ICICI bank has also jumped into the gold loan bandwagon. New focus is being given on gold loans .

A friend of mine ( staying in a Metro city ) who used to take gold loans regularly from Muthoot for working capital in his business recently tried SBI gold loans and was satisfied with the process. Interest was lesser than Muthoot and the procedure was quite easy. Atleast in the big cities Manappuram and Muthoot will get conpetition. In Rural areas traditional gold loan companies will be at an advantage.

It is well known that gold loans are the safest form of lending. Inspite of that only manapuram and muthoot have been able to scale up and do well in this field . Other great nbfc companies have not been able to scale up in this segment. Unlike other segments here the consumers have to trust you more because they have a lot to lose in case of default. Hence it becomes easier for players which have a big scale. Also there is a lot of unorganised sector in this field. The rate of interest charged by the organised players is much higher than the organised market. Hence i believe there is lot of leeway for players like manapuram and muthoot to grow.

I dont think competition from other banks , nbfcs will make much difference to these 2 players here. There is a reasonable entry barrier in this field which people dont recognise. Otherwise it would make no sense that such a lucrative business is seeing only 2 major players and is insulated from competition.

Disc-invested in manappuram

SBI and HDFC starting gold loan at 8% range in comparison to double digit loan rates of mannapuram and muthoot…Do u think in long run this can have an impact on the returns of the gold loan companies

Historically, a lot of banks were offering gold loans… They are offering gold loans even now, the only difference is gold loans are getting a bit of attention & priority from banks now, given the current Corona pandemic & the risk possessed by it.

But , I personally think, it is not going to affect gold loan NBFCs like Manappuram & Muthoot, bcos they cater to a different client base. Broadly ,we have 3 different kinds of offerings:

Local Money lenders - charge highest interest rate, provide little security of the collateral gold,yet the most convenient option. Loans get sanctioned in mins or hrs

Banks - charge lowest interest, provide high security of the collateral gold, yet the least convenient option,as it takes days or weeks to process the documents n sanction loan.

Gold loan companies like Manappuram & Muthoot finance - They are somewhere in between the above two extreme offerings. They charge high interest , provide high security of collateral gold, convenient option as compared to banks . The processing happens in a matter of few hours. These are generally low ticket ( small loan amount), short term loans , provided to cater immediate credit needs for events , functions, small business , small auto purchases etc… The customer base is different from the one that take credit from banks. Here the need of customers is immediate , short term credit and where there is a security of their gold assets. They are ok with paying a premium interest for that.

So, the bottom line is , in my opinion , the banks offering gold loan shouldnt affect Muthoot finance & Manappuram finance Ltd(MFL). Having said that, if the banks were to leverage on technology, improve their operational efficiency & sanction loans in a matter of hours, then they might be a threat. Although, the likelihood of that happening is very less( well ,lunch breaks are more imp for some banks )

On the other hand, Bajaj Finance is planning to enter into the Gold loan space. Given its competent management, operational efficiency & its ability to leverage on technology, if it starts spreading wings in this space, it can pose a serious threat to MFL & Muthoot.

Hope it helped.

Disclaimer : I own both Bajaj Finance & Manappuram finance . They together contribute 30% of my portfolio. So, my views may be little biased. Do your own research before investing.

Extraordinary results considering the offices were closed for half the quarter. Their digital strategy for gold loans has helped big time and remember, Manappuram has much higher number for online gold loan customers than competitors. Microfinance numbers are not great as it barely broke even. All in all, the impact of Covid is barely felt by gold loan companies and growth should come from next quarter as gold prices are at ATH

The profits have come largely from lower costs than increase in AUM or even lower interest costs. When you keep your branches shut, your costs remain deflated temporarily. Moratorium is still high in non-gold biz so I would wait for Q2 results to pass the judgement as they have 400-500cr of accrued interest for the Q1.

A key monitorable for me was their vehicle loan book which was grown at a rapid pace in FY18 and FY19. CV vehicle portfolio was 1’344 cr. in FY20 (out of total AUM of 25’225 cr.) Management had revealed that 10% (both by value and # of customers) of the book was under moratorium in last concall. This was in stark contrast to industry where other players had very high NPAs in their CV divison (eg: Shriram has 9-10% NPA; Bajaj finance has 50% vehicle book under moratorium as of Q1FY21). Management said that this quality is because they don’t lend to fleet operators, but mostly to individual truck owners. This was the exact management commentary last quarter:

As the management didn’t release NPA figures last quarter, it was very hard to evaluate the book quality. They finally reported NPA of 9.9% in FY21Q1 and 6.7% in FY20Q4 which is more in-line with industry standards. Also, their home loan book is not very clean, i.e. it has 5.1% GNPAs as of FY21Q1. However, management says that their more recent lending quality is much better (1.5% GNPA). The real lending quality will be known in a few quarters.

The saving grace is that gold prices have gone up leading to increase in gold AUM (although gold tonnage has been flat YOY). Company is very well capitalized and has raised lots of liquidity this quarter. Looking forward to reading the management trancript.

Q1FY21 -

Gold loan is the only saving grace here and the fact that other business lines are smaller in comparison. They have provided 4-5% of book on the MFI side, and 7% of the book on the vehicle loan side. For COVID. This is when the moratorium is yet to be lifted . The pain they can be seeing in their books seems to be huge. Or maybe, they are front-loading it all.

Excess provisions in the last two quarters are close to 1400 crores appx.

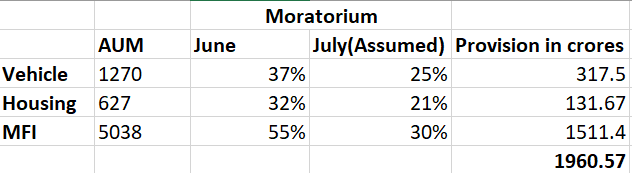

Back of the envelope calculations fetch me the below numbers

Out of 2000 crores, 1400 crores have already been provided in the last two quarters which makes me believe that provisions are frontended. The management has been very conservative in estimates every time in the past. I expect NPA numbers to stay under control in the next quarter and overall profits to show growth sequentially. Pain still remains in the MFI business, but with rural pickup, collection efficiencies could reach 90% by next quarter. It wouldn’t take much time for the company to move into a growth trajectory, thanks to Gold loan business. Still remains an attractive company in the NBFC space for the foreseeable future.

Not that surprising since there has been too much of a run up recently hence expectations seem higher than what the results indicate. Moratorium in non gold portfolio is a big hang up. A lot of uncertainty for the next two quarters.

Cost of capital is finally coming down sharply for Manappuram, from 8.75% a few weeks back to 8.35% today. Ashok Leyland (same rating) had raised debt at 7.65% recently (link)

)

)