In my portfolio , I have only 3 small cap stocks

alkyl amines, KEI and Mold-Tek-Packaging, and even out of these , I am contemplating about selling alkyl amines, so I can safely say that my change of strategy has nothing to do with small cap companies performance. You are right, they will average out.

Rather I am not at all confident about finding good small cap companies which I can hold for very long time, without losing my capital. Precisely for that reason, I am investing in small cap through active small cap mutual funds. I am AMFI certified advisor from 2005. So i have seen the small cap mutual fund performance from last 18 years from close quarters, and I know these AMCs have resources to find such small companies and study them better. We dont have that much resources as well as reach to management. But of course, this is not the right time to invest in small cap funds. These funds themselves give us a hint to stop investing into them, when they stop Lumpsum investments and start accepting only through SIP. Going forward returns will revert to mean.

My reasons for selling : -

-

Hindustan Unilever : - Sales are growing at 10-12%…profit at 13-14% and stock performance is pathetic at 7% in last 5 years. even if it revert to mean in next 1-2 years, still its long term returns are below even our normal Index. It doesnt fit into a growing business definition. I am ware that 9 out of 10 households use their products. But its not fit to give 18-20% CAGR over next 1-2 decade. Just holding it because its household name, doesnt fit into my scheme of things.

-

DMART

Celebrated Retailer with huge respect for promoter. But what are its numbers saying? Sales are growing fast, in last 5 years, almost triples. Net profit in last 5 years, almost 3 times, but stock performance has not been in line with its business performance. its barely double in last 5 years at CAGR of 17…and going forward with retailer competition increasing, dont know whats going to happen…Still I have not taken any final decision on this…Question Mark -

Infosys

In last 10 years, profit just tripled. Already given the reason. -

Balkrishna Industries

sales OK between 15 to 20% CAGR range but profit is pathetic 11% in 10 years and 7% in 5 years, ROE not crossing 20,Stock performance has been good…but since not backed by business performance, very high chance of dismal performance going forward -

HDFC bank

already reasons given. -

Deepak Nitrate or Alkyl AMines ? one among them…still not sure

-

Laurus Labs

already reasons given

Once the reshuffling is at least almost complete, I will post my complete new portfolio

Uno minda net profit margins are between 8- 12% only ( mentioned on concal)

