Mudit, 10 years is not long enough for the Munger quote we are trying to fit in these scenarios.

This comparison is prone to starting and ending point bias. Prevalent market conditions can cause the CAGRs to deviate. Maybe 20 years is a better comparison period.

2 Likes

Interesting Q @Mudit.Kushalvardhan

Such correlation is observed in most stocks like Infy, Wipro even with Apple, Goog etc. However, some are God-gifted like AP, Pidi, Nestle etc. PE expansion went beyond reasonable duration, more than a decade for some minute minorities.

Can we say mean reversion for PE contracted stocks? I have not studied it much hence can’t comment. But interested to know other’s views/data etc.

If I summarise my pov AP, Pidi are exceptional, may not have more such examples. On the other ends not sure whether muthoot does mean reversion…

1 Like

There are many reasons for that. Longevity of the business, sustainable growth, competitive advantage, market share, innovation in products, trustworthy and able management, other sectors not performing at the same time, institutional holding etc etc.

Often overlooked is the high PE period, when only a few sectors are relatively better performing, so many are flying to those counters where the activity starts and increase, safe haven buying. Look at Page Industries thread or other such threads to know more, such threads are great reads, because we get to see investors’ and outsiders’ point of view, optimism, biases, warnings everything exists. Some threads in VP are filled with such knowledge that they are no less to popular books of investing.

And of course the fall of PE, reversion to mean or sane levels will also have the reasons, institutions find other counters, increased competition, management’s guidance misses, turnaround of other sectors, so inevitably the high PE wont sustain if there is materialistic impact on the business, and it falls, or at least goes into time correction.

Not to mention the obvious that each company is different, and some stocks defy and sustain such elevated PEs, if not go even higher.

I am yet to experience everything said above, because I did not get the opportunity to experience all of it. Hence bull and bear markets both teach a lot of lessons.

1 Like

Muthoot Finance is interesting now.

20% plus profit growth

Good corporate governance

Diversified geography

Market leader

And most importantly, at current market price it is likely to give 20% cagr for the next few years.

