Middle-east led by Saudi is in hurry to transition their economies away from fossil-fuel export before world completes energy-transition. Earlier project wins in middle-east were mostly in traditional oil and gas sector but new ones are from diverse sectors which are part of this transition.

India’s longest sea bridge connecting the Indian city of Mumbai with the satellite city of Navi Mumbai named Shri Atal Bihari Vajpayee Trans Harbour Link or Atal Setu, was inaugurated on the 12th of January 2024. Our company was one of the major EPC contractors involved in this prestigious project.

On January 22nd, 2024, the Hon’ble Prime Minister of India led the consecration ceremony of the Sri Ram Janmabhoomi Mandir in Ayodhya. We are pleased to inform you that this temple is also being constructed by Larsen & Toubro.

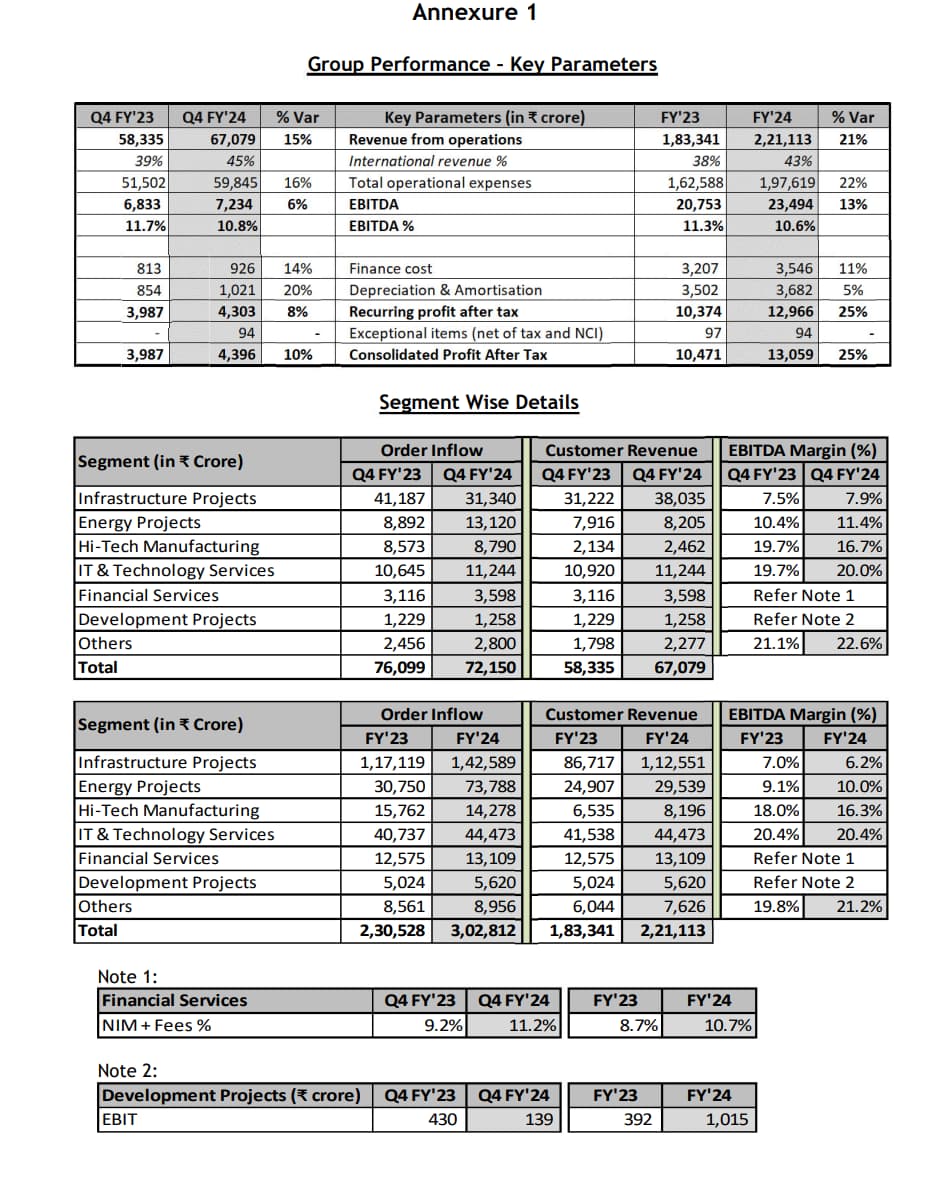

Our Hydrocarbon business has performed exceptionally well during the year. The nine-month order inflow for this business at Rs.582 billion is a record high. Consequently, the order book for this business has expanded to Rs.1.07 trillion as of December '23

Our Financial Services business has achieved the highest ever quarterly retail disbursements of Rs.149 billion and the retail portfolio today is at 91% of the overall book, which stands at Rs.818 billion

We manufactured the first Electrolyzer of 1 MW in the Hazira factory on December 13th, 2023

On the Green Energy side, L&T Electrolysers Limited has emerged as a successful bidder with an allotted capacity of 63 MW under the tranche-I of the PLI scheme for electrolyser manufacturing, launched by the Ministry of New and Renewable Energy

The Data Center at Panvel, a pilot project by L&T, has gone live with a capacity of 1.4 MW in the Mumbai region. Furthermore, there is an upcoming data center closer to commissioning of almost 12 MW in Chennai, expected to be completed in Q4 FY’24.

