Came across the article in a news daily -

To what extent the chinese competition likely to impact the story for Laurus?

Came across the article in a news daily -

To what extent the chinese competition likely to impact the story for Laurus?

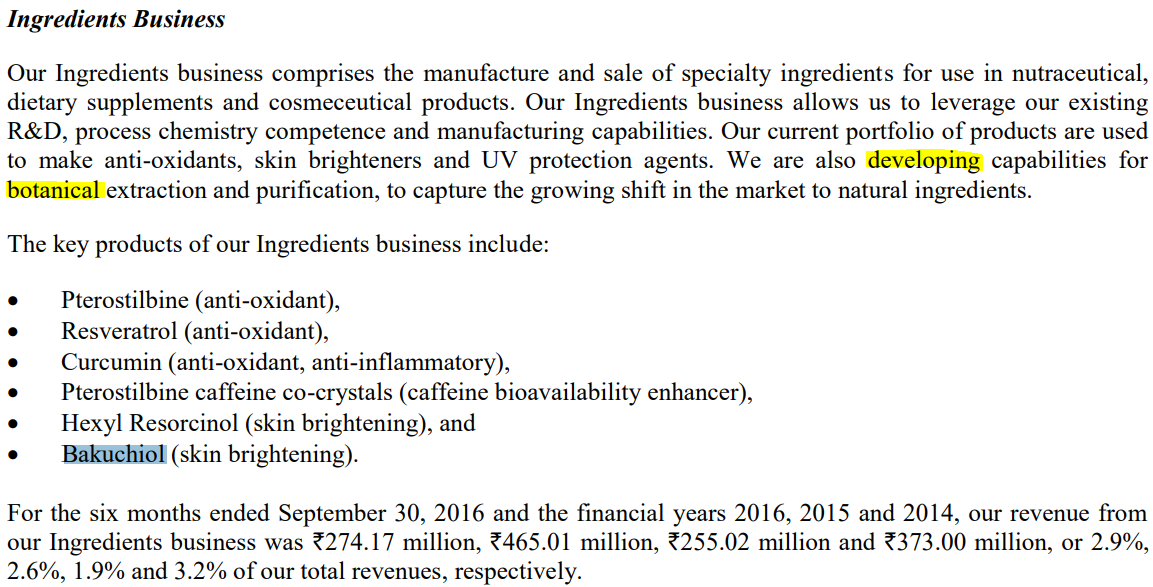

From IPO prospectus:

http://www.investmentbank.kotak.com/downloads/lauruslabslimited-prospectus.pdf

Anyone has idea on whether Laurus supply Revlimid API’s to Natco ?

Just in: USFDA approves Kalydeco (#Ivacaftor) as first & only CFTR modulator to treat eligible infants with cystic fibrosis (CF) as early as four months of age

#lauruslabs

Got this info from a Twitter user… does anyone has the info of the market size and key producers of the drug and laurus partnerships with them??

According to the Cystic Fibrosis Foundation Patient Registry, in the United States:

Its produced by Vertex Pharmaceuticals. Laurus Labs holds certain patent related to this but not sure how it exactly is Laurus involved. And how it benefits.

And Vertex is doing very good there. I guess this might go extremely good for Laurus as well… Check attachment.

Scan 28-Sep-2020.pdf (41.2 KB)

Laurus labs merged it’s two subsidiaries in the usa. Laurus synthesis and laurus generics

I was trying to understand the IP risk with laurus venturing into Formulations. The following sentence is fully written from Laurus point of view. Almost appears to convey ‘No Problem!’. Can those in the industry give their viewpoint.

Disclosure - invested at ~ 1100 levels

This assessment of the situation might have been relevant a decade ago, but the industry has changed: stakeholders do not recognize the same boundaries as before, where companies used to stick to their areas of expertise. To give you a concrete example, the number of legal actions between two originators today are significant when compared to the number of trials between originators and generics companies. In the same way, generics companies are trying the climb up the value chain, while originators have been expanding their business model to the generics field. There is not a single company operating at the global scale that is not diversifying its business model and venturing into new verticals to better benefit from emerging market trends. I believe that our API customers understand these dynamics, as they follow the same approach when it comes to the diversification of their own revenue stream.

At the end of the day, if Laurus is able to offer a better API at a lower price and with a greater capacity than a given competitor exclusively focus on APIs, I have no doubts that our customers will remain loyal to our offering – even if we eventually become one of their competitors on the formulation side.

