Another feather in L&T’s cap. Truly Building India

2 Likes

LT has crossed and closed above it’s previous all time high (2019) today… It’s subsidiary holding in Mindtree, LTTS is benefiting as they risen too back of good results. Given the increase in market capitalisation now, what would be appropriate price per share ? Also to note LT’s PE ratio for the size of its business it’s really low at under 20.

The only con being it has piled up higher borrowings in last one year

1 Like

The answer to your question lies in this article and the CNBC TV video- analysis as per Axis/ HDFC securities. The Fair value stock price of L&T has been assessed. You can watch the video clips.

1 Like

Any idea why Larsen and toubro is trading at such a low PE of 15 when it’s last 5 year median PE was 25. Can somone knowledgeable throw some light on this. Thanks

Capital goods & Infrastructure as a sector was in a down cycle and the fact that in spite of declaration of huge Infra spends by Govt, very little was spent in reality & Covid 19 also played it’s role during last 18 months .

Now, there seems to be some pick up and L&T 's order book is a healthy 9 Lakh crore INR. Now the company is focussing on enhancing share holder value by divesting non-core business…

Its digital arms listed companies such as LTI, LTTS, Mind tree are doing exceedingly well…

A couple of good analytical reports would throw some light to the query that was raised. The second one is a detailed analysis by Sharekhan based upon Q1 2022 results.

Dicl: Invested at Rs 1200 level…not a buy or sell recommendation.

2 Likes

Its trading at very decent valuation too given the growth and holding companies discount not factored into its Mcap.

Trading well below its median PE -

If one does a simple SOTP valuation and knocks off 15-20% as a discount, the core business is available at a market cap of < 80,000 Cr.

This is the largest, most diversified and best run infrastructure business in the country so such an extent that one cannot think of a private capex cycle in India without L&T participating. On a standalone basis the business should be able to generate a PAT in the range of 6,000 Cr which means the market is assigning a multiple of less than 15 for the standalone business.

The market tends to underprice some businesses for years together based on the cycle and the narrative. The current narrative is that a decent quality chemical business will get a valuation of 50 PE but the best infra play in the country goes at less than 20 PE though it owns majority stake in subsidiaries like LTTI, LTTS & Mindtree - each of which has been on fire over the past year.

Investing in stories like L&T which are out of favor with the current narrative calls for a lot of patience and conviction, the number crunching part is often the easiest. As is often the case, stocks don’t rally purely based on under valuation. It calls for a mix of factors like better than expected earnings, good order book for a few quarters for the narrative to finally turn.

Disclosure: Invested for self and others, I am SEBI registered IA. Transactions in the past 30 days

11 Likes

L&T Launches L&T EduTech - A new industry-led, application-based, practical oriented hybrid online

learning platform to help create industry-ready talent.