We incorporated a wholly-owned subsidiary, L&T Semiconductor Technologies Limited on November 29, 2023. Over time, this company will be engaged in the business of fabless semiconductor chip design and product ownership

Our order book is at Rs.4.7 trillion as of December '23, which is up by 22% when compared to December '22.

As our Projects and Manufacturing business is largely India-centric, 61% of our order book is domestic and 39% international. Of the international order book of Rs.1.84 trillion, around 92% is from the Middle East and 2% from Africa, and the remaining 6% constitute from various countries, including Southeast Asia

Receipt of multiple orders contributed to the order inflow in the Defense business, whereas we witnessed order deferrals in the Heavy Engineering segment during the quarter. Our order prospects pipeline for this segment is Rs.163 billion.

Article claims that L&T Defense would be third largest Defense company after HAL and BEL if it was listed independently. Has revenue of 3.5 thousand crore and order book of more than 12 thousand crores.

I had mentioned this earlier, this is getting confirmed by management

Subramanian Sarma, Whole-time Director & Sr EVP (Energy), L&T, said the company’s bidding pipeline in West Asia remains very strong and there are many prospects that remain very active.

“Also, several opportunities are arising from Energy transition-related investments, such as Blue Ammonia, Desulphurisation, gas production, gas transportation infrastructure, and petrochemical projects,”

Read more at:

L&T also feels that its EPC business around Green Hydrogen will be bigger that electrolyser

L&T signs 7000 crore worth of contract. Major breakthrough in a complex defense system. Breakthrough in airforce. Till now their wins have been with Army and Navy. High end radar was monopoly of BEL earlier.

Edit Media is reporting that they got complete 13k+ contract. May be there is another press release for the same or contract is awaiting formal signup.

This has possibility of being one of the biggest segments a decade down the line. Chip Design is highly profitable if you get the product right. eg. ARM / Qualcomm, Infineon and Renesas(though it does other aspects of chip ecosystem also).

Disclosure: Invested in family accounts since 2021.

So , L&T is no longer a mere infra company. it is a play on a mix of many sectors with tailwinds going forward.

Infra +Defence + Green hydrogen/ Electrolyser+ Chip making…And there are listed subsidiaries in

IT too.

now execution is the key and should be reflected in balance sheet going forward. There could be some value unlocking for share holders in the long run too.

Discl : Invested since Covid days of 2020-21 from lower level in L&T , Reliance. Both stocks tried my patience. i have never booked profit. Now only it is paying up.

I see them demerging their Basic Construction business, roads tunnels and stuff in future once all the new plays are stabilized and in growth mode.

Will rerate it completely. Professional run business playing in all segments of new econ as you said. Its one of the hold till market allows type of stock.

Anyway, the tech and finance is already 30% of consolidated profits. Once they cross 50% in next few years it will look a whole new company.

Only Concerns are on the Hyderabad Metro and GCC slowdown in Oil and Gas contracts.

I have been trying to ascribe some ballpark value to L&T Defence business after reading above article.

This interview states that L&T will have close to 26000 cr order book by next year (13k crore they just won last week).

Now when I see smaller companies like MTAR, they trade at 5x order book so even we give L&T a 4x order book, we are looking at 1 lakh crore and 1.25 lakh crore if we value at 5x order book.

When I started this thread whole company was valued at 1.25 lakh crore

So, defence is 20-25% of total valuation of today. That is pretty large. I am not sure if market is still factoring in that. Looks like that is the disconnect between conservative domestic brokerages which value L&T close to 3200-3400 and some of the global/domestic brokerages which are valuing it at 4200-4400.

I believe it to be a good hypothesis. They have under utilised defence capacity from guns to ship making. But defence deals have political dimensions and long gestation to signing. even signing a deal doesn’t mean anything, payment for delivery matters. If you look at HAL, BEL, all of them sign deals 1000s of crores, doesn’t immediately reflect in balance sheet revenues. Probably why, analysts focus on engineering services for roads, power, utilities, buildings, Metros etc as they have a timeline

I’m invested in L&T, so my biases are there and certainly not a recco to buy or sell.

Subdued performance for many verticals including hi-tech manufacturing, IT services. While hi-tech and defence may pick up in future, not overall convinced with execution in these areas.

Decent performance on Infra and Energy divisions.

Exceptional profit in development projects due to sale of commercial land in Hyderabad Metro. Otherwise, dull results there

Finance vertical is picking up but I am not convinced with retail strategy here.

While Energy vertical has done well and shown 100% growth in order intake because of GCC orders, same may be subdued this coming year with slowdown in GCC orders. Saudi has cancelled NEOM projects, reduced spending on Oil & Gas. This is crucial bit to check.