Lot of unbranded players and imported products are also giving tough competition.

In the current quarter (Jan-2025 to date) promoters bought 0.16%.

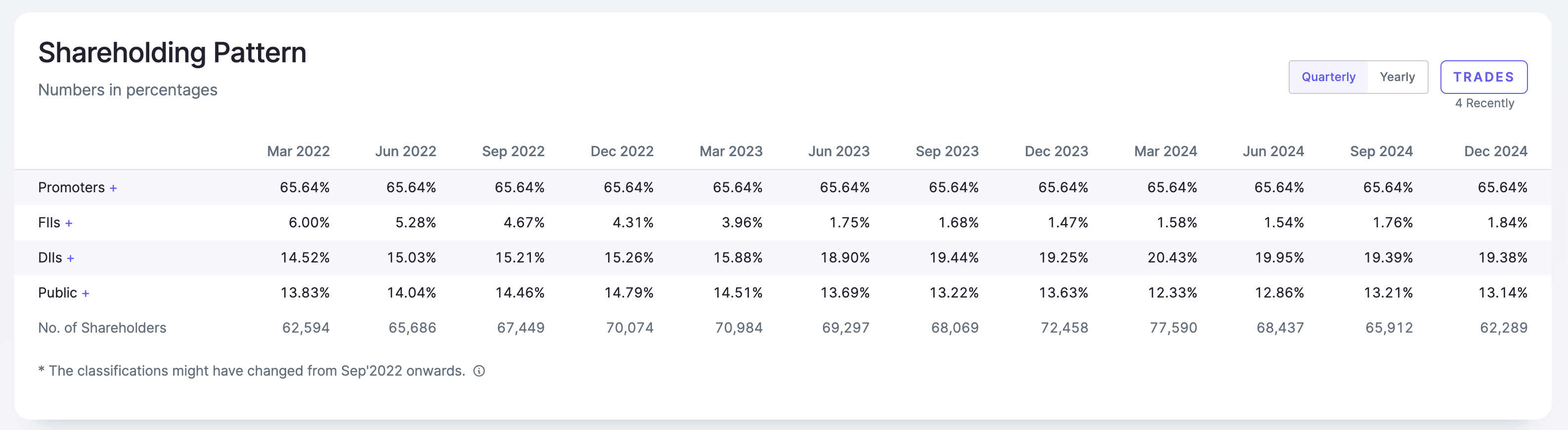

At the end of Dec-2024: 65.64%

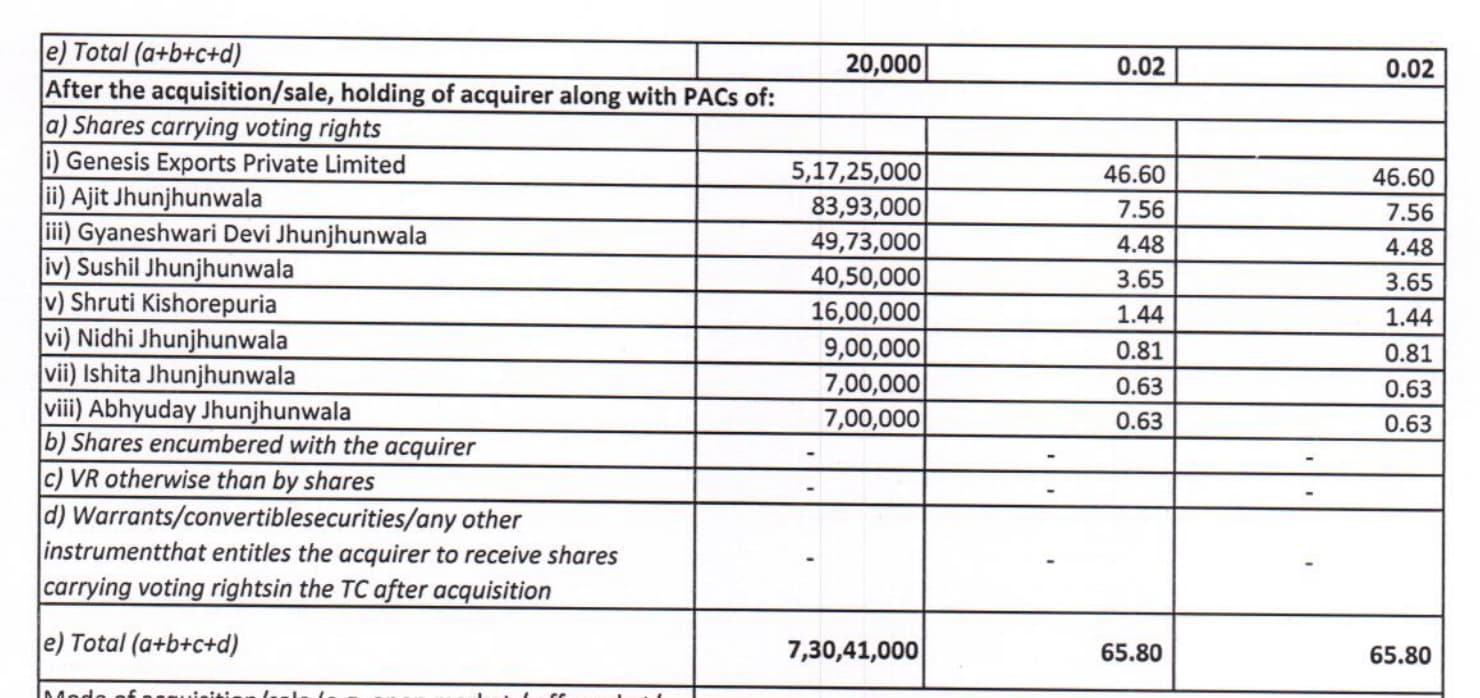

Today’s filing: 65.80% - their highest in the recent years

No. of shareholders also reduced, stock is at reasonable valuation.

