Max group is always so complicated and difficult to understand. So many subsidiaries and events in each for each listed firm. Glad I sold Max India at significant long term loss, Max Fin at long term no profit/no loss (Thanks to Mr Amitabh for the Axis bank stake news, otherwise Max Fin would have been languishing at significant long term loss. He gave me that opportunity long back via HDFC Life stake buy news also but it didn’t work out for both of us back then). They are my tuition fees to the markets and a memory to me to remember from what type of firms to stay away from, inspite looking great and promising.

Disc: Hold Max Venture long term at loss. Lets see what this tuition fees teaches me

1 Like

Optically good results. MSF is the face saving entity again. At a consolidated level, ex MSF, the rest of the business continues to make losses. PBIT of MSF is 40.01 cr and total PBIT is 39.67 cr which means the remaining business has PBIT of (0.33) cr (loss) and if you include interest and tax, it is further down in negative of approx 6.73 cr.

This is actually the worst results ex MSF for MaxVIL in the past one year. There was never a scenario where total PBIT of MaxVIL was less than PBIT of MSF.

Disc: Invested

3 Likes

My Point of View from this position:

Assets: If one compares the overall assets to Enterprise Value (MCap+Debt), the business stands out to be undervalued. Even the CEO has mentioned in the recent call that the share is immensely undervalued. Considering the apathy of Mr. Mkt, Assets are not the benchmark to value this business. Generally, minority shareholders benefit due to appreciation in the share price. In my opinion, one should not rely on assets as the valuation criteria in this case.

Earnings- Capital Appreciation as the Lever: Both quality and consistency, which are valued highly by Mr. Mkt, are not evident. Both the key businesses-Commercial RE and Polymer Films- are Cyclical. The same limits one’s ability to forecast earnings in the nearby future. Besides that RE as a sector has an ongoing HUGE negative HALO effect that is evident in ongoing ‘survival of the fittest’ for suppliers of Houses (Builders) and Capital (NBFCs and Banks).

Earnings- Return of Capital as Dividend: The business is in a phase of investment, which I anticipate to continue for another couple of years considering the aspired plan for RE business. A dividend initation from the company in such a scenario is neither prudent nor anticipated in this period.

A reputed insurance Partner- NEW YORK LIFE holds almost 23% of the Equity: That’s a good sign but one needs to keep in mind that their horizon for investment is long term (10+ Yrs) and a minority shareholder should not assume that their presence will provide a return on daily, weekly, monthly or yearly basis

The key questions one should ask are:

- How one will benefit? Assets are not going to be liquidated. Only earnings have to provide the steam for the engine to chug along.

- Is management taking the right steps to ensure a bigger payback at a later date?

- When those earnings will start? How far is that milestone?

- Does one’s investment horizon permit to wait for that long?

Disclosure: Invested for a very long time and have the opportunity to book a significant tuition fee. Not a recommendation and shared my note to learn from fellow VPers Scrutiny.

7 Likes

Agree, key question for me would be if the management actually wants minority investors to benefit? Somehow, they excel in art of deals and benefiting themselves and the PE firms.

Also, you mention of insurance partner… insurance is a seperate business with no links to max venture…can you elaborate? Thanks for sharing your journey…

Thank you Surender ji for sharing your note. I kind of agree with most of your points and share a similar thesis.

- The market I guess will not value this business at fair value based on assets. Significant earnings (profits and cash flows not just revenues) have to kick in (particularly from the RE business) for the market to value the business well.

- Dividend payout at least for the next 3 years would be negative for the business since the packaging business had a major capacity expansion recently and there is significant amount of debt to be repaid. There is no earnings from the RE business to pay dividend as it is in investment phase.

- Management in the last year’s annual report committed that they will be agile to monetize various investments (including packaging business!!??) if needed in the future at an appropriate time and price to scale their RE business.

- They have reiterated various times that RE business is the future growth driver for MaxVIL. The way Max group has monetized various businesses in the last decade, monetizing packaging business at the right time at a right valuation might not be a surprise in the next 3-5 years.

