The ratings continue to reflect the company’s established market position in the gold finance business, which accounts for around 70% of the loan portfolio. The ratings also factor in sound capitalisation, reflected in consolidated networth of Rs 6,037 crore and low gearing of 4.0 times as on June 30, 2020. Profitability remains strong driven by high gross spreads and low credit cost, while the funding profile is expected to remain stable. These strengths are partially offset by high operating cost in the gold and microfinance businesses, geographical concentration of operations and the associated risks, and potential challenges associated with the non-gold product segments.

Ltv 90% to banks will not affect Manappuram much as customer profiles of banks and NBFCs are different

Manappuram customer usually has low ticket price with average loan of 2 months

While banks have high ticket with long duration.

Manappuram advantage is long office hours as compared to banks and quick 15 min disbursal of loans

I think

If a customer wants a small loan than he will go to NBFCs instead of bank as he will save time and he is not interested in saving few hundred rs by going to bank

Also bank process is bit lengthy now worth to save few hundred rs for small ticket loans

Ashirwad Microfinance -August collections have exceeded 75% and those who have not paid are under moratorium

-We will go back to 90% plus collection in Microfinance by November December

Gold loan

Our advantage is 62 % of our gold loan is online gold loan

Plan :

50:50 gold non gold portfolio plan is still intact but it will take more than 5 years

Guidance :Looking for 10-12% growth this year

—————————————————

Market is closely watching the NPAs in non gold loan sector .As inspite of great results share price has not moved much.Its good to see that they have stopped Loan disbursements in non gold and concentrating on collections .Also its good that collections are gradually improving and now its more than 75% and management is expecting 90% plus collections by December.Stock movement will entirely depend on NPA overhang

Gold locker facility, online gold loan has helped them grow; Average life of gold loan is ~50 days; Average loan size is Rs. 40’000; Their customers choose them for convenience sake; Interest rate is not the biggest concern;

Microfinance: 7000 employees; 76% collection in August; will potentially reach 90% collection this month; Impact of pandemic was less in rural areas and affected the rural MFI customers less adversely; Extending fresh loans to existing customers; Moratorium is ~25%; Will reduce to 15% in the next 2 months; Should come back to near normal in 6 months

Vehicle finance: Collection in September will cross 95%; Will be back to normal in 6 month time

Fund raising: For this year’s growth of 15% don’t need additional capital; Able to raise CP money at 3.75%; Cost of funds will be 10-15 bps lower this quarter

Long term plans: 20% loan book growth on a consolidated portfolio at a 20% ROE; bottom line growth will probably be higher; will take 5-8 years to reach 50:50 gold and non-gold business mix

He is clearly overplaying this 10-15% growth story. He is reiterating the same forecast every week while knowing clearly that achieving it is like flipping a coin. Even the market leader Muthoot is struggling to do the same.

Thank you for your inputs @harsh.beria93.

Just wanted to know if I can find an independent source for the 3.75% CP money rate other than just relying on what the promoter is saying?

What would be the new average cost of borrowing be in this case?

I dont know where to find their commercial papers. Commercial papers do not account for a large part of their borrowings, so incremental costs have lowered total borrowing costs by 10-15 bps (as mentioned by management).

Update: The latest rating report contains more details about its various borrowing papers. Their commercial paper program is 4000 cr. (accounting for 11% of overall borrowing).

The gold loan market in India was valued at ~INR 2,921.42 Bn in 2019 and is expected to reach ~INR 6,275.40 Bn by 2025, expanding at a compound annual growth rate (CAGR) of ~12.75% during the 2020-2025 period.

The companies’ long-term IDRs were placed on RWN in March this year, as Fitch expected the pandemic to present further macroeconomic and funding challenges for the entities, heightening downside risk to their credit profiles.

The removal of the RWN and stable outlooks on MFIN and MFL’s ratings reflect the entities’ generally resilient performance in the face of significant economic disruption amid local measures to contain the pandemic," the agency said.

Real competition arrives here in the form of CSB bank. I have been saying that gold loan segment will see compression in margins due to competition.

The bank’s gross advances rose 11.92% to Rs 12,761.91 crore in Q2 FY21 from Rs 11,402.83 crore in Q2 FY20. Advances against gold & gold jewellery during the September 2020 quarter jumped by 47.10% year-on-year (YoY) to Rs 4,938.98 crore.

There are two ways to look at things - either market is strong for everyone or CSB is snatching market share from NBFCs. In either case it is better to play CSB for low cost gold loans.

I think the market is big enough for both NBFCs and Banks to grow. They are taking away share from traditional pawnbrokers. Also, Banks vs NBFC argument does not include the fact that on small-ticket loans 32k (average) and loan duration being small (90 days). The difference between what a bank would charge vs what nbfc would charge works out to be 300-400 Rs. This is not a serious motivation to change behavior despite lower interest rates. It is about convenience.

Let us wait for Manappuram(MAFIL) and Muthoot numbers before jumping the gun here. Growth in Gold loans was expected to be high considering high gold prices YoY(up 30%) and the state of the economy. CSB’s growth, though laudable, was on a comparatively lower base as compared to MAFIL. Whether this is a structural shift from Gold lending companies can be concluded only after looking at the numbers of MAFIL and Muthoot. Otherwise, I think what CSB achieved is really impressive. On a different note, I am hoping for good growth not only from the Gold lending business of MAFIL but also from the vehicle finance business. The collection efficiency of Microfinance biz is also a key monitorable.

