I wish i had read this book earlier. This book is a compilation of selected essays written by the team of Marathon asset company for their Global Investment review. The book though a compilation of essays, is very easy to navigate. It is written in a very lucid and fun to read way and is filled with lot of examples and case studies which have immense learning value.

This book is like getting into the drivers seat and provides very precise/clear information to understand how various capital cycles work and where/how should one look to make better informed investing decisions.

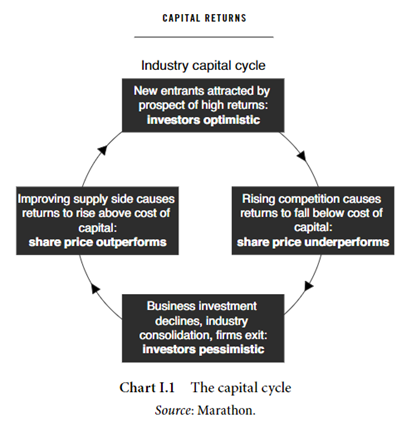

- Typically capital is attracted into high-return businesses and leaves when returns fall below the cost of capital. This process is cyclical in nature-there is constant flux. The inflow of capital leads to new investment, which over time increases capacity in the sector and eventually pushes down returns. Conversely when the returns are low, capital exits and capacity is reduced and over time after consolidation profitability recovers “creative destruction”. This beautifully explains the natural cleaning mechanism of any sector/industrial cycle. One is also forced to focus more on the supply side for determining future outlook of the sector

- This when combined with porters famously discussed five forces can give a investor a detailed overview about the competitive advantage of the business.

There are lot of examples from indian context which becomes easy to understand if we can apply where the industry stands from a capital cycle point of view and how is the future supply going to shape up. Few which readily come to mind are telecom, real estate after the boom of 2008 and also the nbfc crisis of 2018-2019 ( though credit cycle has its own nuances but is cyclical in nature). - Few red flags for over supply in a industry/sector are frequent IPOs, M&A , increased capex along with rise in debt during the upcycle. One should be wary of management who are not aware of the capital cycle of their own industry and hencetend to mis-allocate capital, vice-versa one should try and be with who are aware of capital cycle and are good capital allocators and mostly invest during a down cycle.

- Chapter 2 tells us why we should not even consider accounting metrics like PE etc for valuing a company. Our focus should rather be on strong competitive position,network effects, pricing power,differentiated/low cost product and economic moats. such companies deserve high valuations than avg. This coupled with industry tailwinds can provide a real good ride into wealth creation.The value/growth dichotomy is false, rather we should focus on future earnings growth.

- Chapter 3 focuses on the management quality and attributes. The management should be aware of the industry capital cycle,should allocate capital in counter cyclical manner (raise money via equity sale in upswing and capex in downswing), has large equity stake and is dispassionate towards selling assets when someone is prepared to overpay. The incentives of the management should be linked with long term fundamentals of the business. It is very important to gauge the work culture in the company, ability of the management to accept mistakes and competitors. They should be modest and conservative and during concalls or agm should be willing to answer queries (better if it comes from the ceo/md).They should not be fixated on the quarterly EPS game and should try and comment on the shaping of business environment.

- Chapter 4 is about accidents waiting to happen. here they have mainly covered the anglo irish bank (yes bank in indian context) where in the management was justifying taking on risk without due diligence. The quality and value of underwriting was not good and bank was rather focused on growth and generating profits.

Other evidence to ascertain market froth are also discussed like:

Commodity bubbles, PE mania (overvalued deals), IPO frenzy, M&A Mania ( without logic or value accretion) and finally the retail exubernace. This chapter also has a very good essay in the end about about how a good financial/bank should operate or how can one spot one. - Chapter 5 is about the " The Living Dead". These are the industries/sectors where the natural cycle of creative destruction is not able to take place either due to avb of cheap capital or due to intervention of policymakers. Brings out the importance that excess capacity and weak profitability should be addressed. They explained in detail how policy intervention and quantitative easing in japan since the 1990 has resulted into poor corporate profitability along with growing debt burden. Is the west also heading the same way…sure looks like that…?

- Chapter 6 is about why they have been averse to investing in china. They have always been wary of investing where the formation of fixed assets are on the higher side. China also suffers from misallocation of capital due to avb of cheap capital for long. Other factors one should lookout for is that the State should not interfere too much in the business ecosystem, the chinese companies have lot of interference from the state, so much so that during the IPO the state would help the companies to dress up profits and assets.

- Chapter 7 is the final chapter which is mostly fun to read and comprises of satirical fictional essays about greedy Inv bankers , poor corporate management etc.

Regards

Divyansh

PS: Book reviews by various members (specially @phreakv6) pushed me into making an effort. It helps me in rereading and recollecting along with focusing on the main/important content of the book read. Please do add/correct if someone else has too read the same book.