Looks like there is some progress in the REDTAPE listing they have received the SEBI approval

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e59c3a9c-e4e6-48f1-8b58-f9994b367ad1.pdf

13 Likes

With the Red Tape listing imminent in the coming week, it is interesting to see the entire range of products on the Co.'s website. There are a number of new products introduced & the transformation to a fashion brand is very much happening. The innerware market is huge & it will be interesting to see if the Co. can make a meaningful dent there.

There is also an appreciable improvement in the product designs, across the entire product range. One can’t but feel impressed going through the website. I also gather that there is a marked improvement in inventory mgt of the Co. that is likely to improve the working capital cycle.

After Red Tape lists and the Co. declares the numbers for the year 2022-23, will we get a better understanding of what the base is & what to expect going forward. It will indeed be fascinating to see how the markets value a pure fashion company. All kinds of multiples are being suggested, but we should know shortly. Meanwhile, checkout the website & enjoy the product range & designs.

27 Likes

There accessories and products in footwear and clothing category are good in terms of styling as well.

Good to see Redtape brand revolutionalising from leather formal footwear to a fashionable one stop solution brand.

1 Like

Before demerger mirza trades at 28-30 pe in rally. so redtape should trades at higher multiple in bull case ( personal view ) because leather business is not there and shuja mirza as a md . so there is definately a good chance for improving corporate governance (biggest anti thesis if not improve ) . consider redtape 12 eps for fy23 and multiple of 30 so in bull case price comes around to 360. though that time when mirza trades at 30 pe , scarcity premium is there because of campus and metro not listed . now scarcity premium goes away for shoes companies so redtape can get lower valuation .

personal view not buy sell recommendation.

3 Likes

I looked through the Company’s catalogue. From page 10 onwards of the catalogue they are offering wallets, belts and socks at a steep 60%-70% discount. I wonder what is the strategy here. Who will buy a wallet at Rs. 2199 (undiscounted price) when there is something similar being offered at around Rs. 600? (discounted price). A person would be tempted to jump to the conclusion that the “real” price is around Rs. 600 and the Rs. 2199 price tag product will eventually be offered at around Rs. 600.

3 Likes

Products are highly overpriced and post discount rate matches with brands like PE.

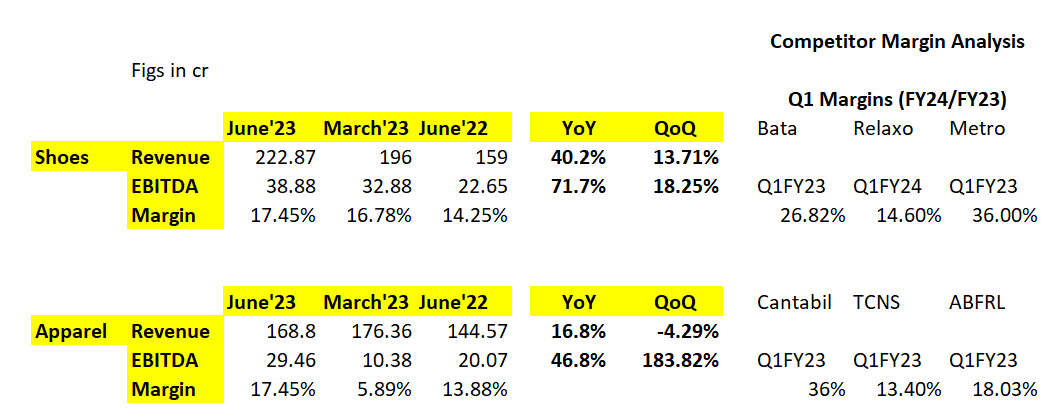

The margins of Mirza are slightly on the lower end. I did a comparison here:-

-

Supply chain optimization & omni channel initiatives (marketplace, own website, etc.) will really help them over the medium term. They get good traction on their insta page, but some of the usual tricks are missing (insta shop for example). These points will help them with incremental margin. Also brand building efforts - imp for mid / long term. Closely linked to success of any loyalty program.

