Lloyd Electric and Engineering Limited announces acquisition of Noske-Kaeser’s Rail & Vehicle global business

5AA62DBF_9191_4A17_891A_77A092AA5DA3_181146.pdf (2.2 MB)

Somewhere in the intimation its mentioned that Noske-Kaeser had filed for insolvency and this sale was effected by the settlement team. So synergies will be the key. If Lloyd can revive the business, it will give a huge boost to the HVAC business and Lloyd might strive to become the single largest player in this segment in India. I tried to find the financials or atleast bankruptcy details for NK but couldn’t land up anywhere.

Also, cash is present in the books as on Mar '15. So additional borrowings shouldn’t be there.

Lloyd Electric & Engineering Ltd has informed BSE that the Consumer Durable Segment of the Company has achieved a milestone by selling 2,00,000 units of Air Conditioners under “LLOYD” Brand in 88 days of the current quarter.

Shares of the company have recovered strongly from feb lows of 190 to 260 odd rigjt now. This has been aided by early onslaught of summer leading to strong expectations from their ac division which will lead to higher matgins in the quarter and also a strong recovery in INR. In their q3 result concall, company has said that they might face further forex losses, like they had suffered in q3 results. They didn’t quatify the losses but said it will depend on USDINR, which they were expecting in range of 67-68.

USDINR has recovered significantly from there to end the FY16 @ 66.25.

Positively biased on the stock, but was unable to buy any quantity durinh the lows.

Disclosure: less than 3% of the portfolio.

Avdhesh, where is this extract from?

I’m sorry I couldn’t find that extract in the BSE filing. Nonetheless, my 2 cents:

Atleast in North India, the demand for air conditioners is steady during monsoons due to the humidity. Rather some people prefer to use desert cooler in summers but in rainy season, only air conditioners work. So I don’t agree with lack of volume argument principally.

Have been tracking this from past 6 months, the brand value in southern India,karnataka particularly is very high…tier 1 tier2 cities have seen great demand…and also was associated with IPL Bangalore franchise…

Indeed. Even the North is catching up. Their TV ads focus on simplified after sales service (they even have an app) and ACs are priced in the lower range along with Onida. Even the summer was extreme this year. But the Q4 results didn’t reflect that and that’s concerning.

Can anyone explain the recent upsurge in the price?

@RajeevJ are you still closely following this story?

Thanks

There was an announcement made by Lloyd some weeks back that it is looking for strategic alternatives to unlock shareholder value …there is a high possibility that the company may list its b2c division seperately…that could be a big trigger

There was an announce made by Lloyd some weeks back that it is looking for

strategic alternatives to unlock shareholder value …there is a high

possibility that the company may list its b2c division seperately…that

could be a big trigger

Hi, below is my brief analysis on what opportunity (imho)could be there in this company.

There was an exceptional item of 45.8Cr (write-off of insurance claim) because of this the standalone PAT declined from 81.64Cr in FY’15 to 56.06Cr in FY’16. Now, assuming that exceptional events don’t happen often and if we add back this exceptional item, the PAT could have been 101.86Cr i.e., a good 24% jump. Dividing this (assumed) profit by 3.62Cr shares outstanding, the EPS comes to 28 and the stock is trading at 9/9.5 times trailing earnings.

[ Screener shows the PE as 10.27, but I do not know how that is calculated, as the basic EPS as per Annual Report FY16 is 15.48, so trailing PE at present is 16. https://www.screener.in/company/LLOYDELENG/ ]

The company operates in three segments namely,

(1) Consumer durables,

(2) OEM & Packaged Air Conditioning, and

(3) Heat Exchangers and Components.

The Consumer durables division contributes to 59% of standalone sales of the company. This division can be comparable with something like Voltas (trading at 31 times earnings) or Bajaj Electricals (trading 27 times). Pls note that I am not comparing it with the likes of Blue Star (trading at 44 times), Whirlpool (trading at 47 times) or Hitachi (trading at 56 times) which are more established market players.

The remaining two divisions are largely B2B, catering to Industries or other AC/Refrigeration companies (including Indian Railways and Metro Rail).

Now let’s assume the company achieves the same Net Profit of 100Cr for FY17. The Consumer durables contribute 60% i.e. 60Cr, and remaining two divisions contribute the remaining 40Cr. We can apply a conservative PE of 20 times to the Consumer durables business and 10 times to the other two divisions combined.

Consumer Durables ~ NP 60Cr ~ Mkt Cap 1200Cr

Other Two divisions ~ NP 40Cr ~ Mkt Cap 400Cr

Total Mkt Cap ~ 1600Cr

Which is significantly higher than the present Mkt Cap of 937Cr.

Strengths:

The company is vertically integrated across the Heating, Ventilation & Air Conditioning (HVAC) value chain from manufacturing the heat exchanger/coils, components, air conditioners to selling to OEMs as well as under “Lloyd” Brand, thereby providing an end to end solution.

The company has entered in the consumer durables market in 2011 and already have 13% mkt share in RAC (Room Air Conditioner).