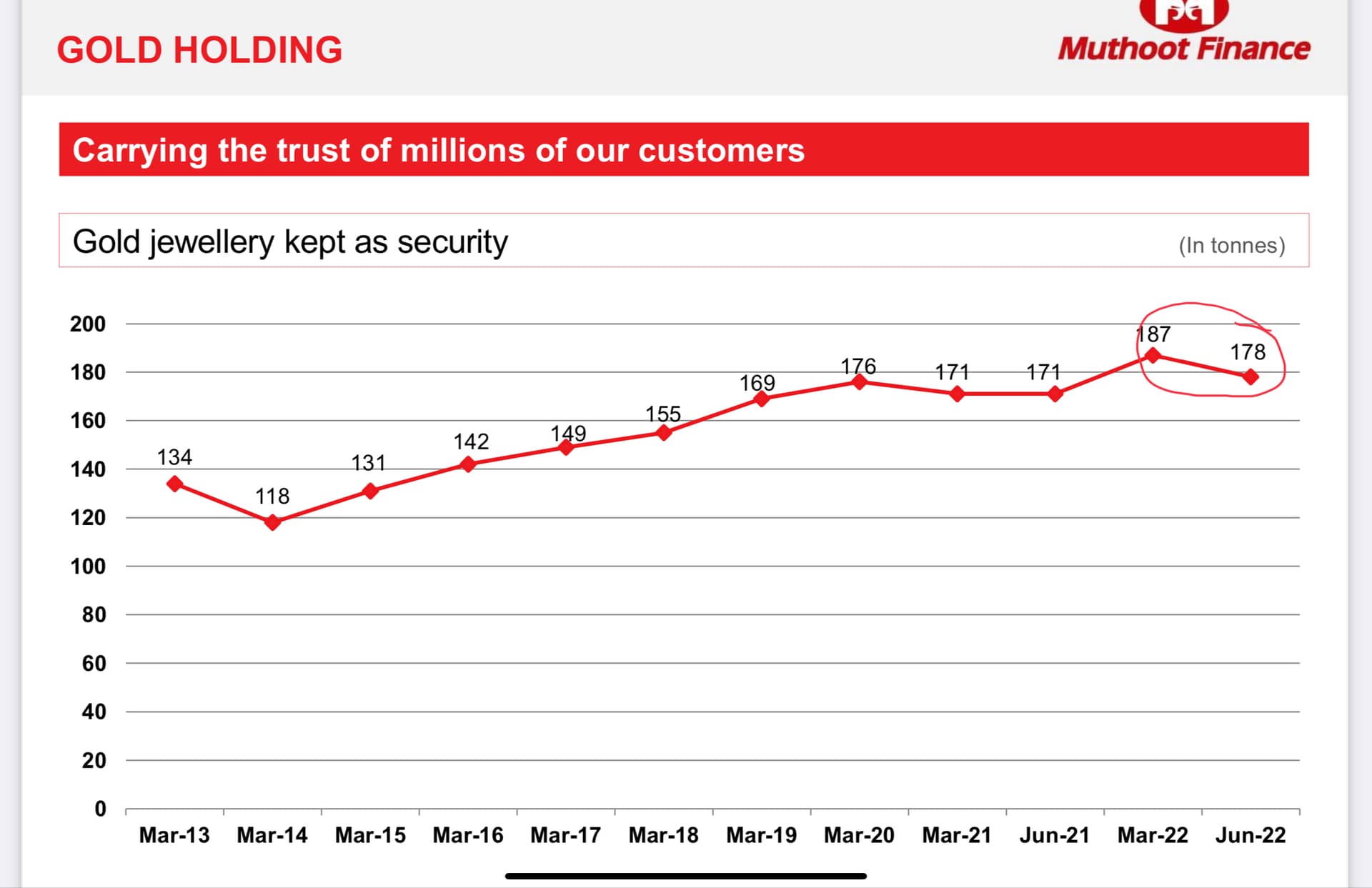

Correlation between its price and Gold price is high. Gold chart is non-threatening.

1 Like

Hi Vansh, is there a location for getting structured quarterly data that you use?

