Yes. Even that also I am counting as a negative factor. All auto ancillary companies are so helpless that they have to go where big OEMs go. They have to put up plants near their OEM plants as these OEMs literally maintain zero inventory and work on Just-in-time . This is a kind of exploitation of auto ancillary where they have no say at all. Secondly , there always a chance that if an auto ancillary putting up a factory to serve a new location of OEM and in case OEM fail to get the market in this new location , they just close shop there. Then what happens to the newly put up factory of ancillary? These lose heavy capital. But who cares about them? I feel sorry for such helplessness of this industry and I dont want my portfolio company in this “bechara” category.

This can also be said about mold tek packaging in your portfolio. They are literally skimmed by asian paints and maybe now by grasim. Thanks to their fmcg division and upcoming pharma division they can think of surviving.

I think this is a good example of difference of perspective of types of investors. While some momentum investors might look to play capacity expansion like once capex done and OEM does not move factory meaning all things done and now time to ride momentum…but as you rightly said its lot to track and be sure of…variables are higher…

Very important here to know what type of investor you are…and i think you seem on right track…

I was thinking that this question may come up. I have given a thought to it. There is a fundamental difference between auto ancillary companies and Mold-Tek packaging. This difference you can see from their operating margin. In case of best company in auto ancillary, Uno Minda, still the operating margin is still around 10-11 while in case of Mold-Tek, its around 20. Mold-Tek may have influence of few paint companies from customer point of view , but they dont have supplier side constraints. And even from customer side ,they are trying to get free from clutches of paint companies , as u said by diversifying into FMCG and Pharma, and these new segments are at very high margins. Also if you look at competitive intensity, when u go into auto ancillary sector on screener, you get 108 just listed companies organised , and then you have thousands of unorganised , pvt.ltd companies. In case of Mold-Tek, they have some niche and nobody else has that, they are exploiting that. Recent example is that of Bar code packaging. So i have come to the conclusion that Mold-Tek is a good proxy for FMCG sector companies. Instead of Mota Haati like FMCG companies, Mold-Tek will be better to bet on for multibagger returns.

But offcourse , I would appreciate differing opinions to put holes in my narrative.

One more thing is I have consciously taken a decision to restrict the number of stocks around 20. This will help me to study and track them.in detail. Hence even if some companies are good ( like Uno Minda) I am purposely finding faults in them to get me an excuse to chuck them.

Mold tek did something serious, they did the equity dilution by huge percentage. How are you sure that they will not do the equity dilution in the future?

Do you know the reason why they landed in a situation where to grow, they had to dilute the equity?

While all of this is true ( I read it before in Vijay Maliks blog), there is another factor at play that might make even bad or gruesome businesses great investment . Since most auto ancillary companies suffer from these issues and auto industry is cyclical, during bad times big fishes swallow up small ones and big becomes bigger . After they reach a critical mass,the aquisitions drive the sales and profit .If this happens then this company can become a huge multibagger . Example is Motherson Sumi between 2010 to 2016 or so . Thats why they are still the darling of many and they still buy companies left and right if you check ther BSE declarations. .

I think here in VP, there is another post that explains this better …probably in the thread of Suprajit . Minda had crossed that threshhold already last year

.Hereon , the growth will be mostly by inorganic means and so its much more unpredictable than simple capex and op lev calculation.Anyway I do not have any Auto stocks either … so its all just theoretical . ![]()

Latest Activity-

-

As decided earlier, sold Infosys completely. Now in IT, I have only 2 companies, LTI Mindtree and TataElxsi.

-

Decided to purchase IDFC First Bank, …by buying IDFC ltd, using reverse merger. Today bought few quantity of IDFC ltd. Incase their reverse merger doesnt materialise, then will directly purchase IDFC First Bank instead of indirect way and sell IDFC ltd. If everything goes through, i will get IDFC bank shares in their ratio of 100: 155

Portfolio Update :- Started accumulating Max HealthCare…This is my only hospital company.After studying the hospital sector, I had finalised 2 options

Max Health Care and Narayana Hrudyalaya…But ultimately chose Max health Care for its growth trajectory and being more aggressiveness. Soon will post latest portfolio after recent changes.

Rationale Behind adding Max HealthCare :

- In healthcare I have 2 pharma companies Divis Labs and Abbott India ( Laurus Labs , I am going to sell soon), but I didnt have hospitals or diagnostics.

If you can notice, I want to reorient my portfolio towards consumer centric with more companies from B to C rather than B to B. Hence recent additions like IDFC, Trent, Nestle, Titan etc, So in healthcare I wanted to add Hospital company. - Hospital Industry is a capital intensive business , so it acts as a moat and strong entry barrier.

- Hospital business is very secular in nature, with complete disregard towards macroeconomic situations. Whether economy is in recession or in boom, if someone needs dialysis, once in a week, he has to do it, no matter what. Bed capacity , GDP expenditure on health is very low , so long runway for growth. there are 10 more reasons for visible growth in this sector…But I know you get it.

