Lux AR is out

Highlights from AR on future strategy for growth - Bold callouts including past weaknesses

- Launch and Scaling Lux cozy world - customer engagement, product pricing validation, data analytics play - brand ambition to convert push to pull

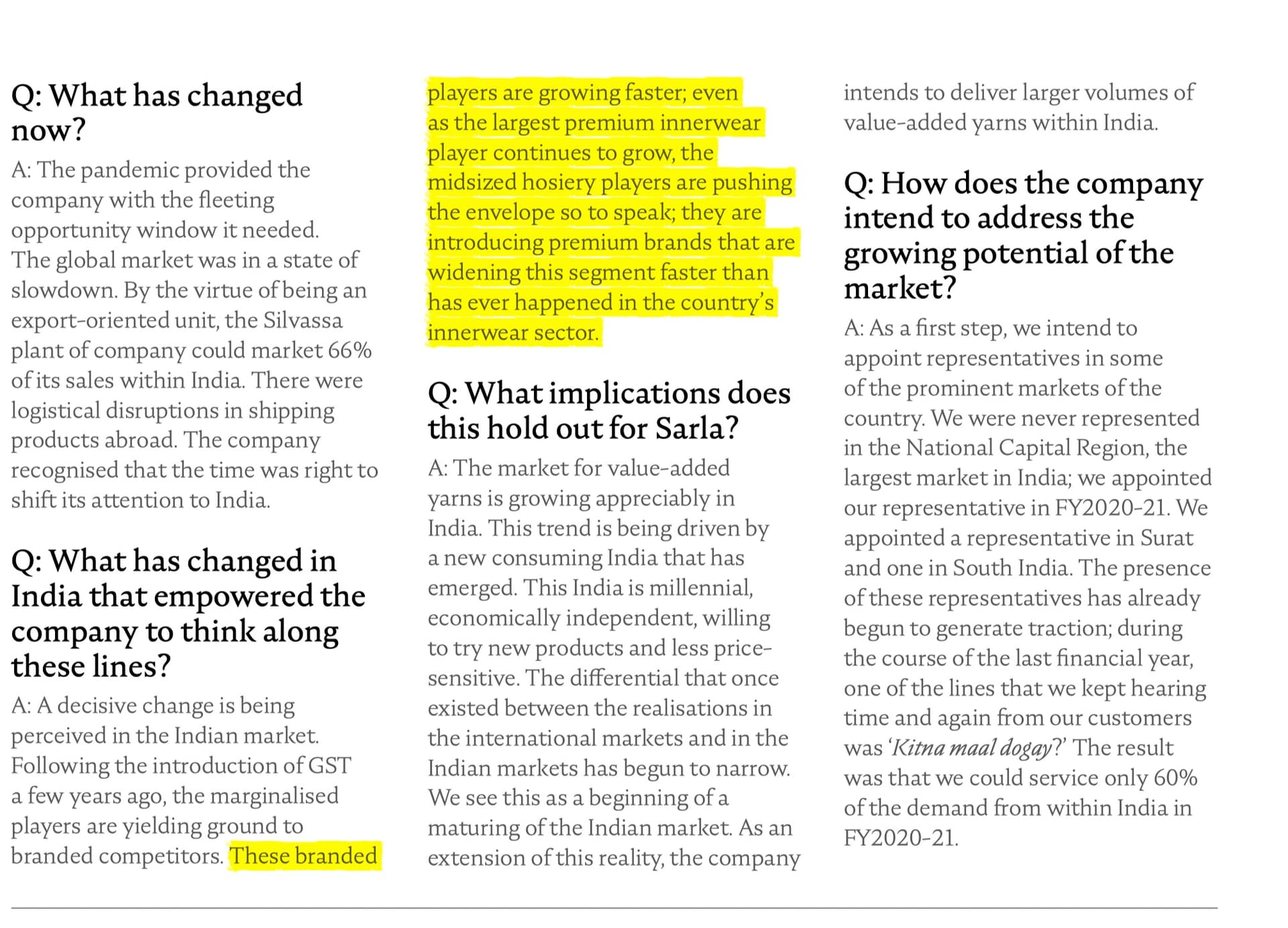

Virtually every company in India’s mid-segment hosiery space has been driven by marketing and distribution; Lux’s extension into retail was the first instance of a company selecting to engage directly with consumers

The Company launched 4 CozyWorld stores in FY 2020-21 and intends to scale this to 50 in FY 2021-22 (company-owned or franchised); these sales are targeted to account for 5-10% of domestic revenues in three years.

