I will try and write on this thread more frequently. One area that I have been exploring in the past few weeks is global investment opportunities. I have found that outside India there are high quality structural compounders, often with higher growth rates but available at lower valuations. Let me briefly describe a few that I have been reading recently:

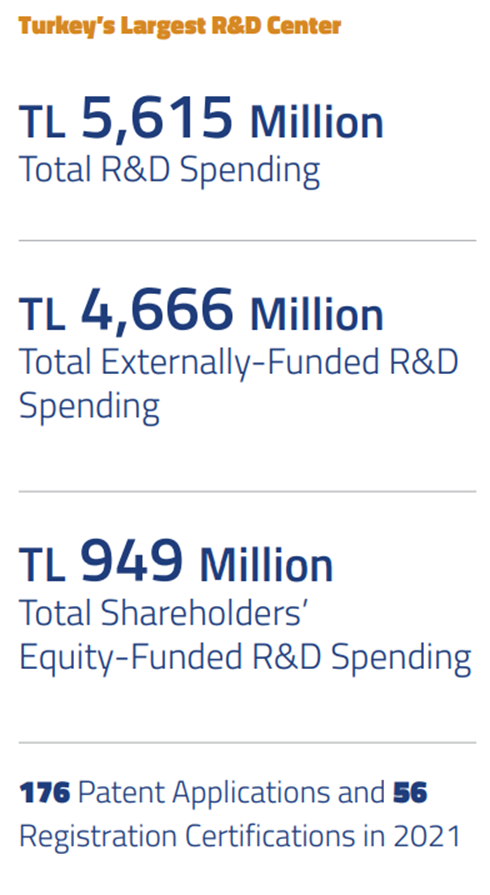

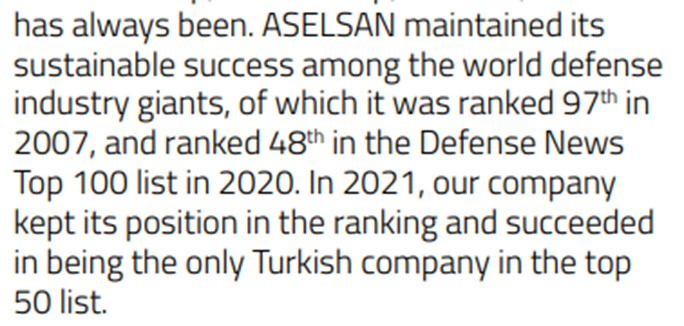

1 Aselsan-Largest defense company in Turkey, among top 50 in the world. This is also an interesting case of how reading a book (The Power of Geography by Tim Marshall) helped me connect the dots with a company. Also, they spend >20% of sales on R&D! The RoE for CY 2021 was 27.6% and the average RoE for the last 3 calendar years for 25.6%. The long-term debt to equity is almost zero. PAT growth is >25-30%.

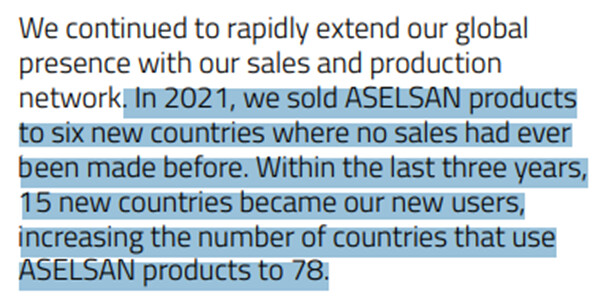

Sales are majorly to Turkish army…

…but even for domestic sales, they take payment in foreign currencies (while incurring costs in lira)

Here’s the punchline- trailing PE is 7x!

https://www.aselsan.com.tr/032022_4232.pdf

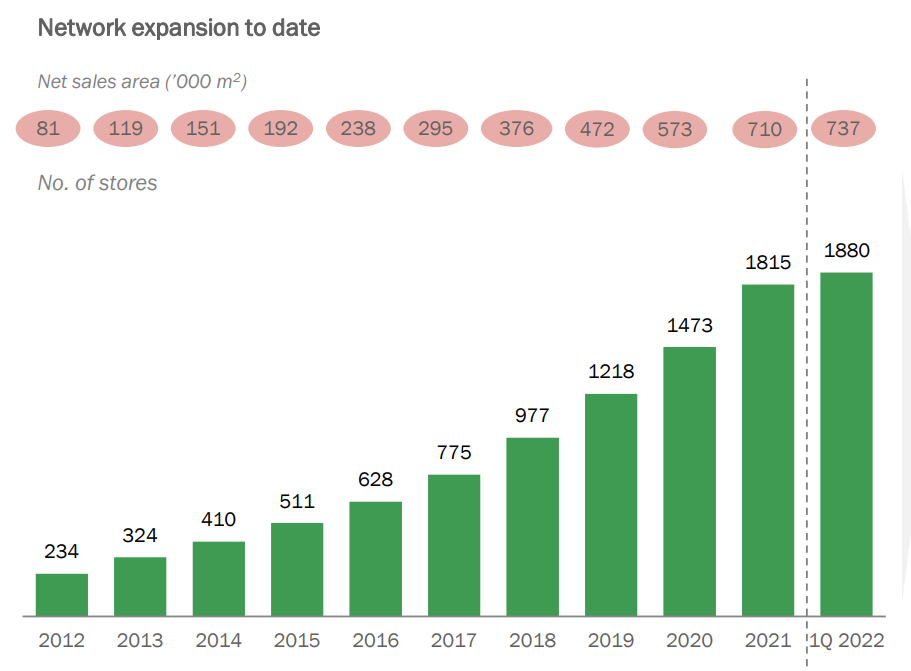

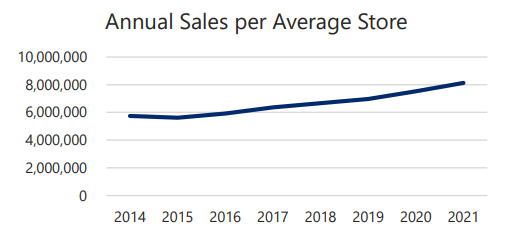

2 Dino Polska- A high growth frugal grocery retailer (supermarket chain) in Poland. Stores are majorly in rural towns, outskirts etc. Almost all stores are owned, not leased. Nil store closedowns since 2007. They have the lowest prices.

Store count growth…

…+ sales per store growth

3 Sechaba Brewery

Disc- no holdings in any of the above as of now. Will update if and when required.