Topline decreased,true. But other income increased drastically. Overall expenses decreased,asset increased. We must appreciate mngmnt for all these which inturn gave profit in Q-o-Q. Also expansion plan on cards. Overall not a bad result I see.need to see next quarter.

The standalone results qoq are decent, and yoy is slightly on the lower side. Annual FY18 results are good as compared to FY17. The receivables continue to be on the higher side at 12-13%.Consolidated debt is down from 19 cr to 3.6cr, which is a good sign.

3 Likes

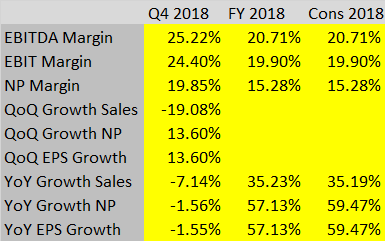

#MaithanAlloys Awesome set of numbers: Margin expansion

Key updates:

Organic expansion: 275Cr 120k Tonne new facility to come up in 30 months. Already have cash and investments of more than ~340crs

Inorganic expansion: Actively look for stressed assets

For long time they are operating at 95% capacity so growth could only come from higher price. Now, things are more clear with greenfield expansion plus strategy to acquire some stressed assets. Strong balance sheet will ensure that they don’t have to take additional debt for expansion and they have a strong track record of timely expansion with in the estimated cost.

Dividend of Rs 3 looks like peanut when they are earning Rs 100 as eps but make sense to conserve cash as they plan to use cash for expansion/acquisition.

My take: Good for long term. No additional growth expected for atleast 2-3 years so will be a good candidate for SIP investment.

Disc: Vested interest and biased views

7 Likes

Everything looks great, Power cost almost doubled from 46cr in M17 to 85cr in M18 quarter.

Last year was a oneoff rebate on power tariffs. Please check the details of previous year announcements.

2 Likes

But that power rebate was extended for 2018-19 as well by AP Govt. So it should have got similar discounts. Maybe someone need to contact their Investor Relation for more clarity.

1 Like

Couple of interesting data points :

- MA operates in a cyclical industry

- This industry has excess capacity

- Yet, MA has been able to sell its alloy throughout - so much so that it is going for an expansion by 50% over next 3 years

Combining the above three points - either the management is fool to expand capacity in (cyclical + overcapacity) market or is very confident of its own future growth.

Now, Based on past results it seems to me that management must be confident.

Took small position based on this thought process. After satisfying myself with financials and management.

Would perhaps be a slow growth for next few years though.

2 Likes

Hi - Request you to please share data that indicates that the industry has excess capacity. Maithan products are input to steel industry and steel stressed assets wouldn’t have seen interest if the statement were true. Thanks

- India produces 3.5 mil tonnes of Ferro alloy and consumer 2.3 mt, rest is exported.

- silico managanese is expected to see and increase in supply be around 5% to 14 mt from 13.2 mt while consumption is expected to grow by 2% to 13.96 mt from 13.7 mt.

These two points indicate that domestic market has overcapacity. For details pls go thru 2017 AR of the company.

Investor Presentation on the Audited Financial Results for the year ended 31st March, 2018.

1 Like

Are you invested in this counter? really good correction in recent sell off. Do you use such correction to add?

I had booked most of my holding earlier around 1000. I will relook at it later. Right now using the correction to shift to better quality companies.

sir which companies are you looking at currently?

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=324da3a8-f796-428e-93f5-9ca8791818ba

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=95c3cd07-9def-4bf3-947c-bd491c57de74

2 entities have become part of the promoter group. These 2 together represent more than 4% of the equity. Also these changes have happened during the period of the stock getting beaten up.

I have a doubt. How is this action supposed to be perceived? Since effectively it will raise promoter holding but still no fresh buying has taken place by them at the lower levels, only a sort of reshuffling. Obviously fresh buying at the lower levels would’ve been a huge positive. How should this be interpreted?

When did these companies aquire these shares? If they were not promoter companies at time of acquisition and deals were not large enough to be disclosed then the buying must have been done around this time.

it is very hard to say that the management has the best interests of employees and shareholders in consideration. if we look at the last 3 years of annual reports, then the director’s remuneration has increased from 14-15 to 16-17 considerably, 5.76 cr to 14.25 cr. while these nos in absoulte terms are big, as a % of salaries and wages they are 62%, 49% and 79% respectively. MA had following no of employees on its payroll, 367, 574 and 586. the total salaries and wages divided by the no of employees gives an annual income of 2.5 lacs for 14-15 and 15-16 and 3 lacs for 16-17. so the average salary increased only 20% while that of directors went up 3 times.

if i assume that maithan added some more employees in 1718 say 600 and increased their salaries by 20% so avg salary would be 3.6 lacs which is quite a big jump to assume in 1 year. even then the total expense on salaries and wages will be 19.6 cr. the total expense was 45.2 cr. i take 2 cr for provident fund and staff welfare expenses although this figure is around 1 cr. even then, the director’s remuneration works out to 23.6 cr which is a whooping increae of 9 cr. infact the director’s remuneration would now exceed that of salaries and wages.

this clearly indicates that the promoters are benefitting the most even abnormally with the increase in profits rather than sharing it with the employees. compare this to the dividend announced of rs 3 per share and with 2.9 cr share, the minority shareholders have 75 lacs, the total dividend works to 2.25 cr only.

management clearly is not following corporate governance fully. i am not invested in the stock but still studying it.

4 Likes

But they are following the SEBI cap for KMP salary. Which is 10% of net profit in a given year.TCS ceo gets 250 times more than what median salary of employee and average salary hike this year is around 11% greater than employee hike.I am not saying which promoter is good or who is bad.But there is instances.

yes true, however, TCS is a 100 billion dollar company, maithan is just starting out. but the consequent increase in promoter remuneration is mind boggling. a company talks about creating value for shareholders in the annual reports but practices different things.

there is one other instance that i noticed. the company is getting involved in trading of goods more actively than before which does not make sense when they should be focused on operations. also this activity is not yielding any substantial returns. for example in 1617 to 1314, the purchase of traded goods is 74, 108, 320 and 209 cr. the sale of these goods yielded, 78, 111, 320 and 212 cr. so there was a profit of only 0-4 crs over such a big ticket item. while this should have served as a lesson for the company, in latest 1718 FY, they again increased the trading to 164 cr. it may be a good company but the way it is doing some things is not understandable.

2 Likes

Topline growth seen but net profit slightly affected compared to last quarter due to 30 cr inventory increase.

Please correct my observation and add any missing point.

1 Like

Well, “Purchase of traded goods” = 30.89 Cr (2nd item in Expenses)

Inventory has decreased by 8.6 Cr (3rd item in Expenses).

Yes, the 8.6 Cr is added, and the total YoY difference due to Inventory turns out to be 6.5 + 8.6 = 15 Cr.

Equalizing for this, YoY bottomline shows growth of 30%.

Seems a good result!