Results on 21st August.

Q1FY19 result out.

Presentation https://www.bseindia.com/corporates/anndet_new.aspx?newsid=94739cdd-179a-4f23-8378-e9d371f0c15b

I was not able to find the PL statement for Q1 results on BseIndia.com

All around good performance except housing which was known. I think few more quarters of high provisioning in housing fin. is left. Accounting treatment of fund based gains was an eye opener for me. I thought it (~6bn) will come in P&L but they have directly taken it into the balance sheet leading to substantial jump in book value (to 3k cr). Fund based gains will largely be MTM gains/losses for the quarter and will remain volatile. e.g. Q2 should be great for fund based gains.

@investr check consol results on their website. I think tax adjustments for prior period has optically depressed PAT. Despite headwinds and volatile market conditions this outcome is satisfying.

http://motilaloswalgroup.com/Downloads/IR/1562270294Consol.pdf

disclosure : Invested

3 Likes

This rumour is quite believable given the fact that one promoter has pushed it into housing finance while all other divisions related to equity biz continue to do quite well. However, they have a lot to lose if the disruptive break up happens.

Disc: Invested

2 Likes

Disc - not invested. tracking

1 Like

Record date for Final dividend(Rs 4.5/-) : September 21, 2018.

Amount will be credited/dispatched on or before October 22, 2018.

AGM on September 27, 2018

Go for unrelated diversification and you have Aspire like situations. The top 5 housing companies have cornered 85% of the market with their credit rating as moat. The top 5 concentrate on the 25 lakh plus salaried category, while the bottom 80 scrape the lower 15% consisting of low income groups. What they require is an efficient man at the top. And they need to give the loan to credit worthy borrowers. Piramal a new player has a different approach. Piramal has a unique loan distribution strategy where the repayment amount keeps pace with the increase in salary.

Motilal is the best professionally run equity AMC. It is the hen which lays the golden eggs and doesn’t need capital to grow. Aspire was Motilals attempt to use the Surplus cash a la Bajaj finance and also to have a regular income during stock market crash. But they don’t seem to have read the housing market carefully before entering it.

3 Likes

1 Like

In the interview Raamdeo makes it clear that asset management will be a 100 lakh crore industry in 2028 and MOFS cannot handle more than 1 to 2 lakh crores. Stupendous opportunity. Do not know why they are spending so much management bandwidth on housing finance, when the scope in asset management itself is infinite. Hope good sense prevails .

I agree. The management has been downplaying the Aspire wreck by saying that it contributes ~20% to PAT, but what about capital? The business sucks large part of capital. As you have rightly mentioned the rest of businesses require almost no capital, such disaster in a capital heavy business just crashes the ROEs. However, I expect the AMC business to continue to outperform.

Disc: Invested

SJ

Aspire was Ramdeo’s idea and in one of his interviews he had said they were fascinated by the high p/b multiples of Gruh finance that resulted value creation so he got greedy. But poor biz sense showed its effect earlier than expected. I am still scratching my head how could they set up an HFC without legal and recovery support. The point is even Motilal Oswal got involved when things got worse. Big lesson is that not every successful Buffet fan can run an operating business like him.

Invested but keep evaluating.

What will be the impact of SEBI expense ratio on their PAT?

What will be the impact of 100 basis point increase in interest rates on their PAT in Aspire?

Impact of SEBI regulation will be marginal considering close to 50% of AUM is PMS/AIF which wont get impacted. In their Mutual Fund business only one scheme which has a AUM of over 10000 crore will be impacted a little (higher the AUM greater the impact). Even in that scheme only the regular plan portion (64% of the business will be affected). So as per my estimate out of 38000 crores in AUM only 14000*64%= 8960 crores will be impacted.

1 Like

Motilal’s schemes have smaller AUMs and their share of direct plans is growing faster so I would not be worried. However, they are also distributors of these MF products and they will take a small hit there. Wealth management products also push clients into MF products and they would lose commissions there or they will be trailing in nature and accounting treatment will be different. However, this would also increase return potential and attract more flows in the long term. Additionally, distributors will see consolidation and those who are advisers rather than just salesman will be real winners in the long term.