2 Likes

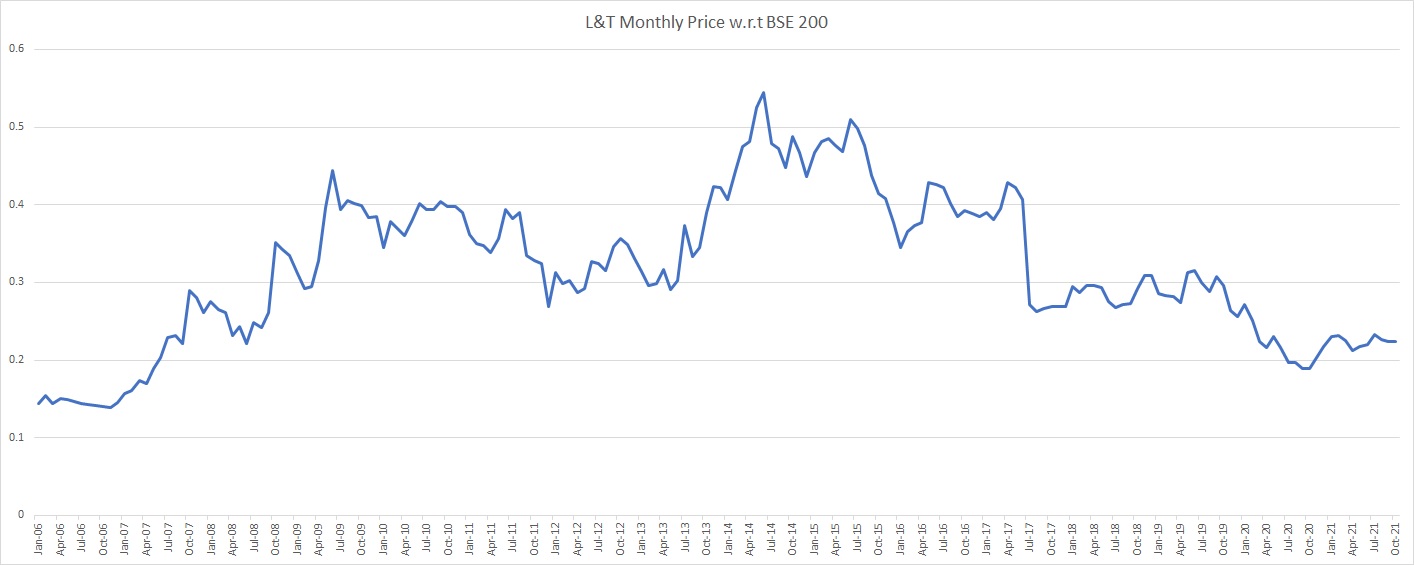

To understand the market’s perception till now, I plotted the relative price < monthly price as a % of BSE200> of the last 15 Yrs., and the overall trend is horizontal with typical short-term ebb and flow. I infer that the market has valued it as an average story on the basis of the past fundamentals.

Picture below for reference:

Using the results of the last 11 Yrs and weighing key fundamental indicators such as YoY trend for Sales, NI, BV, D/E, CFO, ROE, 5/10 yr trend for growth in sales/BV/CFO and few more, business scores an average category w.r.t the entire listed space.

Rationale noted by you is valid for any story & indicates a strategy to catch the pendulum’s swing.

In this instance, both technical and fundamental aspects indicate a mediocre business.

Disclosure: Not Invested.

2 Likes

can you tell in detail, why you think it has mediocre business?

It’s a relative inference after quantifying every business in the listed space on the basis of last 10 Yrs. data. Key categories to pick quantifiable parameters were:

- Fundamental factors spread across the B/S, P&L and CF. For example - YoY Growth in Sales, Net Income, Book Value, Operating Cash Flow

- Other hygienic factors such as Equity Dilution, Promoter Holding, Free Float, etc.

What all to include and how to weight each factor is up to individual’s understanding of equity research? However, the above approach is mechanical & only quantifies past outcomes whereas investor pays for future expectations. If valid reasons indicate a better earning power, human judgement prevails.

Below is one of the way to think in the right direction:

1 Like

Interesting, given the current order book where the management said, it is fully booked out for 5 years, the projections are average if your analysis is valid?

And this is before the PM’s gatishakti 2.0 announcement on Oct 13.

Disclosure: biased and accumulating at current prices of 1600+

That what makes the market tick - every one participating with their own assumptions. The information of fully booked for next 5 Yrs shall already be discounted in price. If future is better than expected, price would visit north instead of south.

Why I do not like this business much?

Profit (which is just an opinion) exists and shall increase further as order book gets executed. But, cash (which is a real fact) generation in tandem is too weak even though supplier’s payment has crossed 365 days . Every year, business rewards shareholders with dividend but keeps taking more and more debt.

I infer it as an empire building culture. How it will change in near future? If reasonable evidence exits against my inference, I could become a fellow shareholders. Right now, there are better alternative options.

L&T has robust liquidity, driven by cash and equivalent of Rs 47,200 crore as of March 2021, they aren’t raising debt to give out dividends.

If net profits are just opinion then CFO derived from Net profits and hence FCF are all opinion. Majority of the impact on cash inflow is due to Nabha power and L&T hybd Metro.

The group will continue to look for opportunities to divest its non-core developmental projects, including Nabha power and L&T Metro, over the medium term its expected to improve a lot ( u can do more number crunching on that - data is available ).

Yes,Gross current assets (GCA) net of cash were large at around 300 days. The group efficiently manages its working capital through customer advances and payables. Public backlog accounts for 80% of the total backlog, which mitigates the credit risk. The improving share of IT&TS has also helped limit the working capital requirement with standalone GCA being higher.

Given the intent of the management to judiciously bid for projects with lower working capital requirement as well as efforts in reducing outstanding receivables and inventory, GCA are expected to decline and will be a key monitorable over the long term.

There is no empire building culture, given the payment risks in infra sector ( mostly from gov side) L&T works as long as cashflows are payed on each incremental completion of projects , if gov stops the payment - L&T stops the work & it’s contracts to its suppliers are such that they will be payed only after Gov payed them the money, L&T model is very risk free.

They don’t own any of the risk in the very risky sector - the reason why they are able to raise money sometimes at GSEC + 50 bps rates.

There are colgate type of businesses where you will get the cashflows u are looking but u imaginary cashflow generating business has outperform colgate over 25 years. ( return since 1999 = 102x)

Colgate 15x since 1999

since 2002 it has outperformed HDFC bank as well

https://twitter.com/Dhruvapandey/status/1331206385183297542?s=20

May be u should reconsider your liking about the businesses.

12 Likes