He seems to be holding other positions in multiple Mahindra group companies. Like he is the MD of Mahindra Agri Solutions Limited as well.

https://www.linkedin.com/in/ashok-sharma-83828b25/?originalSubdomain=in

Hello,

I had attended the AGM and have prepared the notes. I have tried to catch hold of everything the management said. I hope it is helpful

.MAHINDRA EPC AGM NOTES.docx (12.1 KB)

disclosure: invested from lower levels

7 Likes

results declared by the company

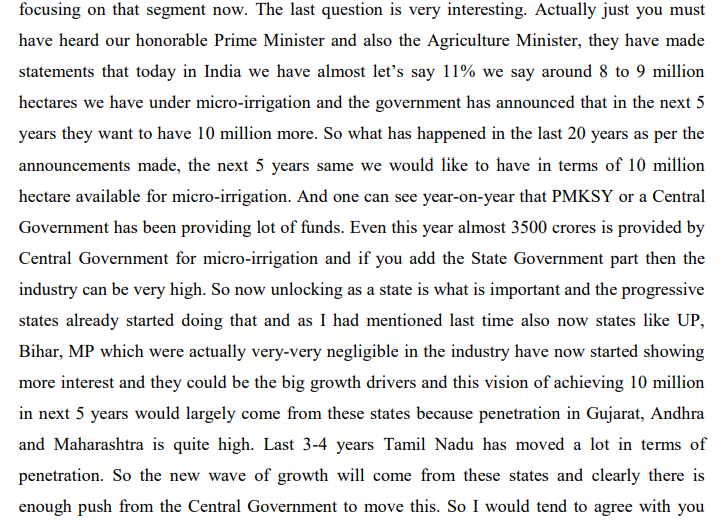

Was reading the concall transcript of H1. A must read for all the people invested gives a good idea as to what is going on in the industry.

Am attaching a few interesting things that caught my eye.

this is what the company expects from the industry going fwd

Disc: Invested from lower levels. Views may be biased.

1 Like

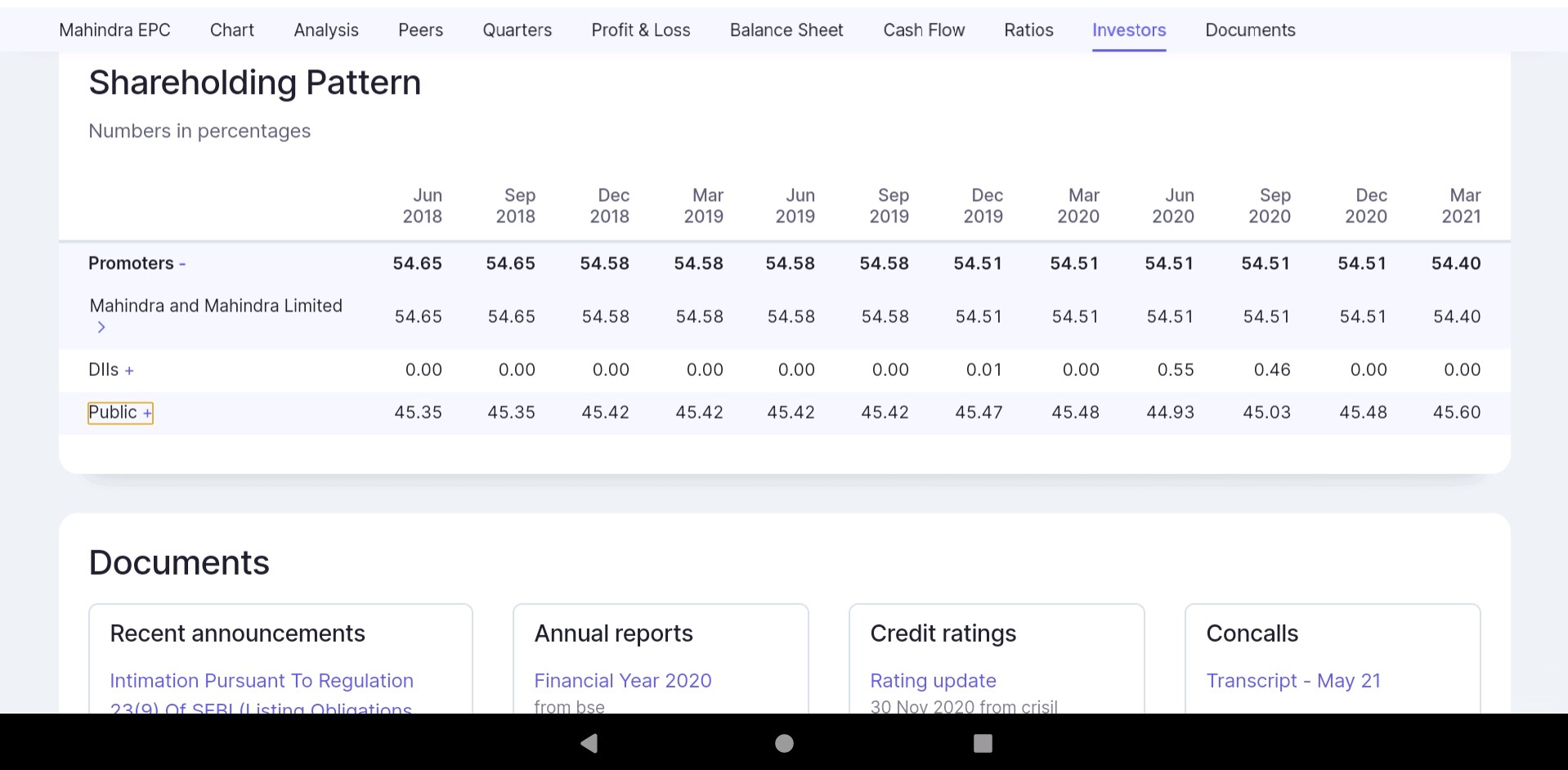

Promoter reputation is the strongest moat of this company. However it seems promoters are unloading shares every few years.

1 Like

Thats not share reduction, its impact of ESOPs.

2 Likes

“Mahindra EPC Irrigation Limited Q2 FY-22 Earnings

Conference Call”

29" October, 2021

MahindraEPC.pdf (874.7 KB)

Q4 numbers are also good. Revenue seems to be All time high. Profit before tax is also very high. anyone tracking it? Seems company is now consistent with good results.

Disclosure- Invested

2 Likes

Bullish commentary by the management on business outlook.

Subsidy business remains a major concern. Management refrained from giving any growth guidance.

2 Likes

The biggest positive is promotors. Microcap. India is agriculture heavy country but this sector is still underdeveloped. But no significant growth since so many years remains much of concern about future growth. What if it stays same for next 10 years like previous 10 years. Please share new updates regarding this company if anyone is tracking. Would love to see updates in this. In radar.

3 Likes

Main problem with them is their subsidy- related business where overdues sometimes takes years to get cleared by the government. Company has not been able to capitalise the opportunity well in this sector. In last concall also management did not give any positive commentry in this regard. Company mat grow topline rather comfortably but bottom-line remains a key concern

1 Like

This itself may be the problem. Being a small company, it may not be the priority for the promoters. Past business performance also justifies this notion.

The promoters acquired the company at a very cheap valuation in early 2010s. Reliance also bought such small companies at a distressed or cheap valuation. But later they did not pay attention to such companies maybe because they did not consider it important.

2 Likes

True. Let’s track and see…and if something good happens in this it will be a good opportunity.

1 Like