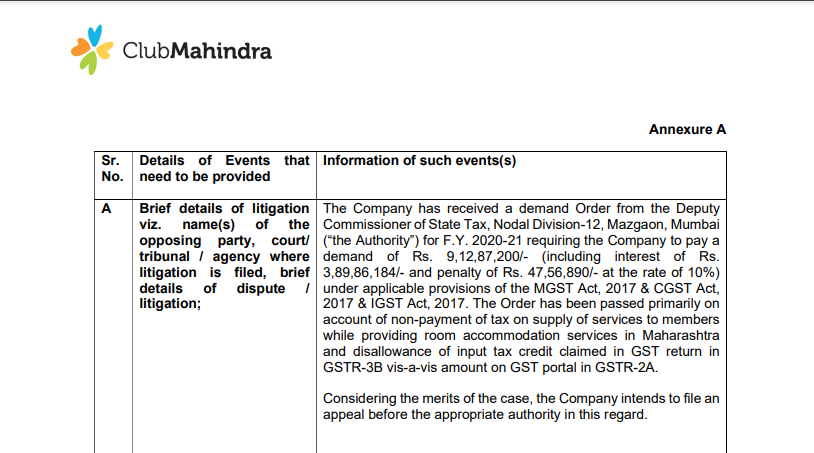

Company has received a GST demand order for ₹9.13 crore from the Deputy Commissioner of State Tax, Mumbai for FY 2020-21.

Total Demand: ₹9.13 crore

- Tax: ₹4.75 crore

- Interest: ₹3.90 crore

- Penalty: ₹47.57 lakh

Quite an huge amount

Company has received a GST demand order for ₹9.13 crore from the Deputy Commissioner of State Tax, Mumbai for FY 2020-21.

Total Demand: ₹9.13 crore

Quite an huge amount

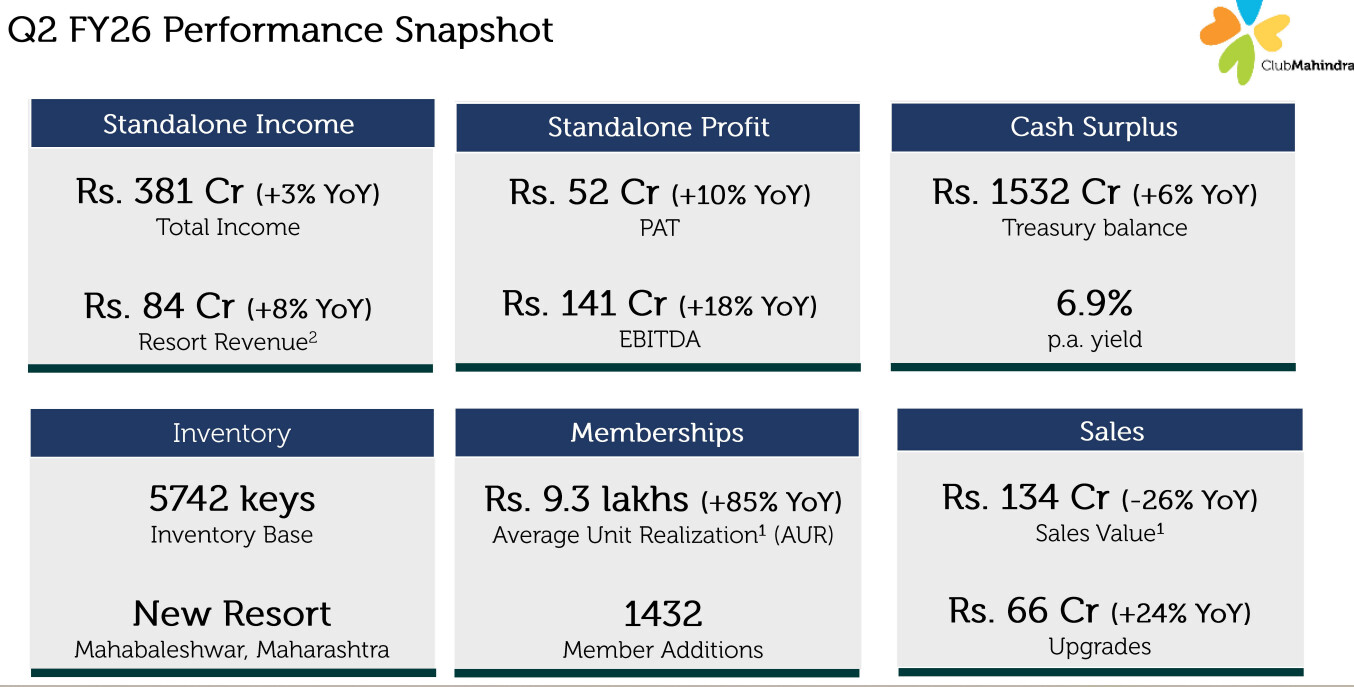

New Member additions in Q425 are down, seems MHRIL is focussing on the high end customers, hence average unit realisations have gone up; also this seems to be their response to the often complaint that members are not able to get rooms for booking.. The member to room inventory ratio has also been continuously improving, and I feel the management may want to focus on higher margin customers for the next few years.. the pace of new room inventory addition if broken down to quarters is also less than 200/quarter (4000 in 20 Qtrs (2025-2030))

Instead of adding 200keys this quarter, MHRIL saw a degrowth of 53 keys!

