Lower vacancies are due to the fact that people can not travel to every destination every time. There are off seasons. Will you go to a beach or deserts in May-June? or mountains during rainy seasons or winters (other than snow / New Year Holidays)? Occupancy can never be 100% for any hotel chain anywhere.

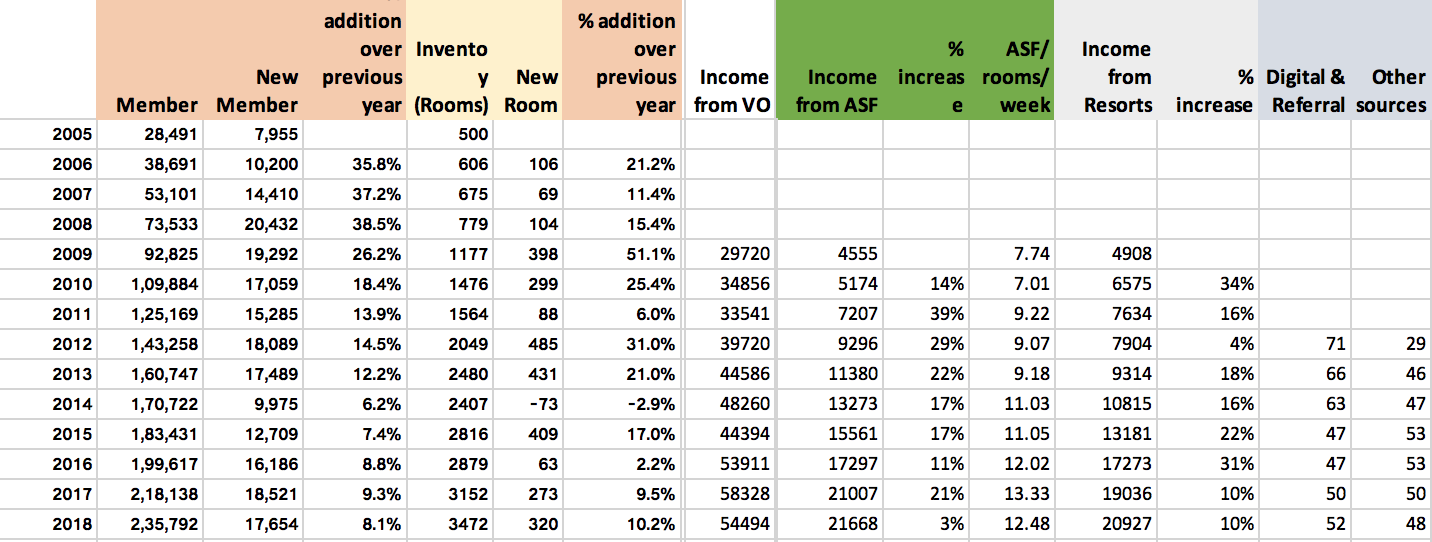

180 lakh weeks at an average occupancy rates of 75% mean 945 lakh nights and to satisfy all 235 lakh customers average is just 4 nights per customer and the customer base is increasing more than increase in no of rooms. So all the members have to upgrade their rooms which is not feasible.

**I have assumed 75% occupancy instead of 80% reported as I have visited their properties. They have special rooms for non-members which are smaller and do not have valley/beach views and these rooms are given to gift voucher customers or sold on other websites.

Regarding your other point, to value this as a hotel business instead of timeshare, it is not possible as timeshare is a long term contract involving 25 years.

In case people are not satisfied and are unable to get rooms during the seasons they wish and they withdraw their membership, the growth will turn into de-growth for the company but remaining customers will start enjoying their memberships again… satisfied customers mean more members… which means the cycle repeats… So, IMO the company can not be valued on the basis of hotels it owns, unless the company stops membership program all together…