Mold Tek shares are trading & also Mold Tek RE is trading. This is the right to apply for 1 share & 8 warrant as a bundled product. Please apply for rights by Nov 11. The RE is trading around 340 as that is the value if you look at the difference in the current share price & the value of shares after deducting the cost.

Now I understand.

Currently trading rights equity is also incorporated with 6 warrants

So minimum theoretical value of RE is (260-45) + 6×(260-180) = 695 ₹

But generally warrants trades a premium value so RE can go way above 695 also.

1 Like

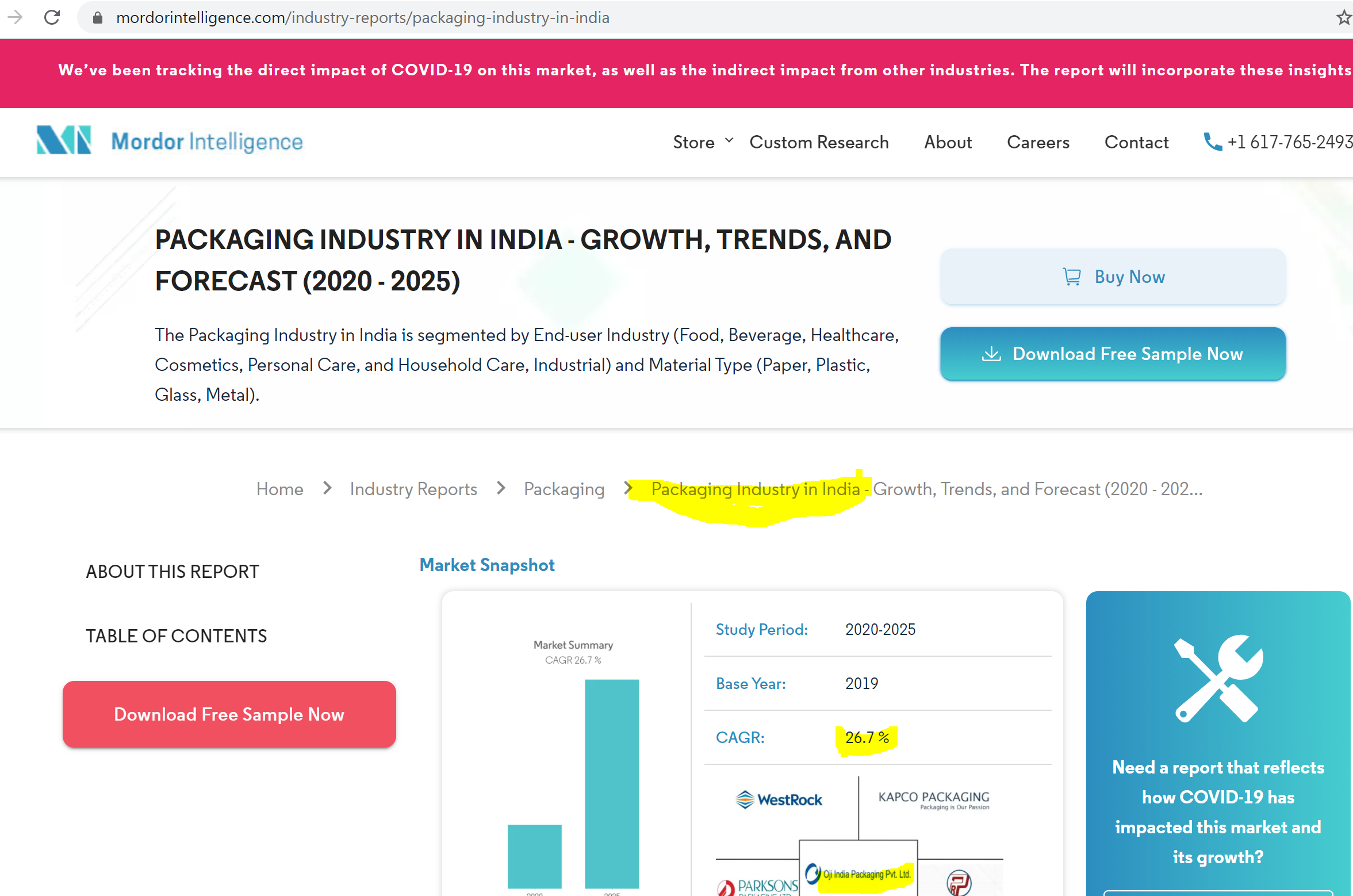

How much authentic is this super optimistic ‘Industry Reports’ projection?

Source: AR 2019-20, Chairman’s Speech.

2 Likes

Thanks @Rafi_Syed, but this is a hugely optimistic estimate in my opinion. Any idea how reputed this research company is? I am saying so because, the ICICI Direct estimate in the Huhtamaki India report says that “The flexible packaging industry in India is likely to grow at 10% CAGR … by FY23”. Does that mean that the flexible packaging industry will grow much slower than the packaging industry in general?