From where the growth will come from :

(i) Rising disposal incomes will mean increase in spending on durables

(ii) Rural Markets has very low penetration of consumer durables and huge scope owing to growing rural income and increasing rural electrification

(iii) Returning of economic growth will lead to increased industrial activity – augurs well for the HVAC&R (Heating, Ventilation, Air Conditioning & Refrigeration – the B2B business of Lloyd)

Concerns :

(i) It has got a lot of debt (Long tem 79Cr & Short Tem 738Cr) and paying over 100Cr as finance cost.

(ii) Trade receivables are 600Cr, which is one forth of Sales (standalone)

(iii) Net cash generated from operations is just 13Cr against Net Profit of 56Cr (I don’t know what % this should be or whether this is a red flag

P.S.

- I have not commented on consolidated numbers. The overseas subsidiaries appear to be a drag as of now and I am yet to study the same.

- Kindly let me know your comments on the above analysis

Disclosure : Have initiated a tracking position. This is not a buy/sell recommendation. Pls do your own due diligence before taking any decision.

1 Like

HDFC Securities has come out with a research report on Lloyd Electric recently.

Lloyd Electric HDFC Sec.pdf (269.3 KB)

2 Likes

Company is looking to demerge its cosumer durables business. Nothing officially confirmed by the company yet.

Welcome move by RBI

Has anyone heard anything about the demerger. Some people on moneycontrol mmb were talking of Havells buying the stake (which imo would be disappointing). There would be strategic advantage if the Japs get involved.

I am invested.

Anil Gupta, Havells MD denied this during their recent post results call saying he wouldn’t like to comment on market speculation. So it isn’t actually a denial.

Havells had evaluated getting into ACs many years back (as mentioned by Anil Gupta in his book) but decided not to as it wasn’t a good fit given that ACs is a low margin, high working capital, MNCs dominated business which also requires a separate channel quite different from their existing channel. And Havells being very channel focused and channel friendly org would find it difficult to manage expectations of their existing channel when their dependency on the newly acquired AC channel (if it happens) would be very high. To my mind, it would create an enormous conflict between the two channels which is best avoided.

The only thing which has changed between their thinking then and now is that they have a lot more money now. I hope Anil doesn’t fall prey to “have money, will buy” tendency.

Disclosure: Invested in Havells, not Lloyd.

Q2 Results are out .

Lloyd has come out with excellent numbers .

Attached the Result

80BFED13_EF9C_4840_B820_10E1AB36EACF_184427.pdf (1.8 MB)

At Consolidated level EPS has jumped from 1.27 to 3.08

From this we can assume that the subsidiaries has stopped bleeding . (Though far from posting profit)

On the standalone basis the numbers are good.

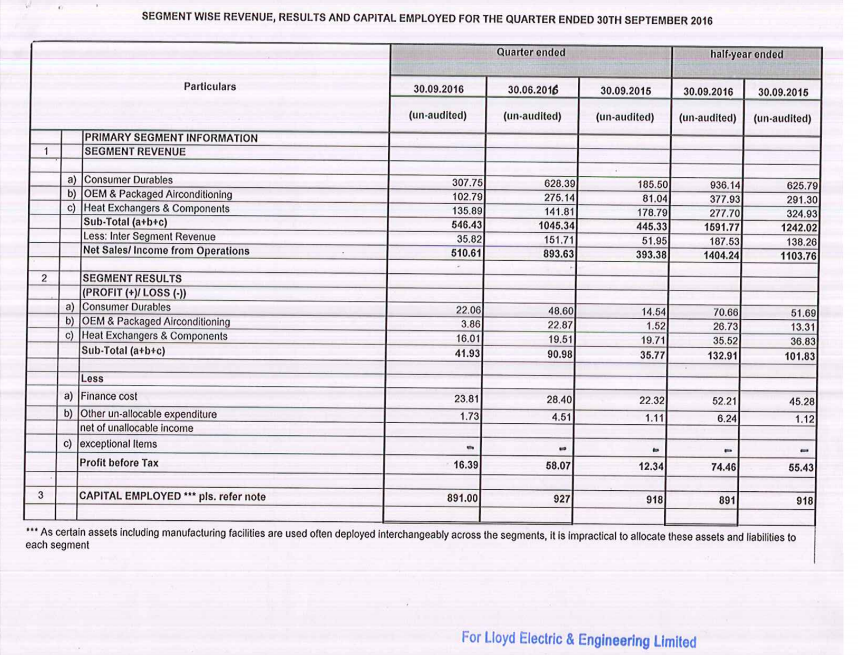

- Consumer Durables and OEMs section had shown good growth .

- Margins in OEM space has increased

- Consumer Durables margins has decreased (Overall Segment result is increased 50 % powered by ~70 % Revenue growth)

- Heat Exchange segment revenue dropped . Probably because now LLoyd competes directly to its customers in this segment . So customer might have changed the supplier (Just an assumption)

- Short term borrowing at standalone has come down from 737 Cr (Mar-16) to 578 Crs (This reduction might have some contribution from Warrant conversion)

- Long term borrowing reduced to 66 Cr from 78

Overall the company is really performing good .

One thing to watch out in next few quarters is Forex losses . In the past Lloyd has reported Forex losses when USD went up steeply .I hope it does not repeat this time .

1 Like