Excellent results. EBITDA is 56% and with increasing operating leverage it should settle somewhere around 60%.

Projecting a conservative topline growth of 20-25% from here onwards, I see company hitting 1000 crore revenues and close to 500 crore PAT (assuming same EBITDA is maintained) by 2026.

At current market cap, 2 year forward multiple comes to roughly 40 p/e, which is in line with historical multiples. But that would still be below industry average looking at current multiples of BSEs of the world. And any further rerating of the stock should create significant upside to the stock price.

1 Like

But the QoQ revenue is down. Not sure why…

Given the business model of MCX, one shouldn’t look at qoq numbers as top line will not always be linear quarter by quarter due to changes in market sentiments and volatility levels (in both equity and commodity) which in turn drive the volumes. Annual revenue growth is a better indicator of market participation which has been on a continuous uptrend.

2 Likes

But if volume goes up QOQ, should the revenue not go up?

Revenue and margin per transaction that MCX derives from different products, in both commodity and equity segments, vary which may explain divergence between volume and realization.

Need to check once again - what i recollect of having seen is volume is higher in all segments

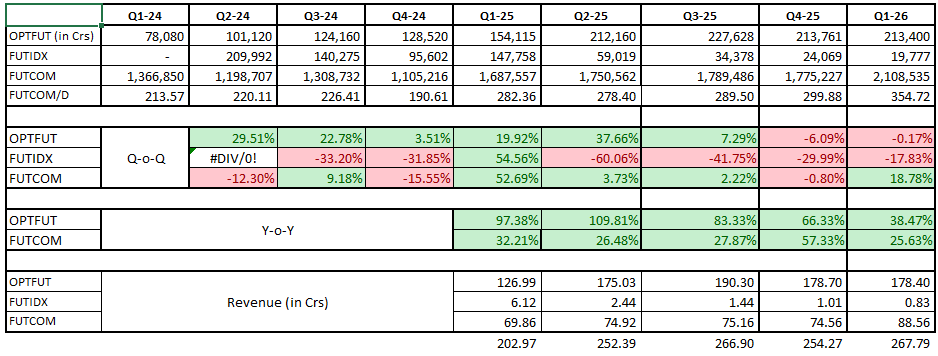

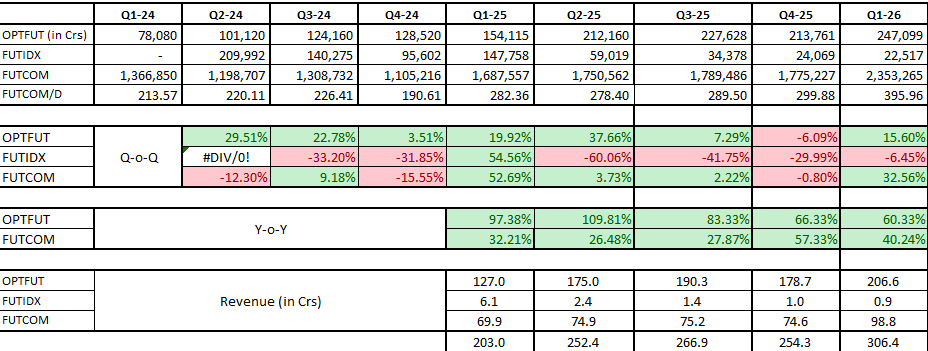

Quoting a news article “the volume of options has grown from ₹95,989 crore in Q3FY24 to ₹113,672 crore, while the amount of futures has decreased from ₹20,796 crore to ₹17,558 crore. As a result, operating revenue decreased slightly from ₹191 crore to ₹181 crore”

2 Likes

Stock has smartly recovered 18% in three sessions from 8% cut on post earning date. Not sure if Morgan Stanley downgrade had anything to do with it. (They placed a target price of 2000.)

