available in single digit PE. It seems to be a good buy.

be careful…

be careful…