I am attaching the Nirmal Bang re-initiating coverage report in this context. (see page no 9)

Mold-Tek–Packaging-4QFY20-Result-Update-8-June-2020.pdf (726.1 KB)

Nirmal Bang’s original initiating coverage report on 2017 is also very much informative and has peer comparison.

Mold Tek Packaging-Initiating Coverage-26 April 2017.pdf (1.1 MB)

3 Likes

According to the 2017 report by Nirmal Bang attached above:

Going forward, Indian packaging industry is expected to grow at a healthy pace of 18% per annum wherein flexible packaging is expected to grow 25% per annum and rigid packaging is supposed to grow 15% annually.

Not sure which estimate to trust, but it is quite intuitive that flexible packaging should’ve greater growth rate given its more universal usage.

1 Like

I believe Manjushree Technopak - formerly publically listed company that was delisted about 5 years ago, is also in the IML space. Is this a serious competition to Mold Tek?

Disc: Tracking not yet taken a position.

1 Like

Manjushree Technopack is a leader in blow moulding while MoldTek in injection moulding. Two different categories. Also, I don’t think Manjushree does IML nor you can do IML for blow molded containers. In packaging, all the leaders have their own niches be it MoldTek, Manjushree, Essel or Hutamaki. So no direct competition as such.

9 Likes

Company came out with very good results.

- PAT up by 68.85% Q3 on Q3 and up by 11.01% Q3 on Q2 and up by 4.23% for 9M

- Basic EPS up by 71.72% Q3 on Q3 and up by 12.95% Q3 on Q2 and up by 4.75% for 9M

- EBIDTA up by 48.31% Q3 on Q3 and up by 7% Q3 on Q2 and up by 6.2% 9M

- Net Revenue up by 32.64% Q3 on Q3 and up by 12.07% and Q3 on Q2 and dip by 4.24% for 9M

- Volume up by 36% on Q3 on Q3 and up by 9% on Q3 on Q2 and up by 1% for

Key points to note:

- We are proceeding with capacity enhancement in Satara, Mysore, Vizag & Hyderabad plants. We are glad to inform that the Asian paint new plants are running at 80% capacities.

- The Company has successfully established & started commercial production and supplies of pumps. In addition to Twist Lock & Lockdown pumps, the Company is exploring additional range of caps & closures like trigger pumps.

- New packs that were launched in 2020 — Hinge pack, Sweet pack, Square packs, Adhesive packs are slowly getting traction and will drive growth in the coming years. Demand for new segments for our square packs is growing rapidly.

9 Likes

I was going through a company named mold tek packaging and i found one of your ( @vivek_mashrani ) presentation. I went through it and i must say that was an excellent analysis and important key points are mentioned so thanks for this. So you were also doing research on this company can you please answer my doubt for which i haven’t found answers in concall/ annual report.

My doubt is the company historically had debt and was selling stakes ( 2012-13) to reduce debt, even did rights issue for the same.

So they are concerned to reduce debt and now its below 0.5 d/e but along with it they consistently given healthy dividend throughout last 10 years so a company having debt distributing high dividend and depending on debt for future capex how you look at these kind of capital allocation? Is it normal or worrisome thing?

5 Likes

What are your thoughts on management integrity guys? Has anyone from our group met management? Hows the management in person though we know that they are delivering what they promised! But they have low skin in the game… won’t go for professional management in future i guess as next generation is also into the business

1 Like

Good Questions Suyog. I came across Mold Tek Packaging through Little Champs Portfolio by Marcellus Management aka Saurabh Mukharjea.

Attaching the Youtube video link about explaining their rationale for investing in all their small cap stocks.

Please view from 46 minutes on the timeline for discussion on Mold Tek Pack.

I am definitely biased towards Marcellus team and Saurabh. So have recently taken position for only 5% of stock portfolio in to this idea.

Lets see how it pans out.

Vikas

6 Likes

Hello VPers, How do you guys see Hitech Corporation in comparison with MoldTek ? I think margins wise Hitech corp is catching up of late. Revenue wise both are almost on similar lines. Its hard to get the information about Hitech as they don’t do any concalls. Only information is AR and most of the content is repetitive. Both Hitech and ModTek have done capex in Mysore and Vizag for Asian paints plant. Hitech is bit illiquid as promoters are holding roughly 75%.

45680-891211d5bc7443548686da4f44ecefca.pdf (580.3 KB)

Sharing latest pdf on Mold-Tek Packaging by Axis securities.

From trendlyne website.

In depth and some good points discussed.

Hope you guys find it useful.

Regards,

Vikas

2 Likes

2 Likes

Board to consider interim dividend on March 8.

So first we raise cash using a rights issue and then we distribute cash via interim dividends.

Capital Allocation?

1 Like

The purpose of the RE was to repay WC loan and borrowings

Your indication is correct. In Last 3 years on average company has not generated any FCF at all. Capex intensity was high due to Asian paints Greenfield and other Brown field capacity expansion .But think that this year is exceptional and company wants to distribute some of it as dividend.