For some reason MS has been perpetually bearish on the stock having given three downgrades in last three years. Clearly stock has disappointed them so far ![]()

1 Like

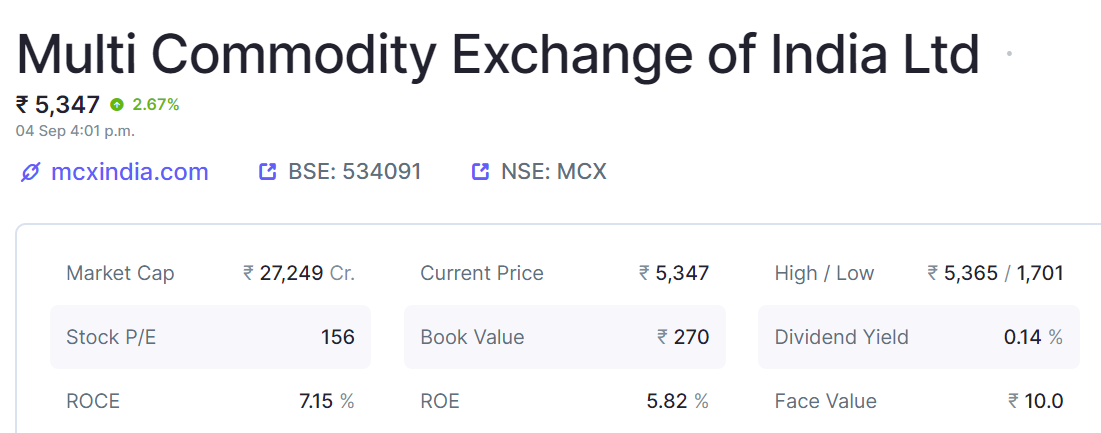

I am holding this stock for a long and recent rally has put me in a dilemma about whether its still worth holding or its a bubble category now? Is 156 PE justified?

This is trailing PE, Expected PAT for FY25 is 450-500 Cr. So forward PE is not what is seen.

3 Likes

what is your view on revenue growth going forward? even after posting good numbers the PE is still 96

The PE is artificially high as in Dec 23, there were significant payments to 53 moons provider of the legacy MCX exchange/trading platform. You should look at forward P/E.

Large of part of MCX costs are fixed so any additional revenues from increase in trading volumes go directly to the bottom line. MCX and most exchanges enjoy huge operating leverage.

A lot of new products are expected to be launched in the coming quarters. Expect volumes to increase post this. These were delayed pending the switch to the new trading platform. Look at the circulars on the MCX site https://www.mcxindia.com/circulars/all-circulars which show a slew of new product launches.

MCX enjoys nearly 98% share in commodity futures.

There is a huge runway, NSE and BSE options volumes are 250 times MCX volumes.

It is easy to track earnings, daily volumes are available on https://www.mcxindia.com/market-data/historical-data. Given operating leverage earnings are largely proportional to transaction volumnes.

11 Likes

Jan month data has only 10 trading days.

The FUTIndex segment has not done well.

Almost all the option volume is coming from Crude & Energy segment. It could be because of the higher margin in Fut Segment.

2 Likes

I am new to MCX. Might seems noob question but what is the meaning of all 4 terminolgies - FUTCOM, FUTIDX, OPTCOM, OPTFUT?

After recent regulatory changes, we are seeing almost 30-40% dip in options trading in NSE. How about MCX? Can we assume that MCX won’t be affected much or in contrast they might gain bcoz of tighten F&O rules in equity ?

What data suggests for last 2-3 months for it ?

In my mind there is a significant difference between MCX and equity capital market plays - and therefore looking at trends in equity capital markets is unlikely to provide appropriate explanations for what happens at MCX.

My understanding of MCX: MCX is a commodity exchange - whereby a fundamental building block is consumers of commodities use the futures market to hedge commodity prices for their use. Typically there are also physical delivery contracts - so MCX enables physical deliveries of commodities. Physical deliveries as you can imagine will be large and minimum contract sizes can be large

Using the futures as an underlying, options on these commodities can be traded. Commodity traders can be individuals or institutions. From data provided, more than 50% of volumes are from institutions / hedge funds.

As a general trend, average traded volume has been increasing QoQ in high single digit / low double digit in the last few quarters. This hides the fact that futures have generally been declining (although seems to be growing again) and options have been growing exponentially

What drives volumes in commodities are volatility in commodity prices - so more volatility typically means more volumes. There is not necessary a link to the equity markets (and therefore MCX should not be compared from a trend perspective to equity futures and options)

Please see MCX and Financial Technologies - #357 by rranjan above that gives you a link to the historical futures and options data - that is published every day - if you want to track traded volumes

Happy for my understanding to be modified / corrected by others with more experience in commodity exchanges.

Disc. Invested so might be biased. Not investment advice

8 Likes