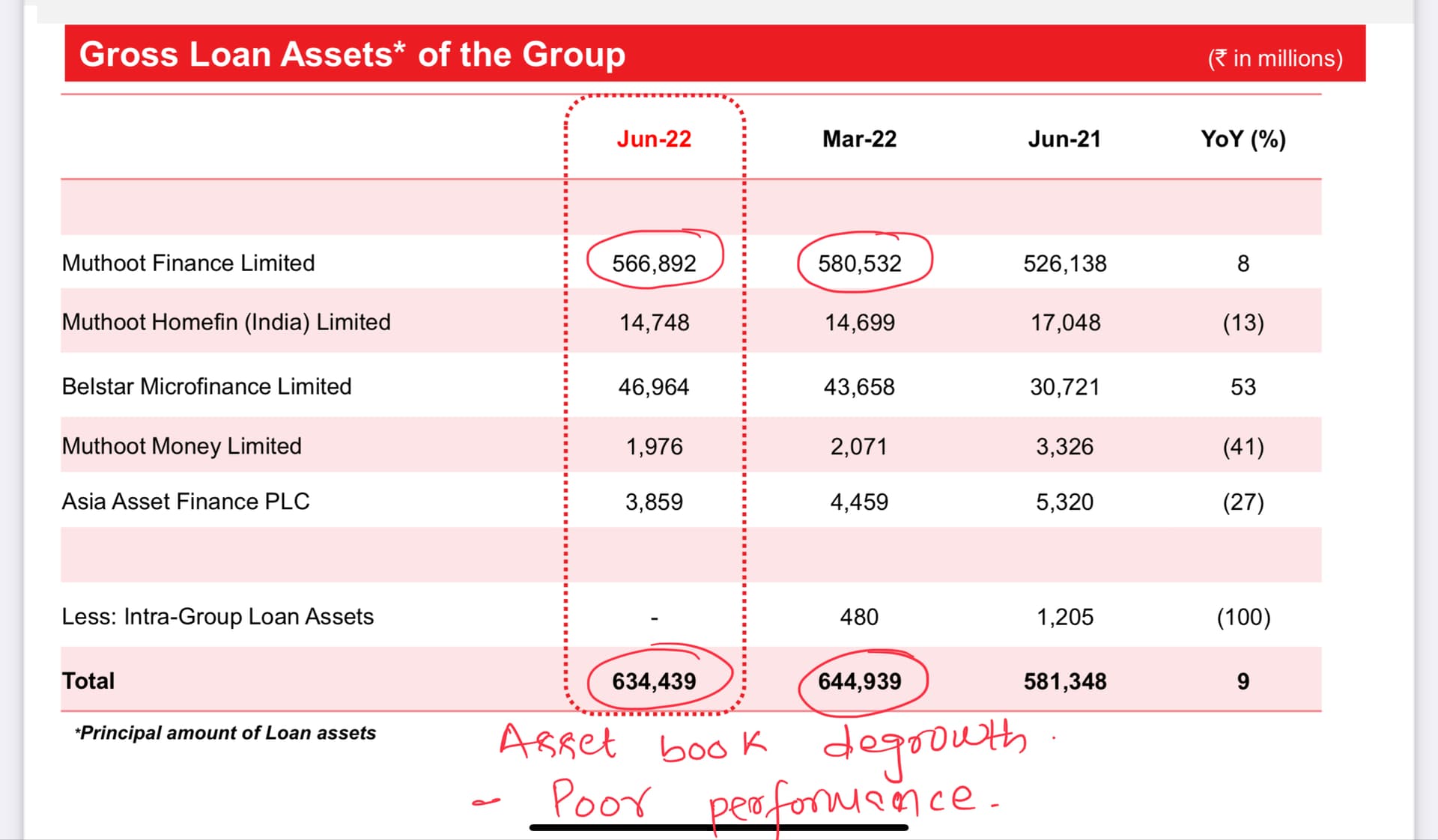

Clear sign of stress due to banks venturing into gold loan.

Disclosure: Exited long back.

1 Like

The customer base for Muthoot and Banks are different. The ones who can do the due process, would.never go to Muthoot.