- Management’s strategy to develop RE business in a asset light way limits them on how much they can scale on a YoY basis, given that RE is a capital intensive business. They cannot continuously dilute equity. They just had an equity dilution couple of years back through rights issue following the warrants issue to promoters and initial investment by New York Life in 2017. However they have stated in the last earnings call that they are comfortable taking debt going forward at a debt/equity ratio of upto 1:1 for RE vertical. Let’s see how this pans out.

- Considering these points, I think MaxVIL story is a really long one of 4-5+ years unless market suddenly starts believing the management’s commentary and begins valuing the business on future earnings projection (like Godrej Properties

)

)

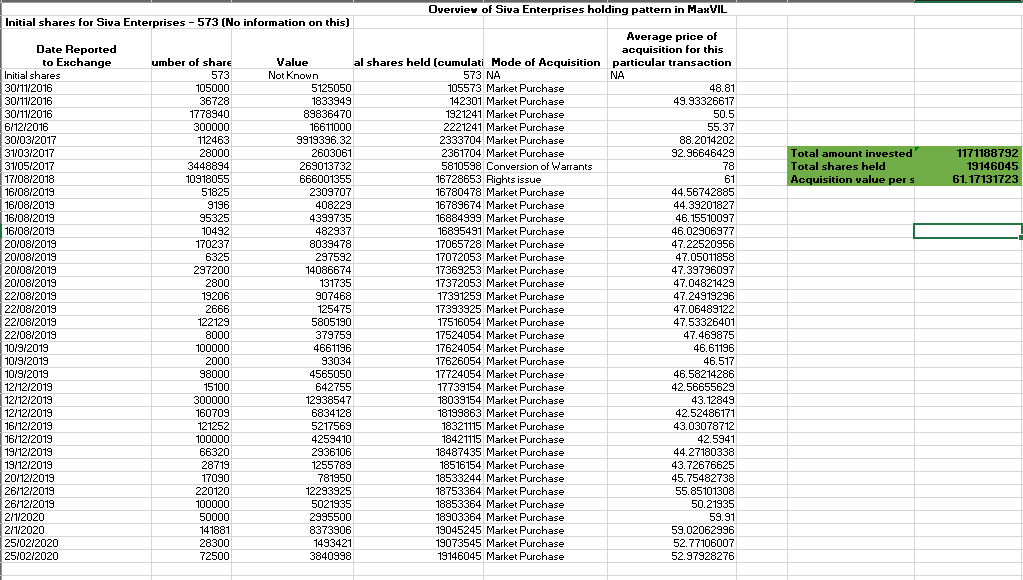

On a side note, like many of the minority shareholders, the CEO of the company Sahil Vachani is also invested in this company at a higher price (13% holding in the company at an average price of ~61). So, it is in his personal interest as well that he and his management take the right steps and deliver the results ![]()

Siva Enterprises - SIVA ENTERPRISES PRIVATE LIMITED - Company, directors and contact details | Zauba Corp

Disc: Invested in the company for the past 3 years. Not a recommendation. Just sharing my notes. Views invited.

6 Likes

Just to keep the discussion going:

What IS the fair market value? Would like to hear opinions from everyone who is tracking it on this forum.

Earnings discount, asset based, P/E multiple – no matter what technique you use, kindly share it with a back-of-the-envelope type calculation.

Would help us gauge a rough range. How the market prices it is out of our hands and so, does not matter, if we assume market will converge with our logic in the mid to long term…

2 Likes

Factor 1: The MD has made it clear that commercial RE will be the primary focus of the company. Considering the same, the company has a potential and might monetize assets worth ~540 Cr. at right time(Max I: 50 Cr, 222 Rajpur: 18 Cr and Max Speciality Films: 470 Cr.). This should happen someday, which one can only speculate

Factor 2: Already built and ready to lease office space has the potential to earn ~31 Cr (Post Tax) on a yearly basis (Max Towers: 28 Cr | 80% occupancy at INR 100 Per Sq Feet and Max House: Phase-1: 13 Cr | 80% occupancy at INR 120 Per Sq Feet). This is the bird in hand and can be used as a basis to value the company. As of today, one is offered a cap rate of 5.8% (NOI/MCap: 31/534). Is that good enough for you to be a partner?

