Mold Tek Packaging - Expect 10% topline growth with Ebitda margin of 15% for FY16, FY17 growth pegged at 20% - Concall Update

Mold-Tec Packging – Company is into molded rigid plastic packing industry which supplies to major lubricants, paints and edible oil manufacturers.

Industry outlook – Currently, Demand from Paint industry is almost Rs 1000-1100crs of which 50% demand is from Asian Paints in organized sector while Lube Oil demand is in the range of Rs 400-500cr. Apart from organized market, Unorganised market demand is in the range of Rs 350-400crs. Recently, Edible Oil mfgs is also started using rigid packaging in which company is into. Based on initial estimates, the size would be around Rs 1000cr of which company intends to capture 10% share in coming 15-18 months.

In Mould Labeling (IML) Decorated containers – Company offers IML containers and is only company in India with its own in-house process. Company has filed the process patent to Indian Patent Office which has been accepted there, certificate to come in next 2yrs. Currently, most of its existing clients are shifting to IML containers. Asian Paints which is their biggest client is apprehensive as it will make them dependent on the company for the container supply and is not keen to fully shift to IML as of now. Company reported IML sales of Rs 95cr (33% of total revenue) vs Rs 61cr yoy.

QIP Issue – Company recently raised Rs 55cr at price of Rs 220/sh by issuing 25 lakh shares. DSP Blackrock MF, SBI MF, Principal MF, Amundi Funds and Canara Robeco MF are among the investors subscribed to the QIP issue. No plans for raising any equity for next 12-18 months.

Guidance – Company’s growth is primarily driven by Lubricants, Paints and Edible Oil companies, of which, Lubes and Paints industry are currently facing some headwinds while company’s recent entry into edible oil segment is showing significant traction. Company is expanding its edible oil molding capacity by 8000tpa which will get operational in phased manner over FY16. Full benefit to accrue in FY17. Company expect volume growth for FY16e at 10% and FY17e at 20%. Realization are linked with input prices so assuming the current RM prices, management see slight improvement in Ebitda margin to 15% vs 14.25% reported in Fy15.

Capacity – Company has current capacity of 22500tpa and is planning to expand it to 32500tpa by next year end. Current utilization is at 70%. Management indicated that the segment is such that it cannot operate at the nameplate capacity.

Capex – Company is currently expending its Edible oil molding capacity by 8000tpa at three locations with combined capex of Rs 45cr of which company already have spent Rs 14cr during the year. Company also plans to setup its first overseas plant at RAK (Saudi Arabia) with capacity of 3000tpa at total outlay of Rs 10-12cr. Company has deferred its two plants – Vizag (for Asian Paints) and Gwalior (for Akzo Nobel) – due to deferment by the clients by a year or two. Company don’t intent to invest any money this fiscal there.

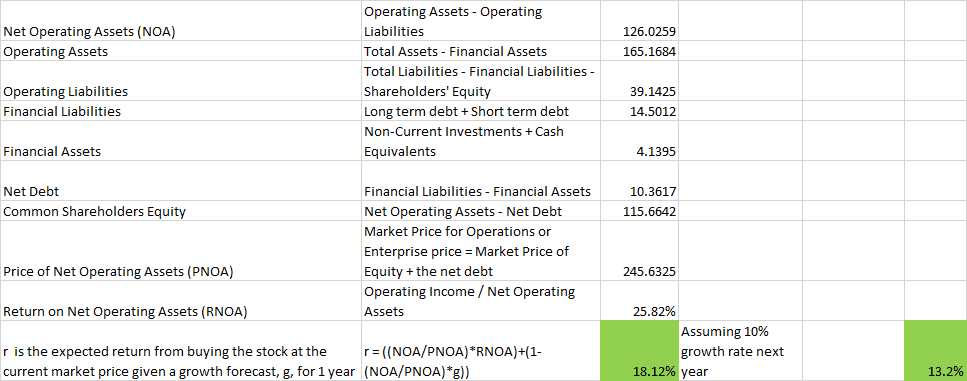

Debt – As of Mar’15, total debt stands at Rs 15cr (Rs 10cr LT debt). Networth at Rs 116cr. Management guided that working cap bound to increase to Rs 40cr by year end and expect Avg Debt to be at Rs 25cr range only.