With a treasury balance of 1576Cr, yielding 8.8% pa, almost 35Cr profit seems to be through passive income itself; but they are also showing FOREX loss of 28.1Cr this qtr vs gain of 3.4Cr last year same quarter. Need to understand whats contributing to these forex loss, since HCR (Finnish subsidiary) loss has reduced over last year.

Degrowth in number of keys continues this quarter, with a drop of 52 keys. and so does the new member addition count, which fell from 1524 in previous quarter to 1432 this qtr.

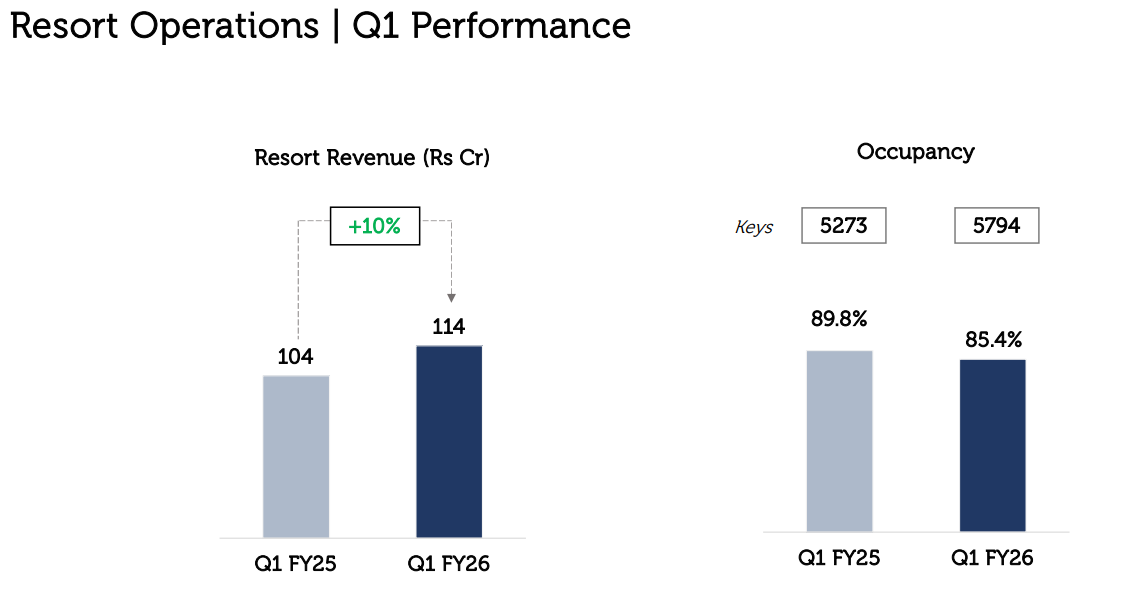

Treasury Balance also reduced along with fall in Yield from 8.8% to 6.9%!!

Interest expense has gone up by 10Cr as compared to same quarter last year; out of which 8Cr the firm says was on account of interest on tax expenses for prior years. Wonder why, as they have been cash rich!!

Q3FY25 they had mentioned target to add 1000keys in next 5 Qtrs, but 3 quarters down they have added only 50 keys!! 90% underperformance!!

Few further thoughts on this otherwise hopeless company, based on the changes I observe during last couple of years:

Net net - Increase in membership price has offseted the decrease in member intake, however, overall cashflows accrued from new member addition has not changed. But what probably has changed and impact in long term is the next point.

Decrease in Advertising and Marketing costs translating into higher cash flows over long term - The focus on high end customers majorly through referrals, may result in decreased sales / marketing / promotional efforts, thus decreasing this expense, which has been a major portion of Mahindra Holiday’s cost structure.

Increasing room inventory translating into high service quality - The plan to double the room inventory form current 5000 to 10,000 in next 5 years (by 2030), along with fewer additions of new members, may translate into better service quality. The regular customer complain of not being able to get booking when wanted, may be reduced to some extent.

Entry in traditional resort business - The company probably has realized that its existing business model requires a change, and hence, it is entering into traditional resort renting business.

Lets see how the future unfolds, however, past suggests, nothing can move the company :)

Disclosure - Invested and biased

True. The foray into traditional hospitality is an admission of the fact that the timeshare business is not scalable. But in traditional hospitality, they are five years too late.

What is this traditional resort business, can you pl give more details?

Few thing I came across, 1) they target highend Mahindra car buyers by offering few days stay voucher. 2) short term point based plans. 3) Talk of improving room to member ratio

To me it will be positive if they 1) Could reduce sales cost. 2) Reduce occupancy (yes, reduce), by improving room to member ratio 3) Use cash to build than earning meager interest on it. 4) Provide better value proposition in overseas resorts.

Disclosure : No position