Apart from housing, broking margins also seem worrisome YoY - Revenue 234.6 cr vs 155.9 cr (fantastic growth of 50%) but PBT at 41.9 vs 35.5 (sub 20% growth in earning).

Recently invested and a little disappointed with the results. Hope the stock gets punished tomorrow - want to add more!

ESOP one time adjustment - Otherwise profit would have been 40% + YoY.

NPA 1.6 - Average ticket size is 10 lakh. I believe this segment will have high NPA’s. Need to watch out for.

Everything else looks good - ROE 22% - With unrealised gains ROE is 26%

Motilal Oswal is trading at P/E 51.3 & P/B of 9 - Expensive valuations compared to peers. I expect MOSL to double its profit by FY19 if bull run continues.The growth should come from all verticals i.e. broking, mutual fund, PE fund & housing finance. P/E FY19 = 25? What do you think?

Yes, I agree investing at these levels is not as easy as investing an year

ago. However I still hold my position in MOSL.

Given the cyclical nature of the business which is correlated to market

performance I think most money would only be made by those who would be

able to exit it at the bull cycle tops (easier said than done!). Therefore

I view my current position as a trade than a very long term investment. I

am hoping that with the bull market in place the P/E will be intact

(neither increase nor decrease) till the bull cycle top comes and money can

be made by increase in earnings .

Say nifty compounds at 15% for the next 3 years it is possible for the

company to grow earnings at 25% with help of some operating leverage.

Comparison to peers is a little difficult as all the NBFC’s have a a

unique business model and risk profiles. I don’t see many AMC + Broking +

PE fund + Housing finances.

*Fundamentals: * Overall I think the company is executing the plan well

and is positioning themselves to become a large finance institution. Below

are a few thoughts:

Broking: Held their market shares and customers in spite the presence of

low cost brokerages. Not many new entrants now in this field.

AMC: Growing at a rapid pace approx. 10cr per day inflows in focus 35

fund. However the competition is increasing from new funds being launched.

Trying to enhance brand to stay competitive.Regularly see this ad on

republic tv.

*PE fund: * A lot of wealth creation is being captured by PE funds in

general. Lofty exits in IPO is commonplace.

*Housing finance: * Business is growing at a reasonable speed. LTV < 60%

and avg. ticket size of 9 lakhs gives me some comfort about underwriting.

Investments: Their investments in their own MF are doing well and they

are booking profits from it.

Just wanted to understand how the Aspire business is shaping up on the affordable housing side, last quarter the NPAs were high and this quarter will it continue ? i remember Ramdeoo talking about improving the collections and he is very impressed by the PNB housing and would focus on the asset quality going forward, although last time they had moved to different type of accounting standards which resulted not so great results, so will that reflect good results this time? any more details is welcome.

Motilal Oswal Financial Services reports Q2FY18 Consolidated Revenues of Rs 7.14 billion, +35% YoY; and PAT of Rs 1.44 billion, +42% YoY

PBT up 56% - because of onetime tax outgo

All the business division are firing - Asset Management, Private equity, brooking, Wealth Management & home finance

ROE 29%, including unrealized gain of 580 cr the ROE could have been 32%

Motilal strategically transitioning from nonlinear earning from broking to linear sources of earnings like Asset Management and Housing Finance. Over half of the revenue pie now coming from these new businesses

Housing finance average ticket size is 9 lakh. GNPA jumped from 1.6% to 2.8%- This is a matter of concern but management has admitted that this is new business for them so lot of learning and they will try to fix these issues

MF revenue is up 96% YOY, PAT up 154% at 23 cr. Expect more operating leverage to play out

Hidden assets - 1250 cr investment (includes 580 cr unrealized gain) into their own mutual funds and quoted equity investment + investment in PE fund 290 cr at cost. As per presentation this fund based business has post-tax cumulative XIRR of ~29% . This is great. Even if we assume 15% of (1250 + 290), this should generate 231 cr annual profit for the company. This figure is more than 50% compared annual TTM profit of 424 cr

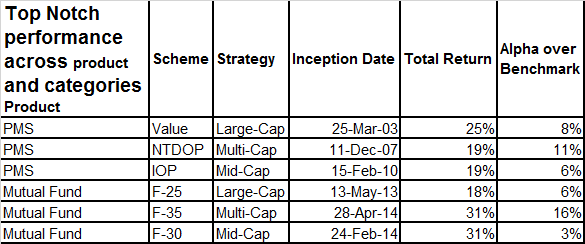

If they can manage NPA of home finance then this can be a good story with huge financialization of savings expected in coming years. They have very few focused MF. And these funds (Multicap, ELSS, Large cap) have completed 3 years since inception with very good CAGR (31%. For multi and midcap) Mulitcap is in top 3 in that category. Expect huge equity inflows in coming years.

At CMP of 1375, EPS 29.34 stock trades at 46 PE so yes it looks expensive compared to peers but strong profit growth is expected in coming years to come

The Housing fin is a concern and Mr Ramdeoo suggested their focus will be on the assets quality improvement, rather strange to me is they are now getting the collection policies and procedure right in order, i felt this could have been taken care when your starting lending business where collection is biggest part (As Mr Ramdeoo has good understanding of banks in the past & seen issues with collections). Good part is management is open about it and trying to fix the issues, being realistic and transparent.