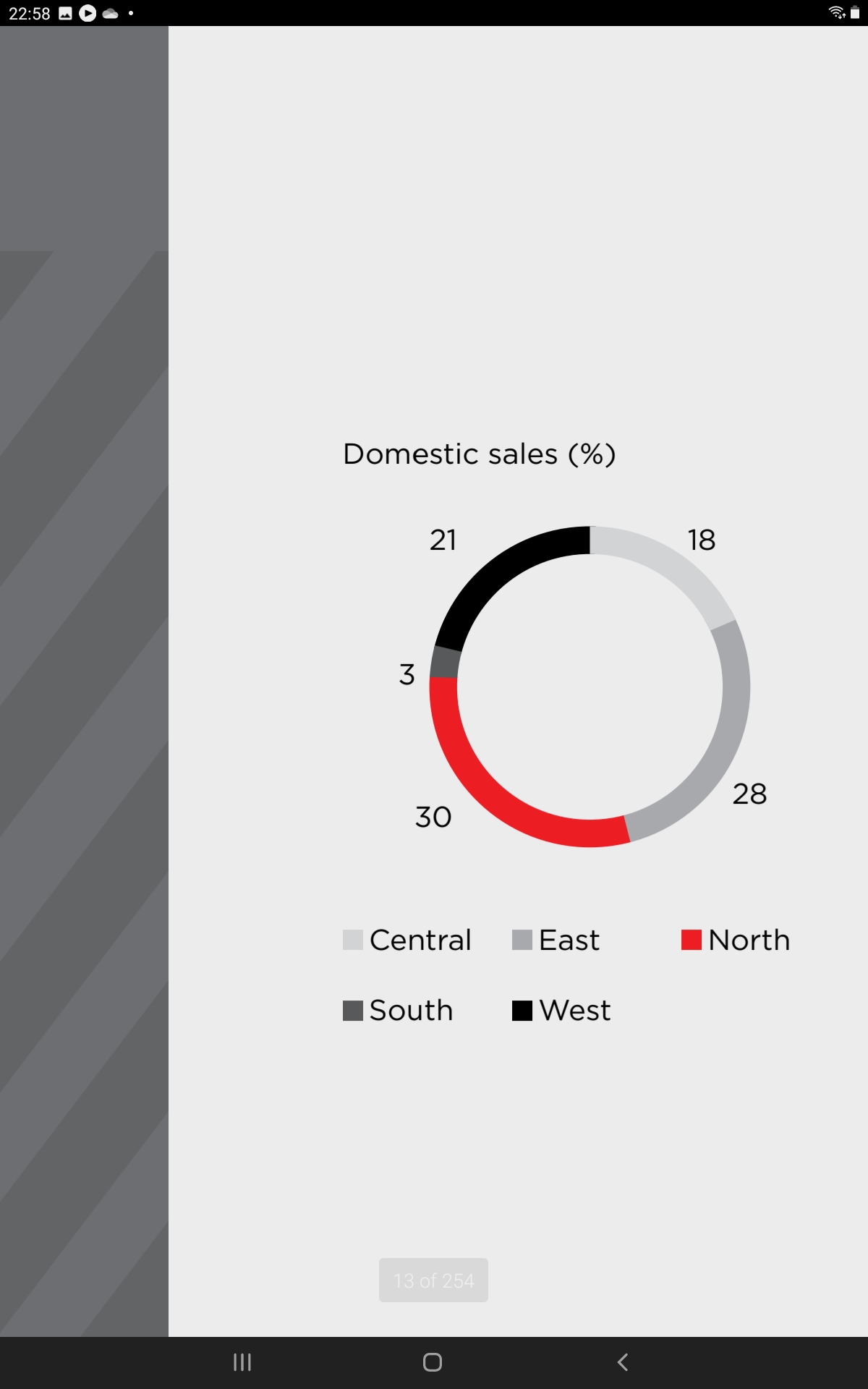

- South geo as next growth driver

The time has come for Lux to widen its footprint from a multiregional brand to a pan-Indian personality.

Lux’s penetration of South India will be increasingly visible from 2021-22, initiating the next growth

phase for the Company

- Online channel - numbers and brand perception benefit

The Company has its task cut out: sustain double-digit growth from online revenues and generate at least 2% of revenues from online sales across the foreseeable future.

- Premiumization push

The Company has its objective charted: extend beyond the functional to the fashionable; premium segment contributed 11.73% to the overall revenues in FY 2020-21.This will achieve the desired objective - each time the consumer thinks of enhancing his or her lifestyle, there is only one company the person will recall. Lux.

- Capitalising with speed on a structural market shift

-

WORKING CAPITAL EFFICIENCY- Receivables sustainable value-creation. management in a low liquidity market

-

New products launches during the pandemic

The result of going back to the drawing boards generated preemptive buying for a product that had been within the Company’s offerings for decades, the full impact of which is likely to be felt in 2021-22