- Why only Max health? why not Apollo or Narayana or Rainbow?

Max Health has highest revenue per occupied bed and also the occupancy rate is high compared to peers. In hospital business growth comes from acquiring other famous and matured hospitals or taking on lease Trust hospitals and I feel Max Person is good at this game . He has proved it many times, Their expansion strategy is aggressive compared to others. Being secular nature of business, this will also give stability to my portfolio. Again there are many reasons…But this much is enough. I am not a “Baal ki khaal” person. If something appears approximately correct, not precisely correct, I go ahead with it. After all business lies not only in screener… There are many qualitative non-screener attributes to each business… Open to critical opinions as always.

Technically forming VCP with strong RS. Max Healthcare looks technically strong in the present scenario.

Disc: Not Invested

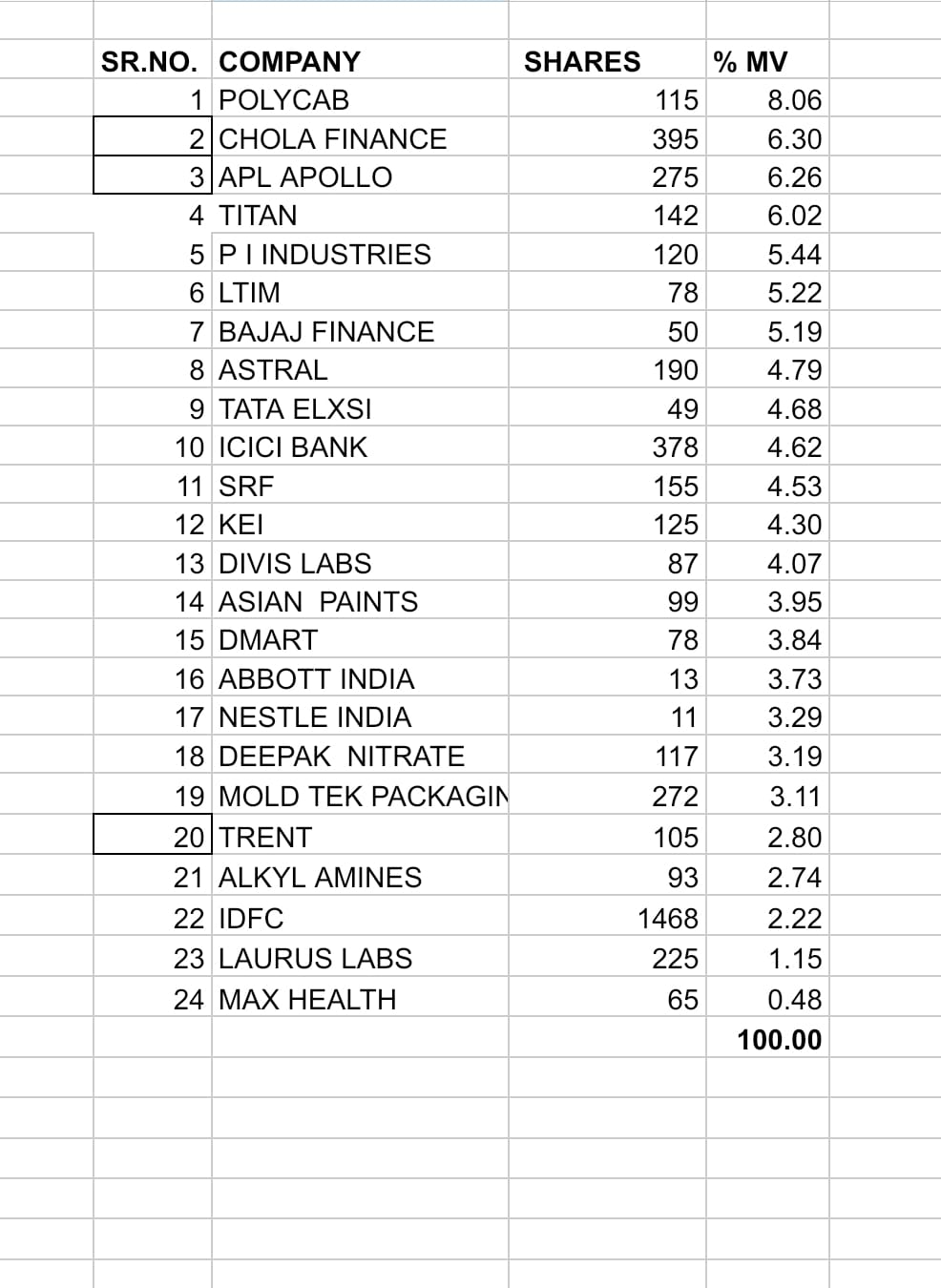

Any Particular reason to have both KEI and Polycab.

There is overlapping between two to some extent. But KEI is having larger Institutional share in business while Polycab becoming more of a Business to consumer company. So I wanted a bit small and more aggressive company. Polycab I have recently entered, so I missed the opportunity which was 5 years before, while I feel KEI is at same growth stage where Polycab was before 5 years.