Same scenario happened Post 2008 crisis ,good prices went up And all banks jumped in for gold loans

But no one persisted as it’s lot of work for gold loans

Issue with bank is That they are not Dealing exclusivly with gold loans .Gold loan is low price high volume business.

banks have multiple products and customer getS lost in bank and One has to spend lot of time figuring it proper counter and then proper Person to deal with it

Most won’t spend lots of time just to save few hundred rs

And here lies the moat for manapp and muthoot

Now banks are creating awareness for gold loans so more and more people will take gold loans but the max share won’t go to banks ,It will go to

Gold finance cos and local pawnbroker

I don’t get it when folks say that they have moat against everyone else. The pawnbrokers have survived for long despite demonetisation and these two NBFCs are growing at industry rate only and not faster than the market. Secondly, CSB is not just another bank. It is owned by an aggressive promoter unlike in the past and this has 33% loan share from gold with good expertise historically. It will not be wrong to say that this is a gold loan focused bank and these NBFCs have not faced a focused competition like this. I also got an impression that gold loan NBFCs are facing stiff competition from small finance banks offlate. If I ask any rural guy, he will be definitely trust a bank any given day than an NBFC. There may be locational and logistical advantage for the next few years at least but mr. market would start recognising this competition sooner than later.

What prof missed was NPA in Microfinance post Covid .Market is smart and waiting for npa picture to become clear before they assign high pe and high book value .And till that rerating won’t happen .

And it may derate it if there is substantial increase in NPA

Pre covid market gave it 15-18 PE.So market takes into account everything and does not value just on PB.

It looked more biased view as there was nil mention of most crucial factor non gold NPA post Covid

Over the last 2-3 years I understood one thing that every story has few positive and few negative points .No one can predict what’s going to happen in future and if story plays out positively then people say “ bola tha na Maine “

And if it plays out negatively than “stop loss ne Bacha diya”

Luck plays major role in exuberant returns and logical analysis plays crucial role in downside protection and average returns

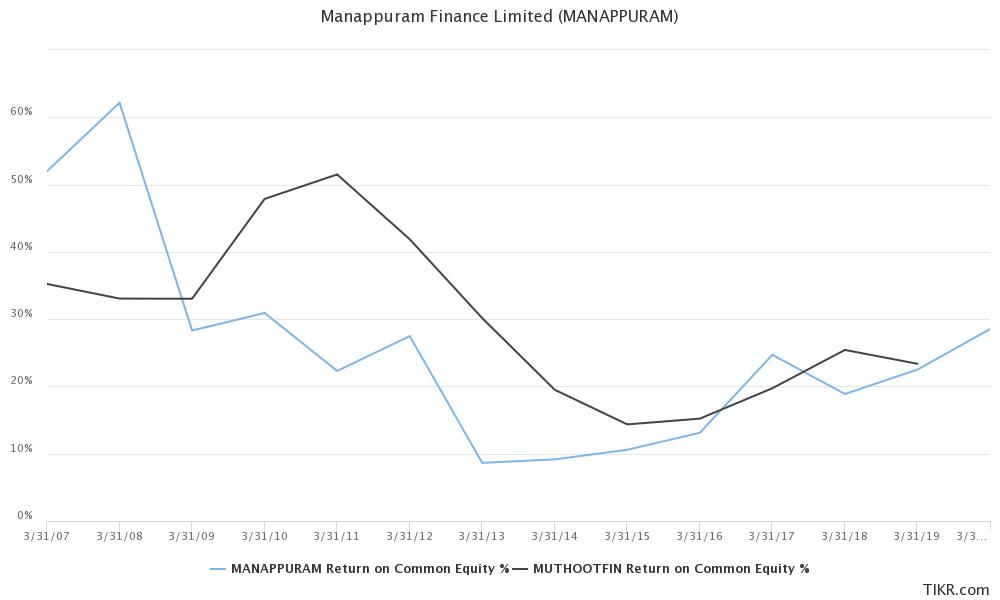

ROE is the bridge between P/B and P/E (PB = ROE*PE). Anytime, P/E looks low but P/B looks higher, it means market is saying that the current ROE of the business is not sustainable i.e. the business is going through a cyclical uptrend. Does this apply to gold financing? Hell yes! ROEs of Manappuram and Muthoot are shown below (taken from tikr).

In the last cyclical downturn, ROE of Manappuram went down to single digits (close to cost of capital) and P/B also went below 1. It will be prudent not to extrapolate 30% ROEs as the inherent business of gold financing depends on gold prices which is cyclical. Over a cycle, this business is still quite attractive making ROEs much higher than cost of capital. But 30% ROEs cannot persist forever.

A good way to play these cyclicals is to wait until market gets excited about them and starts paying a high multiple (>4x P/B) during a business upturn and sell it to the optimistic participant. This has not yet happened for Manappuram because market is skeptical of their non-gold finance lending (vehicle, microfinance) but has already happened for Muthoot (look at PB ratios for Manappuram and Muthoot).