Everyone these days giving reason of Demon, RERA & GST for growth & collection but Aspire was worst hit more than double and today’s fall also kind of indicated the displeasure.

Need to wait and see how the next collections will shape up & asset quality improvement.

Also he suggested since the focus on the asset quality the growth may or may not be as it was for next 1Q or 2Qs.

I had called investor relationship manager and had asked him why your GNPA are more compared to Gruh whose average ticket size is also in the similar bracket 9 to 12 lakh. His answer was most of MOSL customers get their salary in Cash and they are part of informal economy. Because of both demonetisation, RERA - It had an impact. Also he mentioned that Gruh is in the business for 30 years while we just started, learning and still putting processes, infra in place. Remember this is a secured lending, company can liquidate the borrowers assets. So yes situation can be controlled but a cause of worry right now.

Their private equity of 4200 cr (includes 250 cr own investement) is a game changer. They charge management fee and performance fee to clients above hurdle rate. Out of 4200 cr only around 500 cr has been exited so they have decade long income stream that too can be incremental profit.

Just look at the recent IPO - MOSL was allotted shares of MAS financial worth 134 cr at price of 338 per share somewhere in Apr 2017. The recent share price is 635. i.e 116 cr profit on 134 cr investment in just matter of 6 months.

Similarly, they have PE investment into RBL bank, Dixon technology, AU Small finance bank and many such good companies.

For example:

MOSL (IBEF I and IBEF II ) held 30% of Dixton Technology.

MOSL sold almost 25% as part of IPO offers.

Also, per latest SHP, MOSL do not hold any shares. So, they have sold remaining 5-6 % at listing.

This should fetch 300cr+ altogether.

But I do;t see that reflected in revenue. May be I am missing something or looking at the wrong place.

Isn’t that conflict of interest that while they have PE investment in say RBL bank and they are buying the same in their MF and recommending to their PMS clients?

PE funds are basically pooled funds from investors which the entity running the PE invests in nascent or during Pre-IPO stage, and the PE fund exists as per their exit schedules and market conditions for paying out the investors.

MOSL earns management fee as well as a commission above hurdle rate based on returns. What ever the shares they buy or sell are basically on behalf of the investors (MOSL may hold some percentage of the Fund though).

PE funds as you might be aware are like PMS or in a way mutual funds (with limited exit options). No conflict of interest. In many cases one mutual fund may sell and other may buy the same share within MOSL

Please correct me if I am wrong in the comments here.

They manage PE fund of 4200 Cr. This includes 290 cr of their investment into this PE fund. So yes they have skin in the game which gives lot of comfort to new/existing and I won’t see this as negative. They also have around 1200 cr into their own mutual funds which have XIRR of 25 to 29%. This means they are very confident in what they are doing. Mohnish Parbai has praised Motilal for this approach very recently.

Reliance Nippong life is trading at 43x (ROE of 22) and Motilal at 46x (ROE 32% including unrealized gain) with 1800 cr in to MF and PE investment on their balance sheet.

I am looking to make fresh entry into MOFSL but worried on the three counts

a) The Home Finance business is fairly new with last one year showing that management is still learning and implementing appropriate systems and processes - so there may be surprises on NPA especially since growth in this business has been explosive

b) Broking, Asset Management and Fund based businesses are at all time highs considering all are benefitting from the all time high of equity markets and huge domestic fund flows into equity markets - I would not bet against it at present considering the domestic fund flows look to continue. However, these businesses will be hardest hit if/ when the music stops

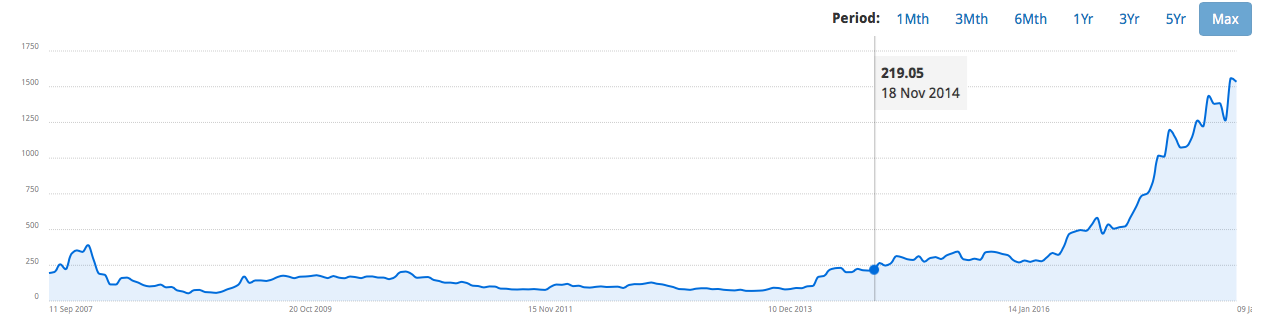

c) Lastly and most importantly, stock is trading at P/B of close to 11 which makes it very difficult to enter at current levels. Looking at long term history and a similar instance at the end of last big bull market in 2008 (some may say its probably different this time but I would beg to disagree!), the stock had tanked from ~400 in Jan 2008 to around ~80-100 levels and remained there till mid 2014!!!

So, my question on MOFSL is how to judge the appropriate P/B ratio for this stock in this business. I can probably apply a P/B to the housing finance but looking for help on the other businesses of the company which are the current growth engines.