Worst case 8%

Normal case 10- 12 % I think

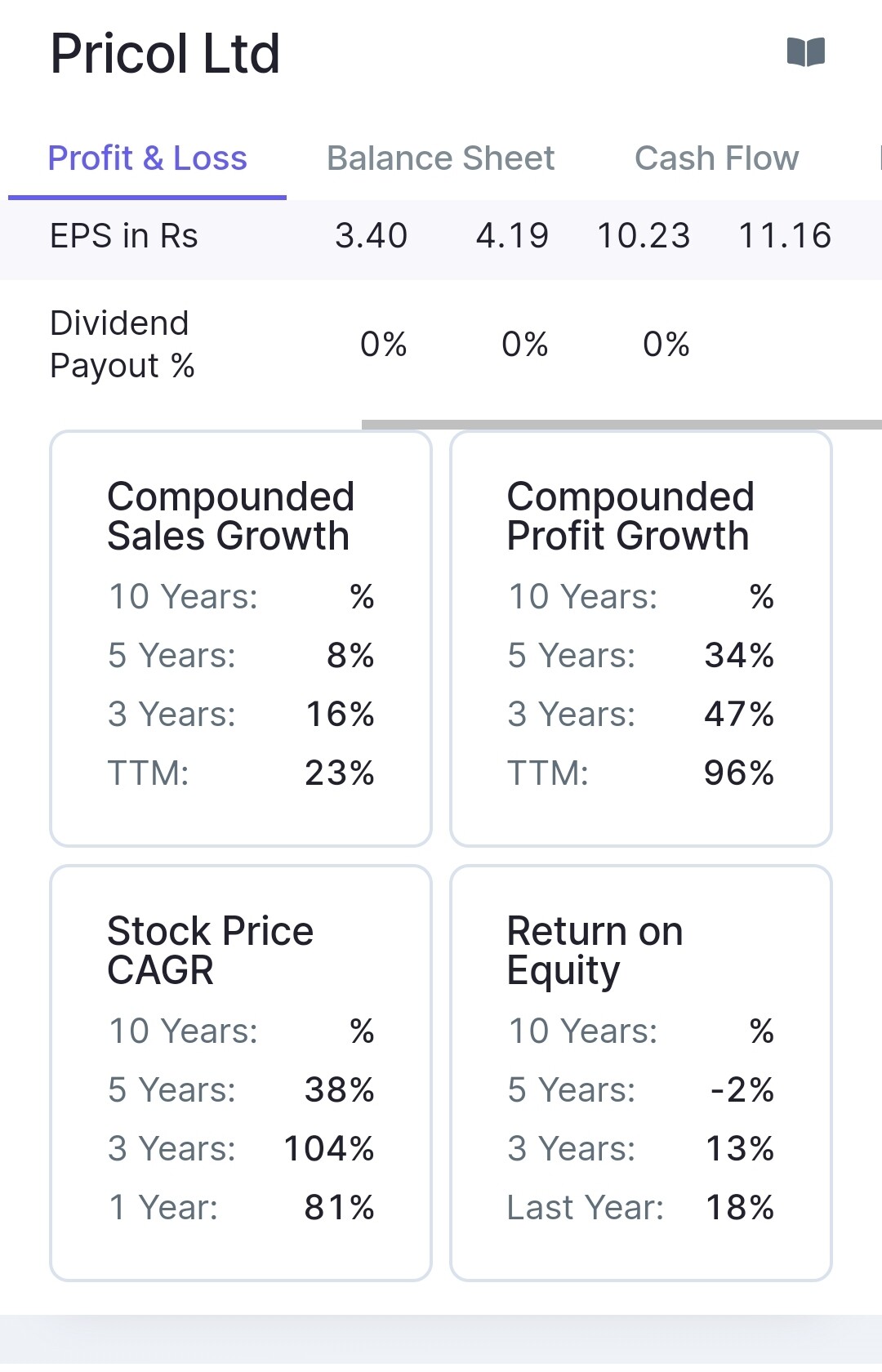

Please also study

Pricol and Fiem industries

UNO minda is ath levels , please do proper research before investing

Uno Minda is squizzed between two big Sharks. Their suppliers are also big Shark Businesses like steel companies and their customers are also big sharks like Maruti, Tata, TVs etc. So they are squizzed from suppliers as well as from customers for margins, hence their margins have been lower and it will remain so. But has that affected its Profitability or sales growth? Not at all.

see their sales growth , profit growth…its high growth company despite having low margins due to sandwitched between big players.

As aginst this, see Pricol performance

In case of Uno Minda, ROE is increasing while in case of Pricol, its been negative over 5 years.

Average 5 years PE has been around 50 for Uno Minda while currently its trading at same level.

Why not buy liquid bees to park cash ?

Its not about instruments…its about getting fully invested, so that money doesnt get spent.

Hi Mudit

I’ve gone briefly through this topic and could see how your stock preference has gone from low growth stalwarts medium (high?) growth cos.

Just curious how your portfolio looks currently. Could you pleas share?

Of course, I’ll not take it as advise to buy or sell. Just out of curiosity

Out of these, Infosys and Laurus Labs, I will be selling soon.

Why are you planning to sell Infosys? As I have a long term view on this…

I already have LTI Mindtree as well as Tata Elxsi, so I dont want to invest in IT more than 2 companies. Also i feel , in future, compared to these 2 companies, Infosys will grow slowly, is my assumption.

Thanks for sharing the PF promptly. I’d like to quiz you on your PF to understand your perspective.