-

Revenue growth in the shoe segment is fantastic. If you go to their product collection, the shoe collection design is really trendy, so I’m not surprised. Remains to be seen if they can sustain the demand traction.

-

Shoe segment margin comparison with Relaxo isn’t ideal. Their ASP is <200 (Bata is ~700 - seams comparable) while Metro has been trending towards the premium range lately. But goes to show that their is room for improvement here. In my view, scale will fix things by itself (better demand prediction, inventory insights, etc.)

-

Apparel growth is sluggish but will give them benefit of doubt since its a new adjecancy for them and they’re still in the learning phase.

D - Invested. 10% PF position approx.

12 Likes

You compared EBIT numbers & margins of Redtape with EBITDA numbers & margins of competitors.

10 Likes

Good catch! I missed that. But I don’t think margins would jump significantly if I try and take EBITDA figs of Mirza. 12crs depreciation incurred overall for the quarter. If I do an equal allocation between the segments, then EBITDA for Shoe segment is 20%, while that for apparel segment is 23%.

Shoe segment still has ways to go given the ASP that is comparable to Metro / Bata ![]()

2 Likes

Red Tape Q1 numbers are superlative. Sales at 393 crs are quite likely at an all time high in terms of branded sales. A YOY growth of 57%. The operating margins too are perhaps at an all time high of 21%. The fact that Q1 historically has not been their best qtr only adds glow to the numbers! Usually its the festive Q3 that has the highest Sales & profits. Even if the Co. can grow at 35% in 23-24 & maintain operating margins at 20%, the Co. could well end the year with profits of about 240 crs with an EPS of about 17-18. The Co. enjoys a high ROCE of 37% if my numbers are correct. This will only improve in the current year. Being largely a fashion/ marketing Co., of some scale, it is quite likely to attract the fancy of investors. A listing below 300 could be very interesting, though perhaps unlikely.

21 Likes

any idea on listing date of Redtape ?

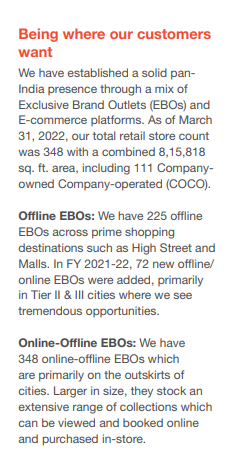

Hello everyone, I have been tracking this company and learning more about it from the detailed posts shared on this thread. Like most of us, I am excited about the growth in Redtape business. I, however, haven’t been able to reconcile the store-count related data shared across past annual reports. For example, the below section from FY2022 AR seems rather confusing to me. It says the total EBO store count is 348. It is then mentioned that number of offline EBOs in prime areas is 225 and finally number of online-offline stores (which are in outskirts) is 348! How can the total number of stores be equal to stores in the outskirts? How do we account for the rest of the 225 stores in prime city areas? Am I missing something very obvious here?

I have prepared a table containing the store count data in ARs of FY20, 21 and 22, and notice the same pattern.

| Number of stores | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|

| Total EBOs | 222 | 276 | 348 | 390 |

| offline EBOs (in prime locations) | 61 | 153 | 225 | |

| Online-offline EBOs (outside the cities) | 222 | 276 | 348 | |

| Shop in shop (or MBOs) | 830 | 246 | 245 | |

| Revenue from EBOs (In Rs. Cr) | 371 | 462 | 798 | |

| MBOs | 83.9 | 0 | 0 | |

| Ecommerce | 212 | 207.9 | 283.9 | |

| Total | 666.9 | 669.9 | 1081.9 |

Further, I notice that while each AR highlights the company’s MBO presence, there is no revenue being ascribed to this channel FY21 onwards.