Everyone is saying laurus labs is going in divis labs way and its next divis but as I can see its adopting dr Reddy labs strategy by diversifying into formulations and other verticals. The divis is solely a pure play api company.

https://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=540222&qtrid=107.00

Laurus labs put up a BSE notification today. Pledged shares down to just 16 percent. Please delete if already mentioned earlier. Just noticed it today on the website

Has ambit capital existed from lauruslabs?? I can’t find their name in the September share holding data. Could someone throw some light on it??earlier they used to have 11 %.

yes, its correct

a small note on changes during Q2 are available here

Laurus labs made a proposal to invest 300 crores in HYDERABAD’s genome vally.

Looks like this FDF capex is in addition to what they announced in 1Q21 earnings call.

“Laurus Labs has also announced the setting up of a formulation facility. The company plans to invest ₹300 crore in two phases of ₹150 crore each. Laurus Labs has its R&D facility in IKP Knowledge Park, Hyderabad and also operates six manufacturing facilities in Visakhapatnam, Andhra Pradesh.”

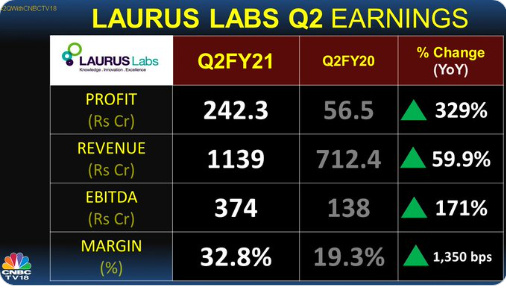

Revenue growth of 60% and PAT growth of 325% in Q2 FY21

Q2 FY21 Revenues up 60%

Q2 FY21 EBITDA at ₹ 378 crs up 172%, Margins at 33%

Q2 FY21 PAT at ₹ 242 crs, margins at 21%

Going through the investor presentation

What does “in-licensed” in the following mean in page 5 under Generic FDF?

“Commenced marketing of in-licensed products in the USA to

leverage front-end capabilities”

I read this in press release

“Commenced marketing of products of other manufactures by leveraging our front end”

Is this like retail? Selling products of other companies?? ![]()

Edit: This last edit should complete the story and answer my own questions

Found this in Q42020. It would still be nice if someone confirmed this is part and parcel of Contract manufacturing biz.

Q2 concall notes

Bullish on their prospects based on excellent order book

Increased their capex plans from 700cr. to 1200cr. over the next 2 years.

New API, FDF and Custom Synthesis plants

30% increase in total API capacity.

80% increase in FDF.

New plant and R&D Facility to focus on custom synthesis which has been growing by 30%. (in Q1 launched a new subsidiary to increase focus on synthesis).

All the green field expansion have turned Cash positive in FY20 with near maximum utilization

Plan to spend 1400-1500 crs on brown field and green field capex with 40% for APIs, 40% for formulations and 20% for CRAMS…

EU - CDMO for non-ARV working very well

4% revenue spent on R&D in H1 FY21

Expect life time highest ARV sales in current fy

Healthy CDMO order book

Synthesis - YoY 36% growth / R&D capex of 60cr - will start contributing to topline in next FY

Customers are not stocking APIs due to covid next wave

Robust growth in Other API segment to continue on the back of higher order book visibility from key therapeutic segments like CVS, Anti Diabetic and PPIs

Formulations growth was led by higher LMIC Market volumes and increased

volumes from North America and EU

Capex increase of 70-80% in last 2-3 quarters is mainly due to increasing order book visibility

Expected revenue contribution change in next 2-3 years from current 60% ARV / 40% non-ARV to 50:50

30% capacity addition in APIs in next 18 months

80% capacity addition in formulation side in next 18 months

nothing new in Q2 - its just normal business as we have not added any new product or new client… so its just normal business & increased demand from current products / clients… indicates that it was not one time performance

Majority of capex will be operational by June’22 (40% API, 40% formulations, 20% synthesis)

After capex (around FY24) base will increase but % contribution will remain similar

ROCE after capex should come down but still it will be industry best (H1 ROCE was 37%)

Process innovation - currently we have 25% market share in 7 APIs / we want to have similar leadership in 15 APIs

Majority of above 15 APIs will have backend integration from formulations but not all

HIV medication :single month dispensing has moved to multi month dispensing (earlier patients were getting 30 day medicine are getting 90 day medicine now in one go to reduce their visits in these tough covid times)

Please consume above data at your risk, I may have overheard and have manipulated some inputs based on owner bias