I believe most of us would agree that having large inventory (aging of rice) is part of the KRBL’s business model. KRBL is where it is because of its ability and strength to age rice at such magnitude. There is no other player in the world - which procures and ages basmati rice to KRBL’s level. In a separate post I will share why aging helps KRBL to maintain its margin especially when industry is struggling to break-even in a bad cyclical year. Currently there has been consolidation going on in the industry, where many weaker players have been wiped out because of financial constraints which has reduced competitive intensity.

Bloating of inventory and debt during paddy procurement period may give an impression that this business doesn’t generate any FCF. This is true if someone views just end of the year financial statements. But the reality is quite different if looked at using proper lens, IMHO. As Buffett has said - a company should be viewed as an unfolding movie, not as a still photograph.

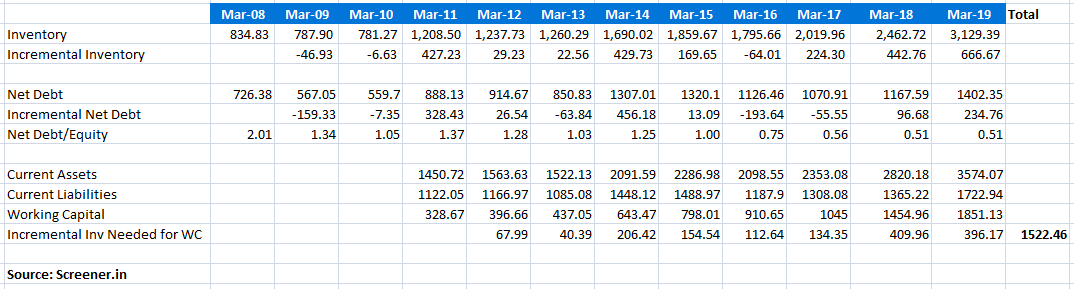

I’m making an humble attempt to share my lens with the readers. Let’s zoom out and look at few key metrics for last 9+ years and see how business has evolved and how the cash has been utilized by the business:

Inventory: has increased 2.6 times from 1208.5cr in FY2011 to 3129.39cr in FY2019. Last three years inventory has increased significantly from 1796cr in FY2016 to 3129cr in FY2019. My guess for sudden increase in inventory is increasing domestic demand and decreasing domestic competitive intensity, as company is attempting to increase its domestic market share.

Net Debt: has increased 1.58 times from 888cr in FY2011 to 1402cr in FY2019. Net debt has not increased at the same rate as inventory. In fact it has remained quite stable since FY2014 with downward trend. Net D/E was as high as 2.01 in FY2008, which has been brought down to 0.51 recently. I’m not too much worried about Debt levels as it becomes almost zero by month of September when sales converted to cash is used to payoff temporary higher debt levels.

Working Capital: has increased from 329cr in FY2011 to 1851cr in FY2019. KRBL has invested almost 1522cr to its WC during this period while increasing Net Debt levels from ~888cr to 1402cr. So we can say that around 500cr of 1522cr investment in WC has been funded by external debt where as 1000cr has been funded by internal accruals. If KRBL had not shared dividends (which it has been paying consistently for last several years) it could have almost fully funded its WC requirement.

My conclusion: WC is growing because underlying business is growing. As long as its WC is mostly funded by internal accruals, investors should be fine. According to me this is the key item that investors should monitor very closely. It may seem like this is a low FCF business. But in fact it has low FCF because it invests a lot of internal accruals in WC. Low FCF but high “Owner Earnings” business per Buffett. It is safe to treat investment in incremental WC as ‘Owner Earnings’ as long as incremental investment is done to grow the business. Please read my post on ‘Owner Earnings’ in BRL thread here.

If KRBL decides to not grow and be happy with its current scale, it can easily fund all of its current requirement of WC from internal accruals. It can be debt free business for March balance-sheet and can throw a lot of cash back to owners since it does’t need a lot of capital for capex.

KRBL is generating 35% ROIC net of investment in energy. It’s a consumer staple business, IMHO, available at 3x book growing at decent pace with good longevity. I will let readers decide on the valuation.

Risks: 1) tax claim of 1268cr + interest by IT which is under protest by KRBL 2) long-term people reducing consumption of white rice and perceiving it as unhealthy which lacks proper nutrients 3) many other risks which are unknown to me right now

Disc: invested and hence biased.