Separately, Redtape Limited’s FY23 and Q1-24 numbers look impressive on the growth front. I observe that it has inherited a manufacturing facility from the erstwhile parent and has even undertaken a significant amount of capex (163 cr) in FY23, which is visible in the cash flow statement. It seems these funds have gone towards enhancing manufacturing capacity (the details of CWIP mention unit-5 and unit-3), and presumably for development of new stores.

It will be interesting to know what proportion of the stores are owned by the company, whose real estate would be on the company’s balance sheet (FY22 AR says 111 stores are company owned and company operated). It will also be nice if the management can share more details on arrangement with franchise operators (deposits from franchisees seems to continue to grow with FY23 number at 122 Cr).

Finally, the balance sheet looks a little stretched on the working capital side, with inventory growing by over 50% and trade payables growing by over 100% (March 31, 23 vs March 31, 22).

Clarity on these aspects can go a long way in helping investors build conviction on Redtape Limited. (esp. considering the past concerns)

Disc: Invested just before the demerger, but interested in increasing my position size in Redtape Limited

2 Likes

Just to close my question on store count, I went through old con-call recordings (which are not available on company website for some reason) and collected the below information:

| Q4FY19 CC | FY19AR | Q1FY20 CC | Q3FY20 CC | FY2020AR | FY2021AR | FY2022AR | ||

|---|---|---|---|---|---|---|---|---|

| small/offline | 156 | 153 | 159 | 164 | 225 | |||

| large/online | 44 | 53 | 50 | 56 | 123 | (Assuming 225 is correct count for small/offline stores) | ||

| factory shops | 7 | |||||||

| 200 | 206 | 209 | 227 | 222 | 276 | 348 |

It seems to me that Mirza International jumbled up store-count related information in three consecutive annual reports (FY20, 21 and 22), which is surprising, but appears to be an inadvertent error.

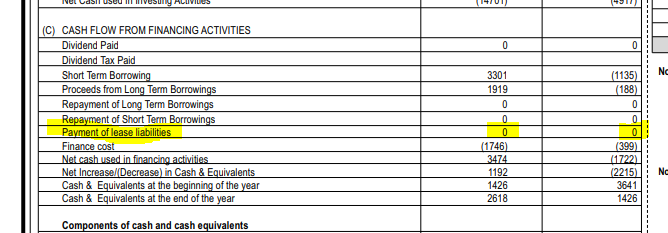

Also, when I was trying to reconcile these numbers, I noticed that there were no lease liability payments recorded in Red Tape Limited’s FY23 cash flow statement (part of recently released newspaper advertisement). That obviously doesn’t look accurate. To be fair, the relevant lease liability entries seem to have been passed in income statement (part of depreciation and interest)

I am not sure what to make of these observations (should they be seen as sign of loose controls/reporting standards?)

2 Likes

Redtape is listing on 11th August 2023

CML57905.pdf (169.7 KB)

22 Likes

Rev Growth for Q1FY24

TCNS - Revenue degrowth of 12%

Cantabil - Revenue growth of 11%

ABFRL - Revenue growth of 11%

Manyavar - Revenue degrowth of 4%

Nykaa Fashion GMV - 12%

RedTape has done 17% growth in its apparel segment, which appears to be industry-leading in an challenging environment (Nykaa commented that the consumer just wasn’t interested in this quarter, ABFRL mentioned “demand sluggishness”, Manyavar said fewer wedding dates)

Just going by this analysis, it appears RedTape is gaining market share.

D - Invested. Added more post listing.

13 Likes

on refusal to allot REDTAPE Shares both by ICICI DIRECT and MIRZA International, I had put up a complaint with SEBI SCORES and they transferred my complaint to GRIEVANCES PORTAL of NSE. NSE took up my case promptly with ICICI Securities and followed it up very meticulsouly. ICICI SECURITIES has credited the REDTAPE SHARES to my account today. Just for info of those who are in similar circumstances.

23 Likes

Shares were not there in my DEMAT Account at all. In fact, they intimated that I am not eligible for REDTAPE Shares.