Both the above factors provide a bottom to the stock in my opinion and are part of my heuristics while thinking about the aspect of the back of envelope calculation. As usual, important questions do not have a straight forward answer in real life else I would not have failed in equity investment

Yet to materialize events such as new bids and pipeline in the form of Max Square are Birds in Bush. Hence, one must not base their valuation on these future promises.

Disclosure: Not a recommendation. Just a mental exercise that is published to hear the criticism of VP brotherhood:

6 Likes

f5b37115-f778-4bb0-9619-5bb5ad72d887.pdf (4.0 MB)

Investors representation

A few highlights from the con call today:

-

Specialty films to continue trend of healthy profitability. Will be used to reduce non-current liabilities. CEO Mr. Ramneek Jain conscious of MSFL’s lagging behind competitors in terms of margins and is working to be closer to benchmark. He also mentioned single plant-nature of the biz and lack of access to a port as reasons for not having better exporting volume.

-

No new update with Max Estates.

The biz development head, Mr. Rishi Raj, mentioned that they have bid for 3 million sq feet area in Delhi One. Out of this, approx. 70% will be commercial offering

They have received approval via vote of class of creditors. Final clearance is pending from NCLT court. They say that all approvals must be in place by end of this financial year (bit longer than expected, must say. This issue has been dragging on for a long time)

They are actively pursuing other distressed projects but there’s no clarity yet on these projects. -

Nothing new to share in MAS and their investments in Nykaa and Azure.

2 Likes

New investors presentationa3347980-c3f7-4bc6-867b-e9534748310b (1).pdf (849.3 KB)

1 Like

If I am not wrong, Mr Vachani, CEO of max was earlier associated with Dixon?

Sunil Vachani (uncle of Sahil Vachani and promoter of Dixon) and Atul Lall are co-founders of Dixon. Sahil was part of Dixon before he married Tara Singh, daughter of Mr. Singh and joined Max group.

1 Like

@Members

Your thoughts on this news? (Assuming this is true)

Also, if anyone can provide a source or link for the NCLT judgement, that would be helpful

Yes there is substance in the news. This was discussed briefly by the management in the past 2 concalls. Please refer to this comment for some brief details I shared earlier - Max Ventures – A Unique Demerger Opportunity

Additional details (from concall and the article):

- Matter is approved almost unanimously by the Committee of Creditors.

- So the management expects NCLT approval to happen by the end of this FY.

- Once approved and handover done, it will take 4 years to finish the project.

- 550 cr to be paid to the creditors over a period of 4 years. Receivables based on the existing bookings done is around 500 cr. So as Mr. Vachani said in one of the concalls - “NCLT deal is structured such that the inflows to Max Estates matches the outflows to the creditors”.

- Total size of the project is around 3 million sft. 1.5 mil sft is already sold out by earlier developer which Max needs to deliver. Out of the remaining 1.5 mil sft, 0.5 mil sft will be sold to the customers (by Max Estates) and remaining 1 mil sft is commercial RE which will be leased out.

- Project cost is around 2000 cr (I assume this includes the 550 cr to be paid to creditors). Partly will be funded by 0.5 mil sft which will be sold out by Max Estates (high-street retail and service apartments!!??) + 500 cr receivables from existing customers.

- As per article, the peak capex will be 400 cr and if needed there will be financial partner to be roped by Max Estates to fund the project. But as per Mr. Vachani, distressed projects will be completed undertaken by Max Estates alone, so not sure what is the way forward on the complete funding part.

Interesting times ahead.

(On a side note, this is a potential 3 million sft for Max Asset Services to service/manage in the future).

Disc: Invested

1 Like

Sounds great. Thanks for sharing this information, sir.

Have already boarded the flight. Now waiting for take off!

(Pardon the optimism)

2 Likes

Has Max House been inaugurated yet? They said it will be launched for leasing in August 2020. I sent a mail to investor relations regarding this about a week ago – No response yet.

Anyone else have any updates about this?

1 Like