Authorised Mr Nandakumar to initiate further discussions on behalf of the company on investment opportunities available with the company.

Unfortunately, the announcement is a bit difficult to understand. Still not clear - whether this means the company is looking to sell part of its stake or is it looking to acquire another business as an inorganic growth opportunity.

I may be wrong, but I think it is kind of straight forward that Manappuram is exploring new opportunities to invest further as it is one of their stated objectives to diversify away from gold loan financing. If someone else is investing in Manappuram, they would have notified as divestment options rather than investment opportunities!

For gold loans, which are adequately collateralised, why does the interest rate be northwards of 20%? Even mincrofinance loans without any collateral are being given at this rate.

With much improved performance this quarter, we have now put the fallout from demonetisation behind us. From now on, it will be business as usual, we expect growth to pick up to the levels we saw before demonetisation," said V P Nandakumar, MD &CEO, Manappuram Finance.

The company is looking at fintech investment or strategic buyouts but there is nothing concrete yet, said Krishan.

Sorry this may sound like a very amateur question. But can somebody explain what is the difference between these 3 items with a live example if possible?

Suppose bank has financed a loan of Rs 100/- but due to any reason bank is unable to recover the loan amt plus interest and as per RBI guidelines if bank is unable to recover its loans say in 90 days, the amount has to be transferred to NPA category. Bank has to create provision on this NPA after classifying it sub standard, doubtful or loss asset. This provision is deductible from profits of the bank also. In this case, if the account is classified as Sub standard and bank make a provisio of 10%, then the provision in this case will be Rs 10 and net NPA will be 90 i.e. Gross NPA Rs 100 - Provison Rs.10.

Better to always refer to RBI glossary for definition. e.g

Net NPA = Gross NPA - (Balance in Interest Suspense account + DICGC/ECGC claims received and held pending adjustment + Part payment received and kept in suspense account + Total provisions held).

Management have been guiding 20% growth all the time. But the reality is different. Review the YOY growth rate and you will get the picture. Diversification is good. But they are still a gold loan company predominantly. Therefore when the primary business growth rate falters it is a major red flag. Also gold loan have no direct relationship with demonetization or GST and these are no reasons for reduction in growth rate. I agree the valuation is cheap and I think it is cheap for a reason.

Hi all,

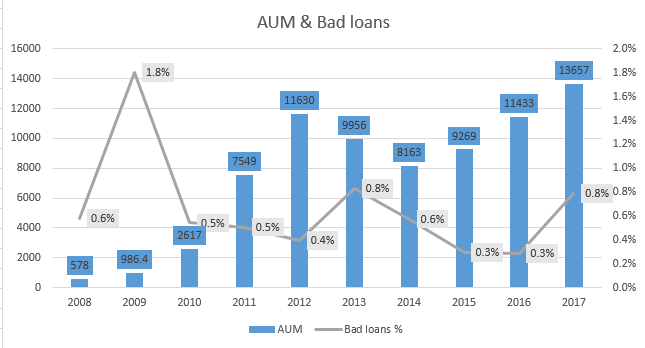

This is the first time I am trying to analyze an NBFC. So please pardon my ignorance. I have tried to assess the total write offs that Manappuram has made over the years against the total AUMs in a given year. Here are the numbers.

Year

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

AUM

578

986.4

2617

7549

11630

9956

8163

9269

11433

13657

Total write offs

3

18

14

38

46

83

47

27

32

108

Bad loans %

0.6%

1.8%

0.5%

0.5%

0.4%

0.8%

0.6%

0.3%

0.3%

0.8%

All numbers are at the consolidated level.

Bad loans have been derived by adding up “Provision for standard assets” & “Bad debts written off and provision for bad debts” from Cash Flow Statements for corresponding years.

Total write offs of 416 Crs in 10 years for a company with an AUM for 13700 Crs isn’t bad at all.

Puneet Kaur Kohli has joined Manappuram Finance as Group CTO. Headquartered in Cochin, Manappuram Finance is one of India’s leading gold loan NBFCs. Incorporated in 1992, Manappuram Finance has 4148 branches across 27 states/UTs with assets under management (AUM) of Rs. 13,723 crore and a workforce of 22,112.

In her new role, Puneet Kaur Kohli will be based at the company’s headquarters in Cochin and will report to the MD & CEO of Manappuram Finance VP Nandakumar.

It is interesting to note that Manappuram Finance has always been an early adopter of industry-leading technologies. It was one of the earliest to adopt the core banking platform despite the fact there were no ready-made software solutions for gold loans NBFCs. It developed its own proprietary solutions, and this technology platform has been one of its core strengths. The firm has leveraged technology in streamlining procedures to reduce turnaround times in gold loan disbursal and in implementing advanced risk management practices. It launched “Online Gold Loans” in 2015.

As the Group CTO, Kohli will be tasked with high priority projects aimed at the digital transformation of the gold loan NBFC. Her near-term priorities at the company including e-KYC, transitioning the ERP on cloud, adoption of analytics for customer centricity, mobility initiatives and creating a single view of the customer.

Prior to this, Kohli served as the Group Executive Vice President IT & CTO at Bajaj Capital. In a career spanning 24 years, she has worked with companies like Motorola, Reliance, Duncans, Carrier Aircon, UK Land Investments, Bharti Airtel Limited, Soma Networks and Motricity in countries namely, Dubai, US, UK, Canada & across APAC.