Point 1

In customer facing business, I think customer orientation is most important. (Ref : Jeff Bezos)

Each high flying company will close down if they don’t focus on customer.

One way to check the customer reviews is through the google reviews.

Try checking it for the shortlisted candidate of hospitals.

Point 2

I think max is trying to do horizontal progress in healthcare which I feel is not too beneficial in Indian context.

Narayana is a disrupter and is actually trying to solve the customer problems while maintaining growth and profit.

From Zero to One

In business, horizontal progress happens when a startup takes a product that is already available and improves on it incrementally . Vertical progress is going from zero to one. Vertical progress is the creation of something unique, some technology that no one has ever thought of or developed before.

Hi…What must be the zero to one initiatives that Narayana is taking? If you could elaborate…

Thanks for the response. However and this is just from a small part of research, the entire so called FMEG and small FMEG space is extremely competitive. Look at sheer number of companies trying to build a B2C business here. 10 years back what was a 3-5 major competitors for every appliance/lighting system is now 10-15 competitors.

So While growth outlook appears rosy given higher units per home+ increase in number of homes i feel margins will be extemely thin. Would love your read on this.

Both polycab majorly and KEi entirely are not FMEG companies. They are major cable companies. You are confusing Havells and Crompton Greaves with them. Or am I wrong?

No You are right on historical and current basis as they are predominantly W&C business, however both companies have stated ambitions to grow in FMEG, Just attaching todays polycab PPt . H1 shows the fmeg business at approx 650 cr. which is approx 9-10% of total H1 business. PowerPoint Presentation (bseindia.com). Have not checked KEI but i remember they stated ambitions in this areas also. My comment was focussed on this point only. And look at competition concerns both Havells and CG Consumer are facing.

However this is not to comment on overall franchise of both companies where predominanly copper and maybe crude prices will play major role. I have no idea when you bought both but at current prices they are priced to perfection.

No outlook on future price movement also however both companies should do well seeing the uptick in Infra and RE.

Before starting, I want to give you a disclaimer that I can be completely wrong and hence take it with pinch of salt.

Point 1

No one focuses on giving affordable procedures and surgery. When you have decided that you will not earn by increasing the cost drastically of the procedures and surgery, innovation needs to happen to increase profits and maintain growth. No one talks about the affordability in hospitals except Narayana Health.

It is not all talks, Here are my reasonings(still in analysing mode though) →

- They increase the surgery per doctor to compensate for the increase in cost.

- They have new inventory management to reduce costs.

- They are using technology and introducing apps to make the nurse and other employees productive.

- They are introducing apps to streamline certain manual processes and their app is getting adopted with positive reviews. For reference comparing the reviews of app of max and nh.

Ref → Finology article

According to me the hospitals should remain affordable for direct patients as even if you have the policy the claim settlement ratio is not healthy in many insurance companies and even most people don’t have health insurance.

Here are the claim settlement ratio for the few insurance companies(Source : Ditto)

Start Health → 83.07%(average of last 3 years)

ICICI Lombard → 86.67%(average of last 3 years)

Niva Bupa (erstwhile Max Bupa) - 90.74%(average of last 3 years)

Point 2

They have not stopped here and they are testing to bring the clinics for the primary care(something new done by private hospitals I guess).

The are also thinking of coming with heath insurance.

Final Note

It is like they really are looking to solve the most important problem for the humans, the healthcare at the affordable rate. Until and unless it does not impact their profits and growth, I will prefer the NH any day when compared to the Max hospital.

The zero to one that they are doing is trying to provide healthcare at the affordable rate by being profitable and showing growth.

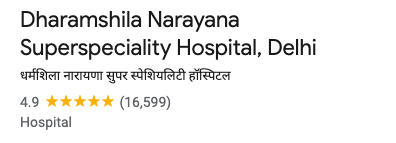

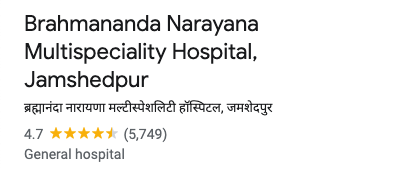

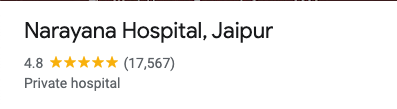

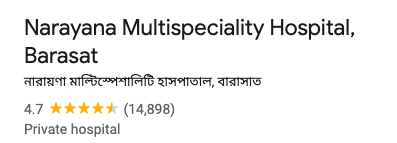

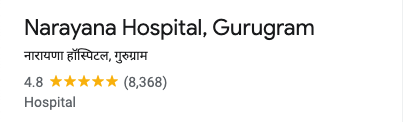

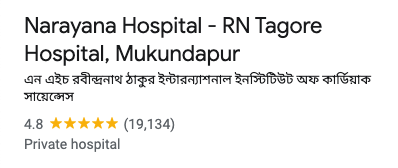

Reviews of NH hospitals on google

Reviews of max hospital

Please check the reviews of the Medanta and you will be surprised.