Disc: Invested, added more in last 30days.

2 Likes

How is Cello vs La Opla now? Can anyone tell how’s they performing on ground? Is Cello taking market share?

Retailers currently hold excess inventory, and with low brand loyalty, competition remains intense. Cello is gaining market share by selling at lower margins than La Opala, but as investors, we can avoid this space as there is excess supply here with weak demand.

1 Like

Is the current inventory surplus expected to be short-lived? Won’t upcoming income tax reductions and possible GST cuts increase consumer disposable income and, consequently, demand, thereby resolving the inventory issue?

2 Likes

can we quantify the market share data for La Opala based on all the industry data available? are they really losing market share ?

1 Like

What are the problems facing La Opala. why is it not able to increase revenues? Is the consumer interest on their products (as a sector not specific to LaOpala) fading? Is it the main cause? Any opinions pls

I believe theres too much competition and La Opala just hasn’t focussed on their distribution like they used to.

Everyone out there is offering the same products at similar or lower price points and brand just isn’t a good enough differentiator anymore.

2 Likes

I understand your logic but it is incorrect to say that the promoters are using shareholder funds to increase stake - since the number of shares La Opala owns of Genesis exports has been stuck at 75330 since 2012. So shares haven’t changed - hence there is no additional money that goes to Genesis as shareholder money. However they do receive a chunk of dividends, and those dividends may be reinvested, but that’s not a problem

Could you pls share why the cross-holding is detrimental to minority shareholders? Although it’s explicitly mentioned that there is no holding company - genesis exports acts as a holding company at the end of the day.

And is it a negative trait to be investing into bond funds? As long as there are not credit risk funds in the portfolio - treasury money is fine in bond funds since most of it wouldn’t be used in one financial year. Franklin Templeton was a serious problem - but Im not considering that poor corporate governance because they did invest into short term debt funds.

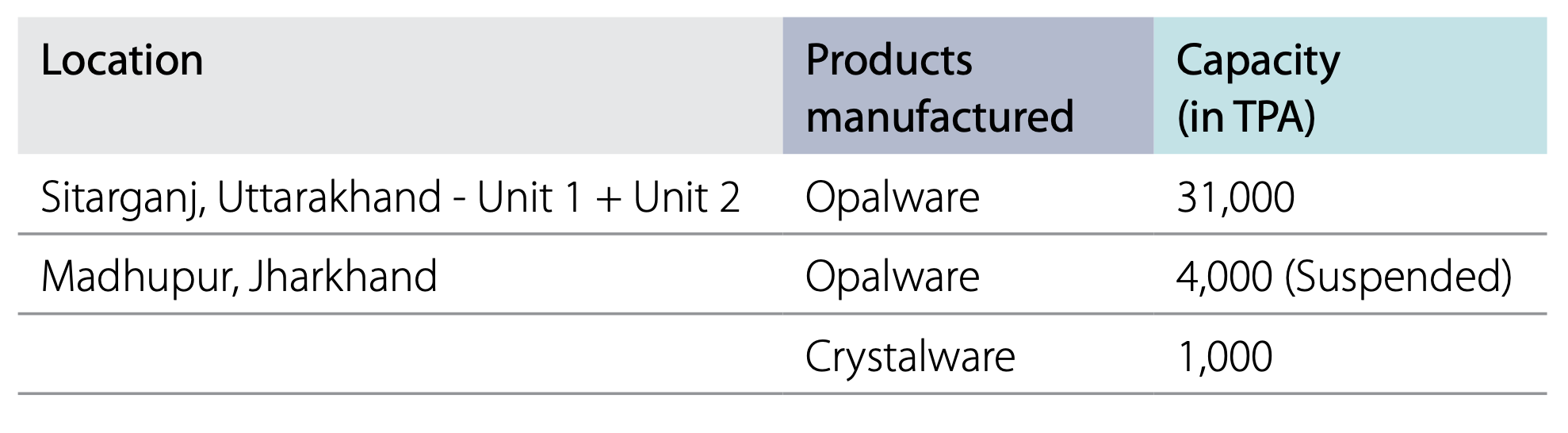

Regarding capacity - they had Greenfield expansion of 12,000 MT in 2022, and then they downsized their Madhupur facility because it was pretty old (since 1987). That money should be further utilised.

But current capacity is as follows:

I have some information (not concrete) regarding their dealer network - it had fallen in between 2023/2024, and they were focusing on a dealer rationalisation strategy which is largely done now hence the recovery in sales numbers albeit not to previous highs.

Disc: not invested