Major events that have played out in the meanwhile -

Stability in the Oil cartel returns though oil prices will continue to swing for a while. The prospect of a supply war at a time when demand is expected to collapse was a huge risk to the US bond & banking markets. Oil at very low levels for even 2-3 months could have been disastrous sending a bunch of companies in the US into serious solvency problems. Liquidity issues can be solved by central banks, solvency problems will call for bailouts which aren’t so easy to execute. Overall impact is positive for sentiment across markets

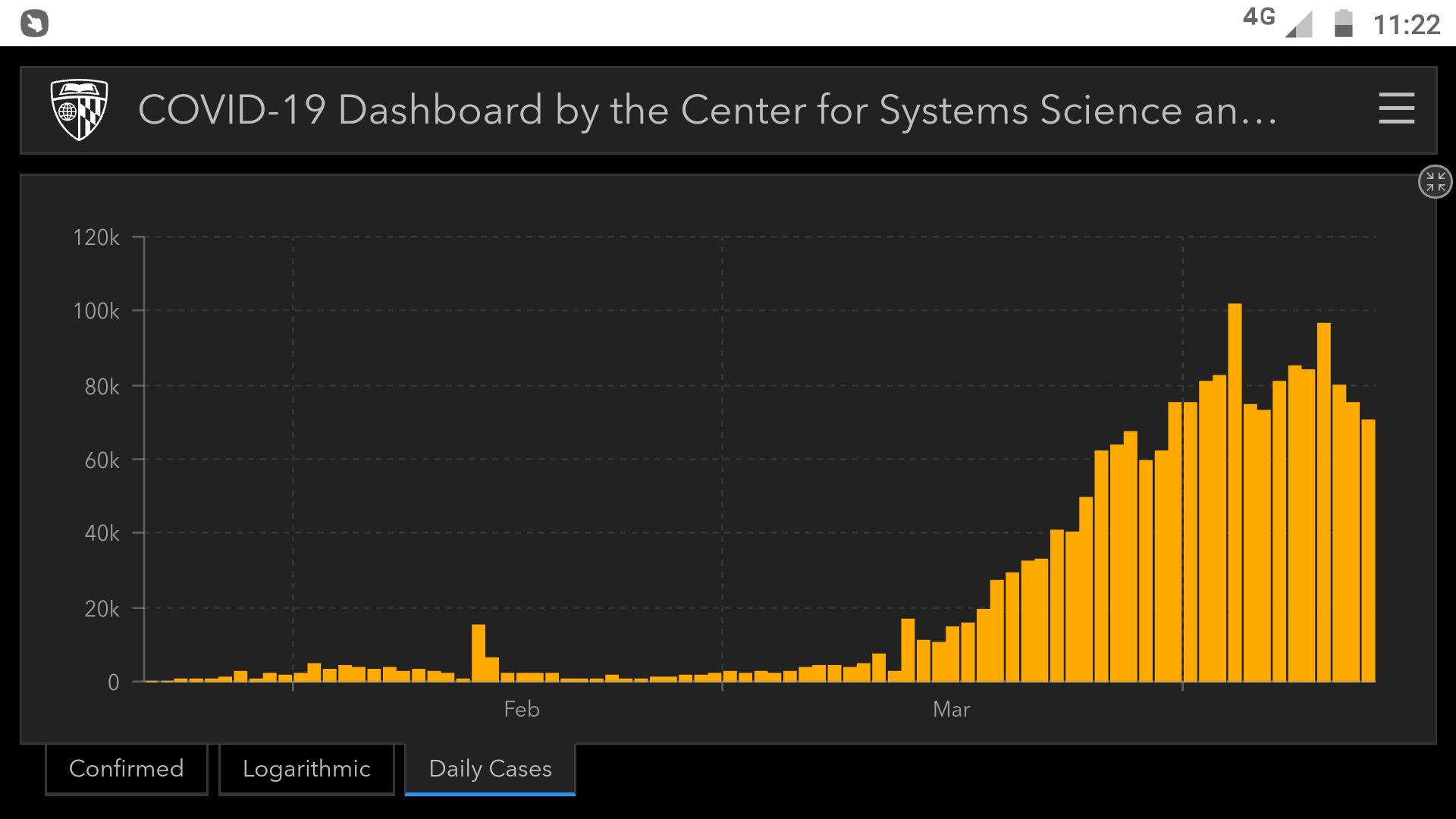

Increasing focus on whether the lock down is achieving the intended effect or not across countries. Going into lock down for a month is an easy decision for any Govt (they can always say “we tried” and give the perception of prudence), extending this into a 3-4 month lock down however is very difficult. Indian Govt came out today and said extension by another 20 days which was anyway expected, interesting thing was the reading between the lines that said they might consider opening up clusters that are behaving well/less affected well before the May 3 deadline.

Extending this thinking deeper - Govt does not want to be in a situation where the lock down is opened but supply chains continue to remain broken. The next 2 weeks will see a lot of action in the background where the Govt is tying in things using the FMCG distribution channel at a state level. Read more here - Government to set up 20 lakh 'Suraksha' retail shops to provide daily essentials - The Economic Times From my discussions with some FMCG folks over the past 3-4 days, inventory levels needs to be replenished which will anyway call for focused action. The Govt will likely have the revival mechanism working before the lock down is lifted to avoid chaos.

My overall takeaway continues to be that the lock down will end sooner than later, especially in India. A 3 month lock down can and will most likely be disastrous for India - won’t be surprised to see reports projecting zero to slightly negative GDP growth for FY21 after this 20 day extension. The economic prospects for a longer lock down will start looking really ugly. We just do not have the means to keep pumping in money as stimulus or for the central bank to go into QE mode like the developed nations.

Here on we will have some companies that start announcing Q4 results, on the conf calls all questions will be about Q1 rather than what happened in Q4. We will soon have some sense of the economic impact across industries and companies, all these days we were just shooting in the dark. The market is unlikely to get too worried about a Q1 washout, a Q2 washout is a different ball game altogether and can make the stock market outlook much worse that it is right now.

Markets across the world have also started reacting to liquidity measures and central bank announcements. We may have well seen the worst of the Wave 1 of the pandemic in terms of the impact on financial markets. VIX has cooled off more than 40% across equity markets, there are no jerky FX movements or wildly swinging bond yield movements too. How markets react to central bank action is a huge input to my framework, things are much more normal today than they were around March mid. Just see the gold chart in USD terms since the beginning of March till today.

Between 2010 and 2013, developed country markets were in a strange phase where bad economic news was being cheered (which meant QE and central bank support continues rather than be withdrawn). I would not be very surprised if the markets go into that mode here on, so we might see economic news that looks bad in a conventional sense but the markets just shrug it off knowing the central bank has it’s back.

The big risks to the current market situation are a combination of wave 2 of the pandemic in the countries first hit by the virus and extended lock downs as a result.

The market agility factor will come in handy where once these big risks are addressed/covered, one can actually go and increase the equity allocation % itself, rather than just continuing to buy the stocks that have already been identified. I would spend more time listening to asset allocators rather than to fellow stock pickers over the next few weeks/months.