Although on further inspection, the two critical ratios, P/E and RoE seem to be understated. As for P/Es, I beleive earnings should be higher. And as @Alphin correctly pointed out, I also agree with his analysis. Here’s a quick something I threw together in Excel:

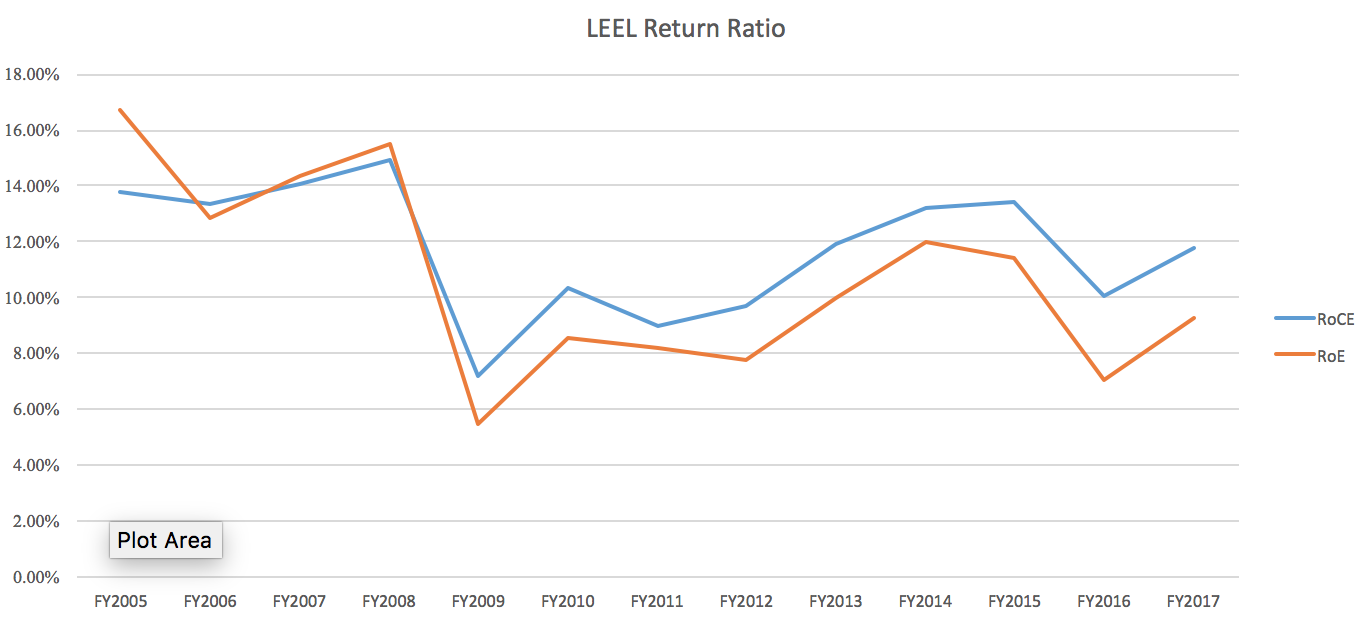

Look at the huge dip in RoE/pre-tax RoCE since the consumer company scaled up. I think we can see 14-15% RoE’s going forward.

Also, 75 crores PAT seems kind of on the low side. The way I think about it, the company made a 25% lower operating profit June '17 to June '16. At 271 cr FY’17, I’d say performa FY’18 earnings 203 cr, (75% of 271cr), 35 cr depreciation, 165cr PBT, and and 115cr PAT. Along with (hopefully) lower cost leverage and huge growth, I think PAT can compound at 14-18% CAGR, which should make this a solid investment. At the base case earnings, this is only 10x P/E for an earnings CAGR of 15%, which seems like still a great stock.

Given current momentum and spotlight due to Dixon Tech, I am a confident holder of LEEL.

Market cap of the company @246 r/s is around 1000 crs and sale from proceeds of Consumer durable business is around 1500 crs. If the company pays off the entire debt of around 1000 crs still they have 500 crs of cash on books. These are broad level calculations but net net at this market capitalisation of 1000crs I think its a bargain.

Tulsian mentions eps of 24-25. the last quarter results were pretty bad. How did raw material cost increase from 30% to 80% of sales. To get an EP Sof 24 the co. now requires eps of 13-14 in q4.

Still they pay pretty high interest per qtr. most of their EBIT gone into finance cost. They show profit after all cost Rs.946 crs and after tax it has been Rs.730 crs from the sell of consumer durable business. Do they have any cash on books as on 31 dec 2017?

I’m also confused by their high finance cost of 10 cr shown in the last two quarters. At a 10% interest rate, this is a loan of about 400 crores. I’m also pretty sure they don’t have any cash on books since they have no other income. So I am thinking they have spent some of the sale proceeds on capex.