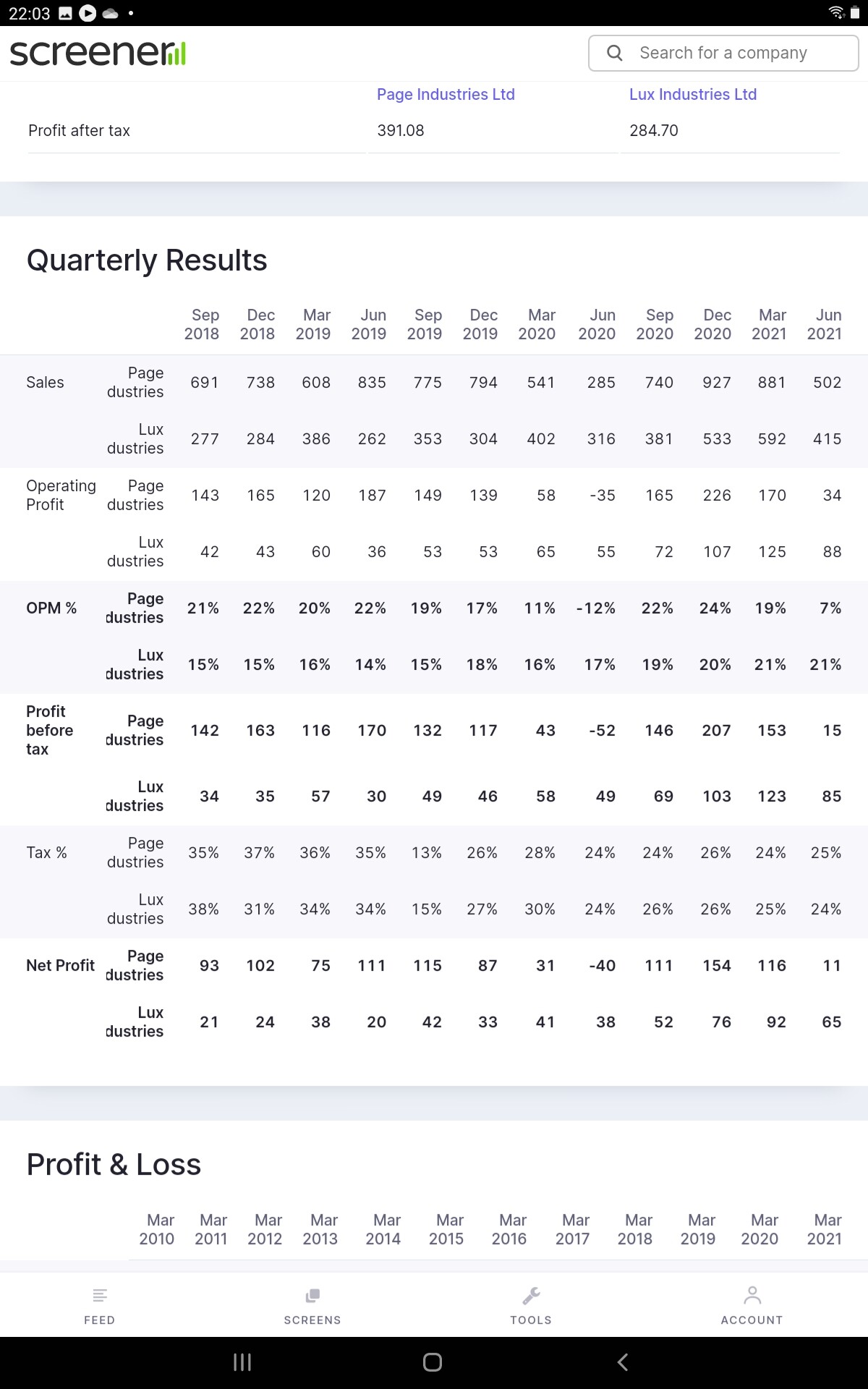

Valuations

Markets have rewarded the innerware segment players well in last 3 quarters, esp lux catching up with segment leader Page ind… some interesting facts in comparing both player

12 Qtr view

Lux wins hands down on consistency, biz resilience during corona impact. Sales growth and margins trajectory as well goes in favor of lux. Even if in all fairness to page we consider non Corona times such as Q3 19 >Q3 20 > Q 3 21, Lux has done better here as well

Long term view - 5 Yrs

If we compare last 5 years for both players together

Page 5 year avg PE ratio has been 69 and Lux has been at 33

Here are long term numbers for Lux

Here are long term numbers of Page

Given mkt is forward looking

Can lux deliver industry leading sales growth?

Industry itself will grow at 10% CAGR for innerware and allied categories - Lux has guided and delivered for mid to high teen growth and has delivered as well. AR also calls out some bold and interesting steps in this direction.

Can lux deliver industry leading margins?

Lux has guided for 20% + EBDITA , it can get further upside support from product mix tilt towards high op mgns premium segment, Page has their long term margins have been in similar range.

Industry dynamics well articulated by @zygo23554 , LUX INDUSTRIES - Can it Scale? - #69 by zygo23554

For FY 22 ( approximation)

Page optimist case ( normalized Q1 - removed corona impact) Page at market cap of 36K cr, 9X sales( at 4000 cr), 45X EBIDTA ( 20%)

For similar sales growth, similar margin profile, somewhat catching up working capital and balance sheet quality( lux may continue to lag here in forseeable future, point is reducing gap)

Lux has 12K cr mkt cap, is available at 4.5X sales( 2500 cr sales), 25X EBDITA ( 20%).

We have crazier valuations(10-15X sales) in pharma and chemicals etc

AR further strengthens the future outlook and conviction. Future is exciting and there is lot to unfold in coming times to help sustain further rerating as long as mgmt keeps delivering.

Invested - among top PF holdings