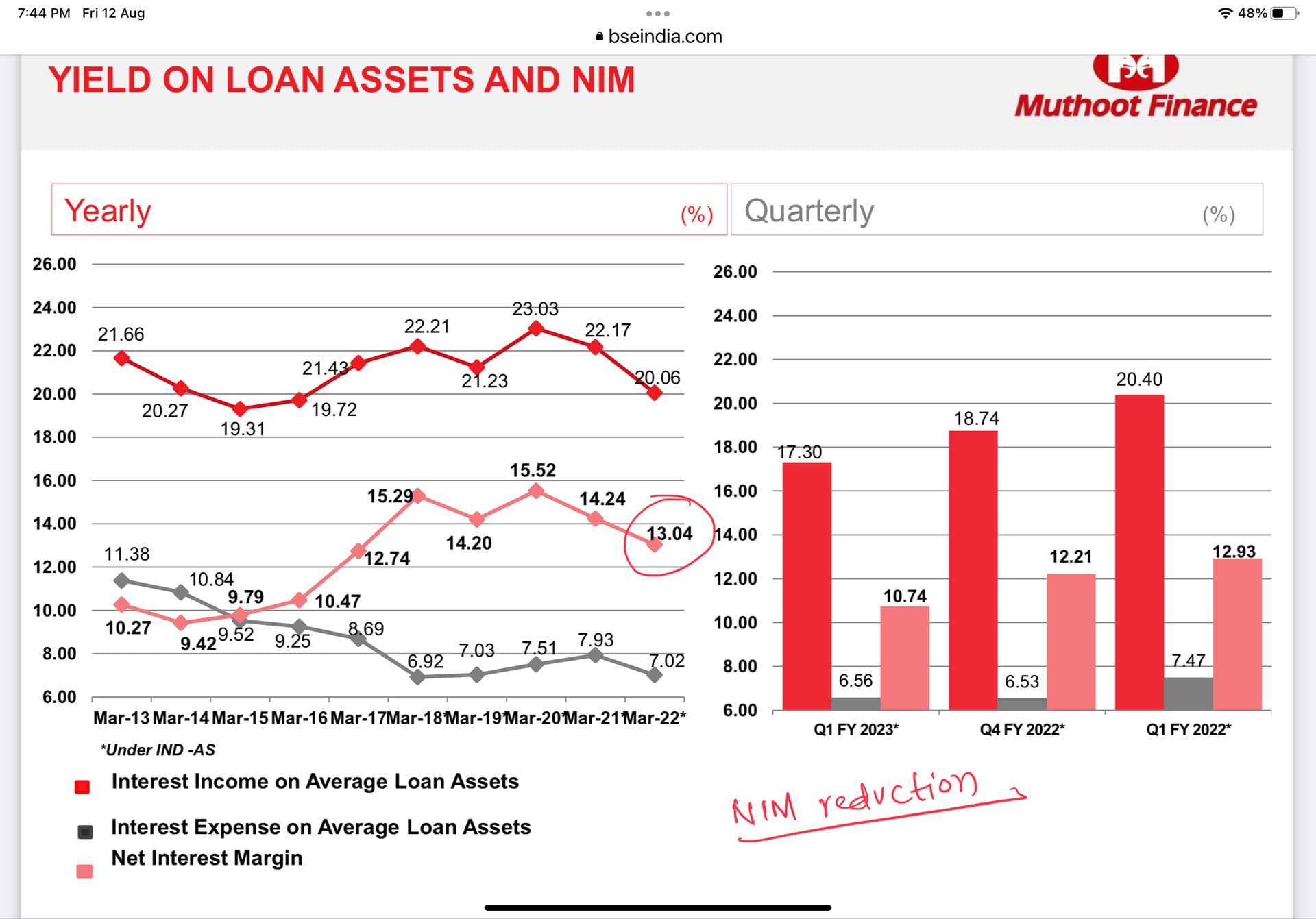

Average lending rate is 20%

and NIM is 13%

A quarterly dip probably won’t make a trend. And that weakness is now discounted in CMP

6 Likes

Hi Naman,

I used investing.com to get quarterly gold prices, and that’s the easy part. For company’s quarterly revenue numbers, it took me about half an hour to jot down values one by one from past quarterly results.

1 Like

Why can’t banks cannibalise Muthoot’s customers? Is there a regulatory requirement for increased customer verification etc. by banks?

1 Like

Yes. Norms are stricter for the Banks than they are for NBFCs. Due to this, inspite of being able to offer lower interest rates, banks have a smaller market-share.

The situation has changed considerably. Now banks are giving nbfcs run for their money. People also understood the interest rate difference. Nbfc won’t be successful in gold lending. I’m telling you this because I’m a banker. In our bank a customer will get money in 10 min from the time he entered in bank premises at 9 percent rate of int. Banks are focusing alot in gold loans.

4 Likes

There are mortage lenders that give these gold loans at obscene rates, and moreso the terms.

Those very same people who used to go there now go to NBFCs and are charged half the interest rates.

Sure, the ones who can open a bank account will prefer banks.

NBFCs are going to do just fine because their business is dependent on the “black” money part of the economy. Folks who pay nil IT return, cannot go and deposit gold into banks and do the entire paper work. Just won’t work.

I feel, as long as a strong parallel economy exist in India, gold loan nbfcs won’t struggle for growth.

Repayment options are convenient with nbfcs. They require only interest payments. Banks require principal as well.

Fintech disruption is also at play.

3 Likes

@Vikky9995 @jamit05 - which customers can get gold loans from the nbfc but can’t from banks?

I am no banker. Yet, my 2 cents.

Ones who do not want to

*pay principal amount in emi

*Open bank account

*Show/Have income statement

But, they have gold jewellery, which is a big population in agri, textiles etc.

People have to open bank account and show income to take gold loans from banks? Why? IF this is a statutory requirement, Muthoot has an amazing long term franchise? I really like the management and the business, just scared about the structural disadvantages of being a non-bank.

That is incorrect. People who have black money don’t need loans at all. What you are saying is the informal economy, and majority of the people who are part of this economy, who don’t not fall under the IT radar don’t have black money. There are crores of honest people who earn less than the basic exemption limit, who don’t have PAN, even a bank account, and don’t even know that IT filing exists. So these people may have started visiting NBFCs, knowing the interest rate differences, and I don’t know what kind of checks the companies have in place before disbursing loans.

And I guess, these are all fragmented businesses, there may not be stickiness too, unless they repay the loan quickly, need a loan again, happy with the experience they have had with a company, approach them again for the loan. I don’t know if companies keep track of all of this data and analyze it.

Not invested.

There is a whole parallel economy.

Small to big, all kinds of people who don’t pay taxes, evade or circumvent, have cash stashed or converted to gold jewellery.

Now, this is a huge population. All dealings is cash. Cash in cash out. And when they need money, for an expense, like house renovation, marriage etc, where do they go?

Fruit, sabji walas, food stalls, cleaners, daily wage workers… And even small scale businesses like haircutting salons, shops etc.