However, post dividend payout of ~90 cr + DDT = 105 cr of dividend outgo, so from that + 300 cr transaction expenses + tax, I think total proceeds remaining with the company should be close to ~1150 crore (1550-400). This should be enough to pay off all of the company’s borrowings as of Mar’17, so I’m not sure why they still have a loan of 400 cr outstanding. My gut feel is that the company has been heavily reinvesting in the B2B side of the business and undergoing capex, although the small uptick in depreciation the last two quarters suggests that most of this capacity expansion has not yet taken place.

The stock has been falling, but I think the higher RM costs will easily get passed on to the brands due to high demand this season. I might start adding to my position if I can get LEEL for under 200/share or half of its book value. A back of the envelope calculation suggests that if LEEL is able to utilize its book value at its historical average of a 10-11% RoE, I am getting this company on a 5x forward multiple of the time this capacity is fully utilized. It doesn’t seem like a terrible bet given the industry size is growing at 15-20% a year.

Disc: Not invested, was invested earlier last year. Will look to buy if stock continues to fall with the small and midcap indices

This company does not have the pricing power, it’s mostly commodity type business. Any increase in raw materials, increase in cost of capital/ interest rates or due to competition it will not be able to pass on the hit to its clients and hence will take a blow on margins that’s my personal view. I exited when porinju was loading up

LEEL Electricals Ltd. is a leading system solutions provider of heating, ventilation and air conditioning (HVAC) for the railroad industry. With its extended capability to design, develop, manufacture and maintain highly engineered HVAC systems, Lloyd is uniquely positioned in the industry. original equipment manufacturer (OEM) to Indian Railways, supplying products for all rolling stock manufacturing units, as well as the first Indian Railways air conditioner company with in-house heat exchanger manufacturing facilities.

LEEL Electricals Ltd. can design, manufacture, install and maintain HVAC systems for all types of rolling stock including locomotives, suburban trains, inter-city trains and metro cars, and is a preferred supplier for these systems to Indian Railways.

Not even one of my assumptions from an year ago have worked out with this investment - time to move on and book loss. Investors have only themselves to blame at this point and i’m not sure of we can give the management another chance.

“Since the closing adjustments have been accounted for in the 4th quarter, this quarter reflects a loss of 283 Cr, under exceptional item, which represents the difference between audited figures for the full 12 months and unaudited figures for the 9 months ending dec 2017”??

After audit, they figured they sold the consumer business at a loss!!! or they overstated the profit from sale of cosumer biz in the earlier quarter??

Havells bought the brand, with the understanding that Leel will still be manufacturing the AC at a cost plus arrangement. Then why is the turnover nearly 1/3rd of the earlier years? Also, if the consumer durable biz is such a big cash burn, the reason they sold it to havells, why are they posting operating losses even after its sale?

Debt hasnt come down significantly. What the hell are they doing with the proceeds???

Any idea about the management? are they planning for some opportunity which we are not able to see?

Profit of Rs.662.98 Crores arising from the sale of Consumer Durable Business to

Havells India Ltd. on 8th May’ 17. The Company sold its Consumer Durable

Business as a going concern basis for an enterprise value of Rs.1550.00 crores on

cash free debt free basis which was inclusive of predetermined net working capital.

Of this, a total of Rs.1458.00 crores of the consideration have been received and

balance, as per terms of business transfer agreement (BTA) was to be released

upon finalization of the closing financials as at 8th May’17 , i.e. date of the transfer

of business, after appropriate adjustments. Since the business sold was as ongoing

concern basis, few of the final adjustment/reconciliation has been pending

finalization with the buyer and considering the impact thereof, the Company, has

arrived at the gain arising from the deal as per prudent accounting norms.

Accordingly, the gain has been computed considering the impact of assets and

liabilities transferred in terms of BTA, unserviceable left over inventory and

unrealizable receivables of the discontinued business, deal associated

cost/expenses, impact of financial obligations pertaining to 10 years of prior

operations arising under E-waste Management Rules, which has been made

mandatory with retrospective effect, post the BTA finalization. The total impact of

all the above factors comes to Rs.887 Crores.

So due to all these factors, Profit of 662.8 crores turns into loss of 283 crores?

Or

Profit is overstated by 283 crores and hence net profit from sale is 662 - 283 crores?

Separately, Havells had mentioned that the plants of Leel are quite dated and hence they did not buy the manufacturing plants. I’m thingking, Given the new energy norms, Leel was forced to upgrade their existing plants to meet industry standards - this they have also reiterated in their explanation dated 06.06.18

All in all, I guess this company will take some time to generate profits. Is Amber enterprises way ahead in the game compared to Leel?