2 Likes

This is not an issue, in ICICI Direct when any share is added from a demerger, you have to add it manually. Just go to advance options under stocks portfolio and then go to Demat reconciliation, there you’ll find the data and then you can add it to your portfolio. attaching a youtube video which helped me.

3 Likes

What is driving Mirza’s recent performance in shoes?

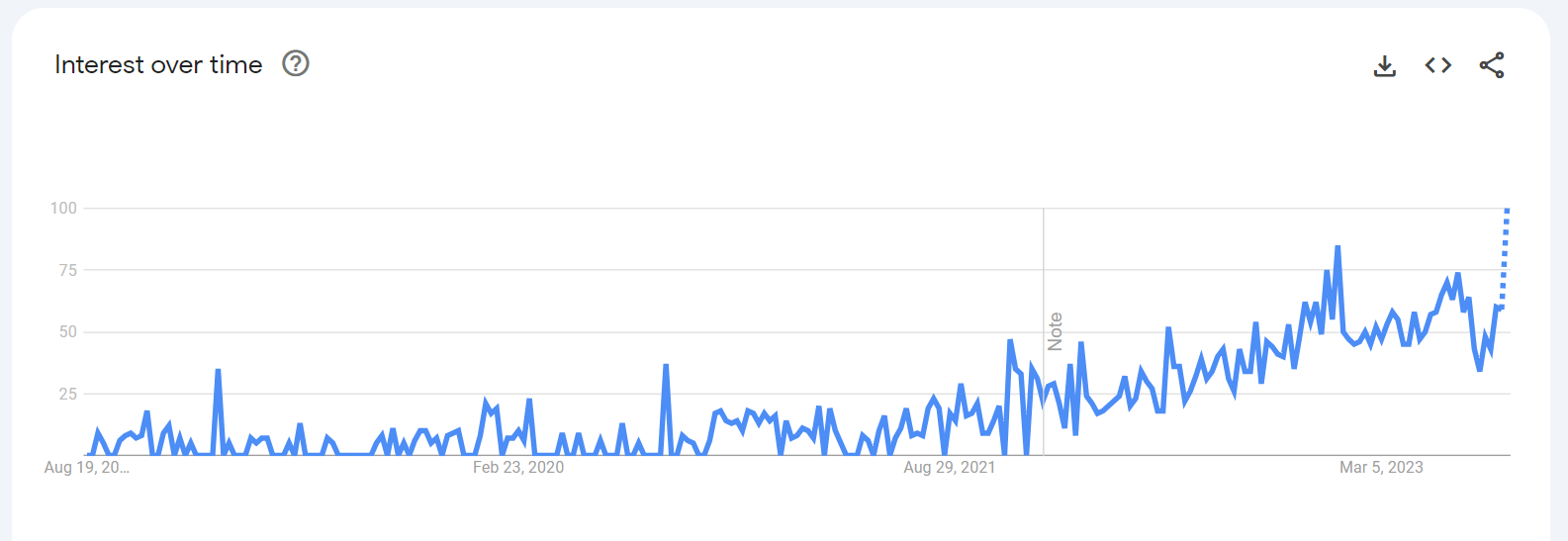

Sneakers. Just look at the google trend data for keyword “redtape sneakers”:-

Rising trendline since last 2 years or so. If you then check Amazon’s bestsellers for men’s sneakers, you see 3 or 4 SKUs by RedTape in the top 10 and many more in top 50. Their designs are good but reviews often complaint of quality. I guess they’ll need to fix that over some time.

Also sneaker market - how big is it? what’s the growth rate?

The sneaker industry in India grows larger every minute. In 2022, the revenue in the sneakers segment amounts to nearly $2.46 Billion USD and is said to witness a volume growth of about 20.5 per cent in 2023. - Deconstructing India’s Sneaker Culture - Luxebook

I guess over a medium / long term - a good question to ask RedTape is whether they intend to collaborate with any star for sneakers or do they wish to compete with resellers like Mainstreet Marketplace given the existing price points of RedTape (sub 2k).

5 Likes