NBFCs is where they go.

Deposit gold get the money. Simple.

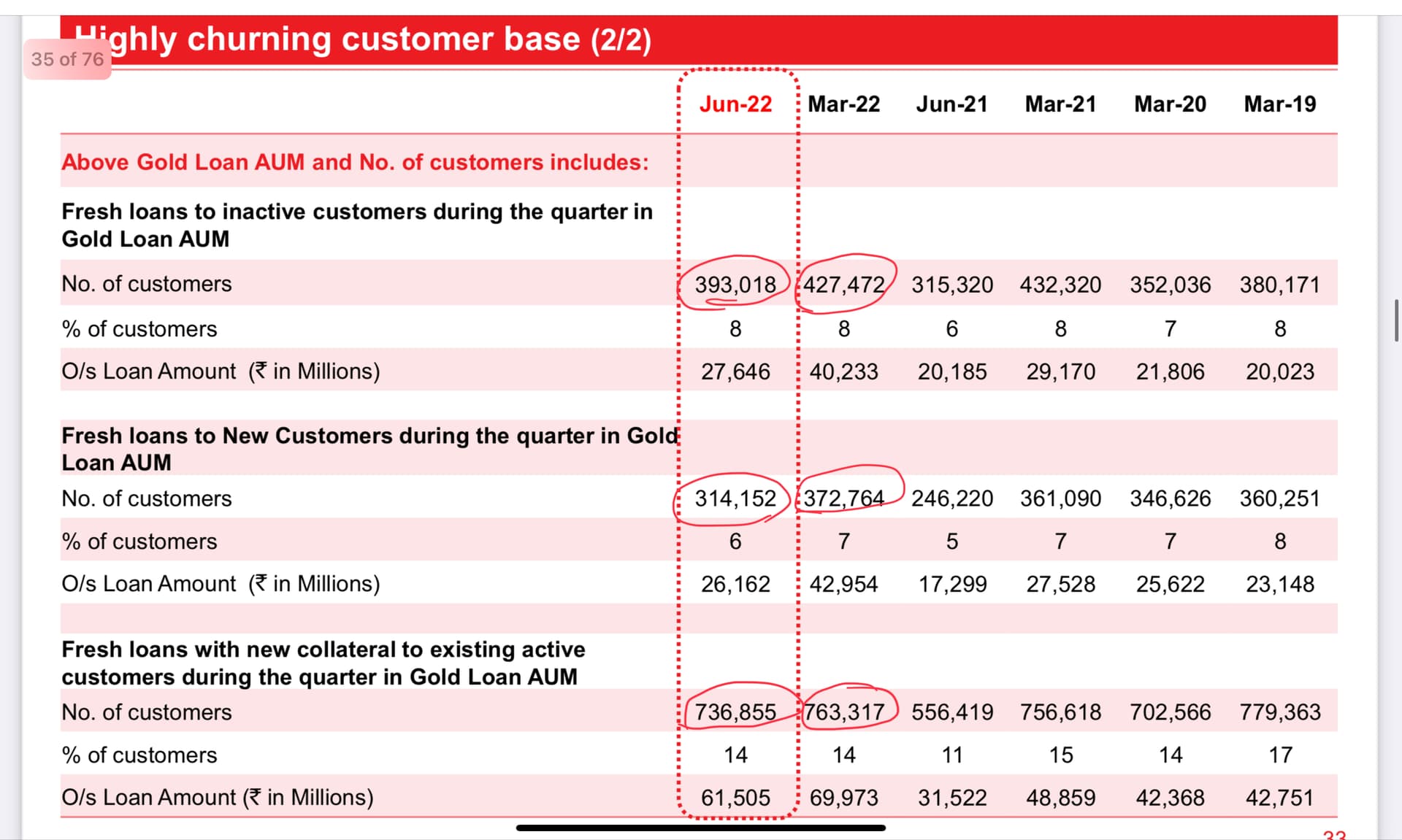

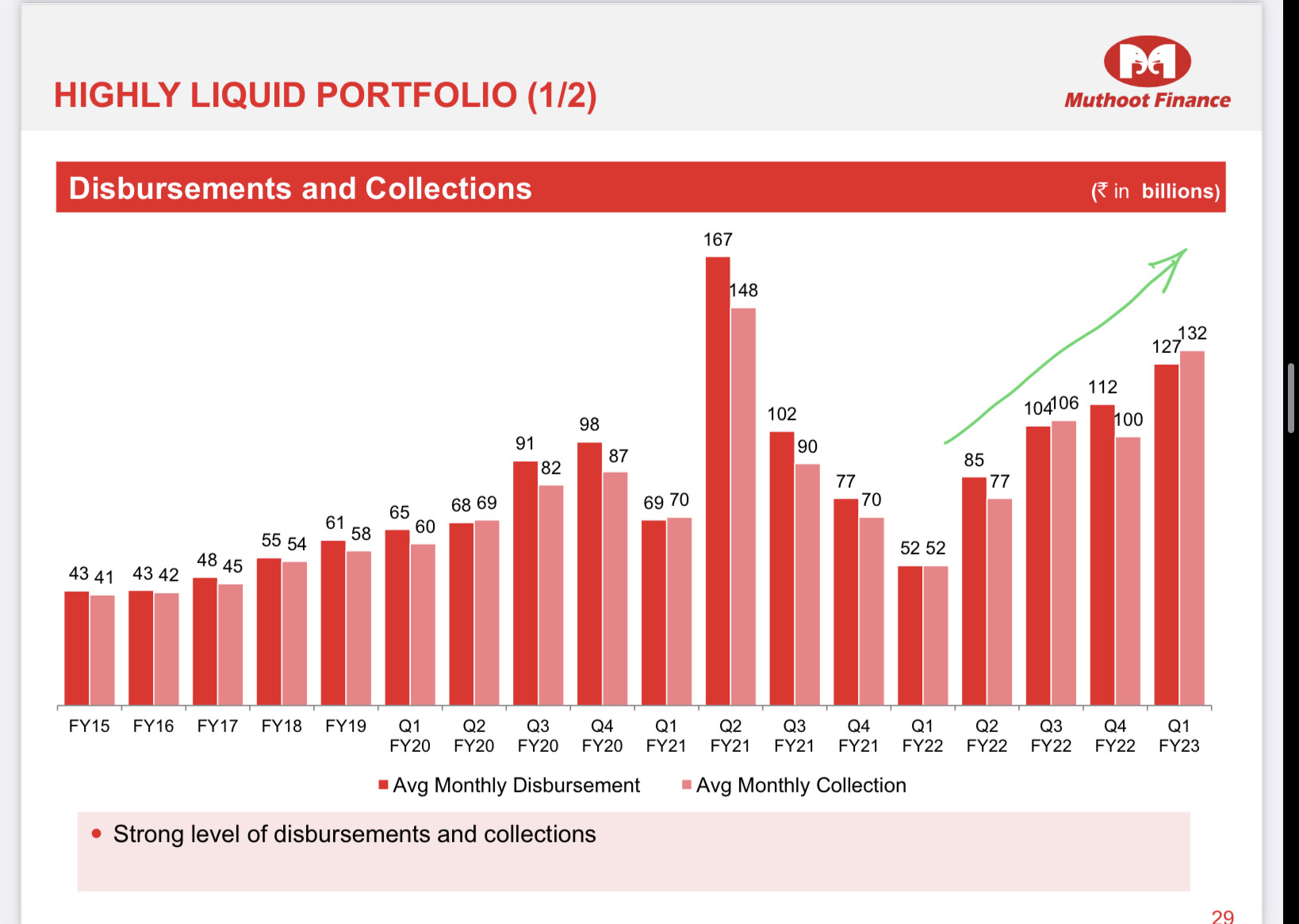

Therefore, a dip in numbers that Muthoot saw this quarter doesn’t worry me. There is a huge population who needs their services.

Besides Muthoot is only 66K Mcap. Long way to go. Plenty of headroom. It is a market leader.

Growing branches every year.

2 Likes

For all the people her ei can say is the days of nbfcs are over. Even the PSU banks are pushing their employees agressively to sell gold loans and credit cards and other insurance products. Except the Bajaj finance there is literally no hope for any other nbfc to become a gaint. This is evident in the valuation they get in the market. These companies shares didn’t move anywhere in the last few years and they won’t go anywhere in the foreseeable future. I request the boarders here to be realistic and ask themselves if they want a gold loan will they avail from a bank at 9 % or will they go to nbfc and get it at 20%. I request them not to give silly reasons. People have become more financially aware and this is irreversible.