- what’s the exit criteria for high valued stocks like Astral, Nestle, Asian Paints etc.

- why not Indigo paints instead of Asian paints? Indigo is cheaply valued relatively, have operating leverage paying out, Growing higher than Asian paints

- Why low allocation to SRF, even though it’s a large cap with low volatility (like nestle and Asian paints). It’s available at lower valuation for better growth rate. Why not shift some allocation to SRF?

-

No exit criteria . After reading the Pulak Prasad book, I am confident to become permanent owner and want to hold all my stocks forever. But of course, if any of my business performance deteriorates, and any scam happens, i will sell the next day.

-

Paint industry overall is undergoing a very big churning. Many players are coming with huge capacities and huge money as well as distribution capacities. Grasim is one example, pidilite another. Hence going forward, competitive intensity will increase a lot. This is pointing towards sub-optimal business as well as stock performance. Hence i sold berger paints. I was contemplating selling Asian paints too, but this stock gives stability to the portfolio, hence i decided to stick with industry leader. I added Mold-Tek packaging for this reason also as they are providing containers and packaging to all paint companies Asian paints, Pidilite, even they are coming up with dedicated plant for Grasim paints. So i will be in ancillary paint sector through Mold-Tek without bearing the heat of paint sector competition .

-

SRF i will increase the allocation . I dont like to shift allocation from one company to another. I keep adding fresh money to portfolio companies from my regular income. SRF ka number bhi aayega. Everybody will get their share of pie, but piecemeal basis.

I maybe wrong but it seems your top allocation bets have changed significantly since you started the thread… your thoughts must have evolved with time.

Would be nice if you can capture some main points learnt in journey so far which changed your top bets and even the overall portfolio with time…

Some of the previous bets are still there and in almost same weightage. Like Bajaj Finance, Divis , Asian Paints, LTI, Abbott , PI Industries, Nestle, SRF…

Only thing happened is, some like Polycab,Astral, Apl Apollo grew in size while i tried to remove some duplicacy like instead of 3 banks now only 1 bank. And NBFC also instead of 3 just 2…I had posted my portfolio exactly in sept 2022, 1 year is over, and i have tilted towards large and midcap growth companies more instead of only Stalwart . Thats a major change. Also i have decided to do on my own instead of mutual funds while in small cap space, i will go with mutual funds. Also i am.not locking any funds in Nifty and Nifty Next 50 Index funds

If you are devoting your time directly in markets than its important that you generate at least 20% annualized returns. Thats not possible with conventional approach which i have learned hard way. Let me give you an example, my absolute returns from Dec 22 which was peak till now are 75%![]()

![]() . 70% My holdings have changed every year. Top 5 bets always make 60% of portfolio. Juggling in small cap gives high beta, Force motors moved from 1300 to 3500, Kalyan moved from 110 to 228, AGI Green 300 to 750, recently bought SKM egg at 230 one month back which is quoting at 440.

. 70% My holdings have changed every year. Top 5 bets always make 60% of portfolio. Juggling in small cap gives high beta, Force motors moved from 1300 to 3500, Kalyan moved from 110 to 228, AGI Green 300 to 750, recently bought SKM egg at 230 one month back which is quoting at 440. ![]()

Laggards

AB Fashion, was largest holding in PF at 360, dropped to 220 still holding, capital could have been utilized somewhere else.

Keep 10% of your PF moving with small and stocks in news. Thats give u additional return generation capability.

Thanks for the advice. But I am not going to follow market movements much. I am determined to keep watch on business performance mostly. In that also i will be focussing more on small cap and midcap companies largely, and just a bit on large cap. Just to give an example, keeping close watch on Bajaj finance and ICICI bank type stocks wont make much of a difference, as hardly anything happens over a short period of time.

Uno Minda is sold after realising that Auto ancillary segment companies are in a very disadvantageous position with reference to margin, competitive intensity etc.

Uno minda is expending very fast, two new plant coming.