2 Likes

@sumi00 Your statement “However, this would also increase return potential and attract more flows in the long term”

Great long term thinking. This should also teach investors to move away from PMS and other such hedge fund like set ups, which significantly erode investor wealth with their 2 & 20 commissions. In today’s Business standard, it is mentioned that the new rules will affect the smaller AMCs more than the larger ones, while the newer ones will take 10 years to break even as against the 7 years as at present. This should keep the competition at bay, and discourage newer competitors from setting up shop. So in effect, competition has been discouraged, and the top few funds will corner up the market. The big boy wins. Their PMS returns are untouched, while life is made hell for new mutual fund competitors. 3 cheers to Motilal Oswal.

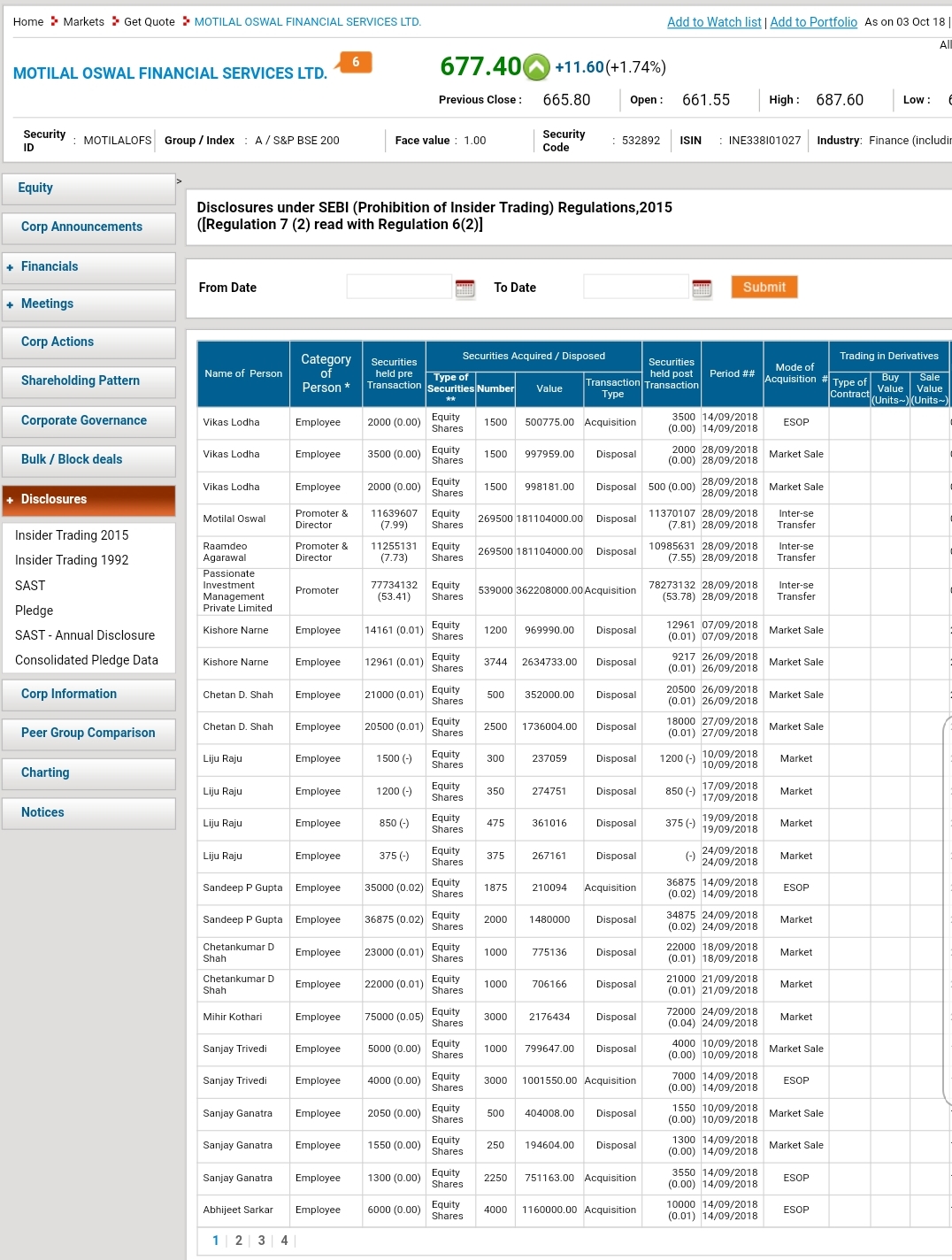

Who knows better better than investors about a company? Yes, their employees.

See the disposal of shares by their employees

Large deals are only transfer between promotors.

1 Like

Motilal Oswal appoints Sanjay Athalye as new CEO for Aspire Home Finance