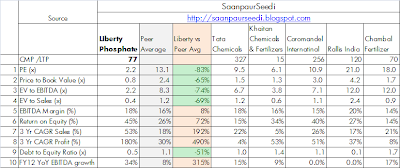

Excerpt from HDFC Securities Report

Concerns

â Approximately 50% of rock phosphate requirement for production of SSP is imported. Global rock phosphate prices increased by~27% in FY12 from $160.4/MT to Rs. 204.87/MT. While raw material prices have stabilized a little now, and LPL was able to passon most raw material price hikes forward, fluctuating prices remain a concern. Raw material expense for LPL increasedsignificantly in FY12 reflecting the high global raw material prices.

â Import of rock phosphate exposes LPL to forex risk. The company reported a Rs. 1.8 cr forex profit in Q4FY12 due to its hedgingstrategies. However, in FY12, forex loss was Rs. 3.7 cr. LPL has negligible earnings in forex and high expenses in forex resultingin a large exposure to global currencies (largely the USD).

â Agricultural productivity could be a concern as a poor crop could leave little income in the hands of the farmer who in turn wouldnot want to buy expensive fertilizers.

â Urea prices are still cheaper than those of SSP. While the government has been discussing the feasibility of applying the NBS tourea as well, it has been unable to make any substantial move in the direction. Decontrolling urea prices will be very beneficial toSSP manufacturers, as Urea prices will increase, reducing its cost attractiveness.

â The fertilizer industry is always prone to government intervention since farmers are the end users. Any unfavorable interventioncould wipe out profits.

â With a lot of new large players having plans to set up SSP units and existing companies in expansion mode, there could be anoversupply situation in the industry over the next few years leading to a drop in profitability over the medium term.

Earnings Scenarios

Assuming a ~30% increase in revenue in FY13 from increased utilization and added capacities, we believe the net margins can varybetween 6.5% (in a worst case scenario due to increased raw material prices, low subsidy and inability to forward to cost to thecustomer) and 10.5% (in a best case scenario due to low raw material prices and high finished goods prices â and anyway lower than10.6% earned in FY12). A brief scenario analysis is shown below:

Scenario Worst Average Best

PAT 39.9 52.2 64.5

NPM (%) 6.5 8.5 10.5

EPS 27.7 36.2 44.7

P/E 2.8 2.2 1.8

It is evident from the scenario analysis that even in the worst-case scenario LPL is still trading below 3x FY13 (E) earnings. Downwardvolatility in margins and earnings could have a negative psychological impact on investors however, from a price perspective LPL istrading at a very low valuation. And if dividend payout is raised sharply (normally decided in early August every year) then reratingprocess could gather momentum.