Completely agree. Specialization (for that matter, diversification too) is a double edged sword…but wielding such sword required special skill and maturity which is what separates men from the boys. I think recent Honda deal has proven that KPIT has really grown up, from being a small town, bits and pieces software company, into global full fledged automotive software company with marquee clientele like BMW, Renault and now Honda. Those who have experience in auto component industry would know how difficult it is to get long term supply deal with large Japanese auto OEMs like Honda or Toyota.

1 Like

Even though I am not courageous enough to buy, i didn’t sell in today’s carnage…Will wait and see what management says after results. I know stock price cannot keep in going up every week/month. But falling from every new high gives more pain as in absolute value terms we loose much more even though stock falls say 10%. When KPIT was peaking up few months earlier around 800 when Goodman Sachs was giving buy report I felt like it was top for KPIT. But it’s trading above and keep on adding new clients, acquiring related companies, growing QOQ with each passing quarter, some times it feals fearful to book profit also…!!

1 Like

expecting downside as the valuations were uncomfortable, same situations happened earlier & stock had a beating of 40%, competitor is running with 30 PE & this stock with 70+ PE, promoters are also not comfortable with valuations & selling as well, otherwise fundamentally still good enough to bounce back, management +1 always, at least 40-50% downside is expecting ,

A lot depends on upcoming quarterly results and management commentary on the report.

However, Kpit has been riding on a bull despite bearish broader sentiments across market. PE ratio too was not providing a good entry point.

If the growth story remains intact, this can be good buying time.

However, is there a way we can track automobile cyclicity? At what stage of the cycle are we in he automobile industry.

Narrative build by JPM is completely baseless. KPIT is different from all other Automotive suppliers like Tata Elxsi, LTTS or even Tata Technologies.

The following are the main differences

- KPIT is mainly focusing on OEMs(High margin, high risk, difficult to enter ) but other are focusing on Tier-1(low risk but any SW company can enter in to this space).

- KPIT enjoying monopoly in some engineering activities at OEM level that the OEM don’t have the skill and the European and US Tier-1 are very expensive. That’s why KPIT is adding more and more OEMs in recent times.

- Once an OEM is added, revenue increase will be visible only after 2-3 years( development cycle is arond 2-4 years now).

- Winning new big project is relatively easy, once they prove their capabilities

I think it will take minimum 10 years for Tata Elxsi, LTTS and Tata Technologies to compete with KPIT in the OEMs core engineering space.Others are quite happy with low quality work as they can execute such activities with relatively freshers (1-2 years experienced ) hence the margin is very high.

D:Invested at very low level (average 45)

14 Likes

exactly, but valuation wise in this sideways market it’s not sustainable , many mf & pms has a good chunk in kpit & they will create opportunity to book profit and make fresh entry , more correction is expected ahead, if investment is at extreme margin of safety then sticking to it is justified

4 Likes

Short term we cannot predict the price movement and I am least bothered, even in KPIT itself we have seen such corrections many times in the past. The only potential RISK I foresee in KPIT is “a big failure in any of the currently operating project that will affect the relationship with OEM”(car call back/ liability issues etc.), that will definitely affect their growth. Any such news will be a trigger for me to exit. Otherwise untill 2028 they could easily maintain above 20% growth. KPIT is aiming only tiny bit of Giant 800B Automotive SW market

8 Likes

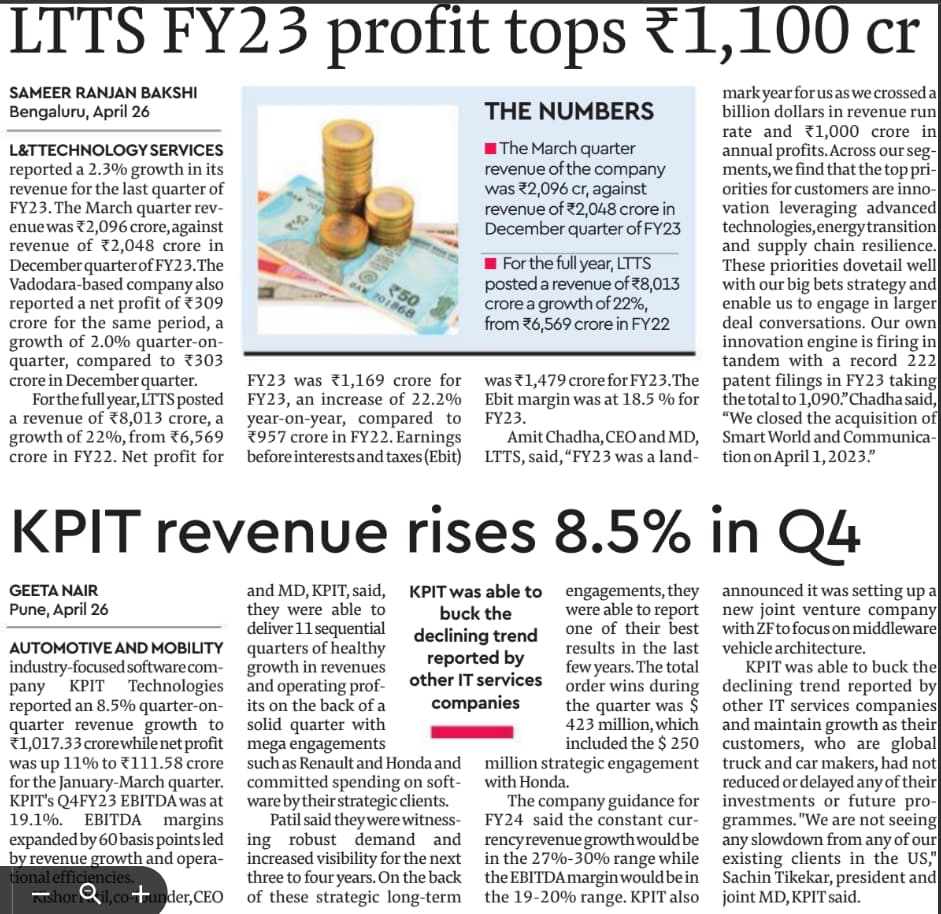

Good results from KPIT

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f30abcc1-788f-400d-b2df-6905a03fac24.pdf

Big News

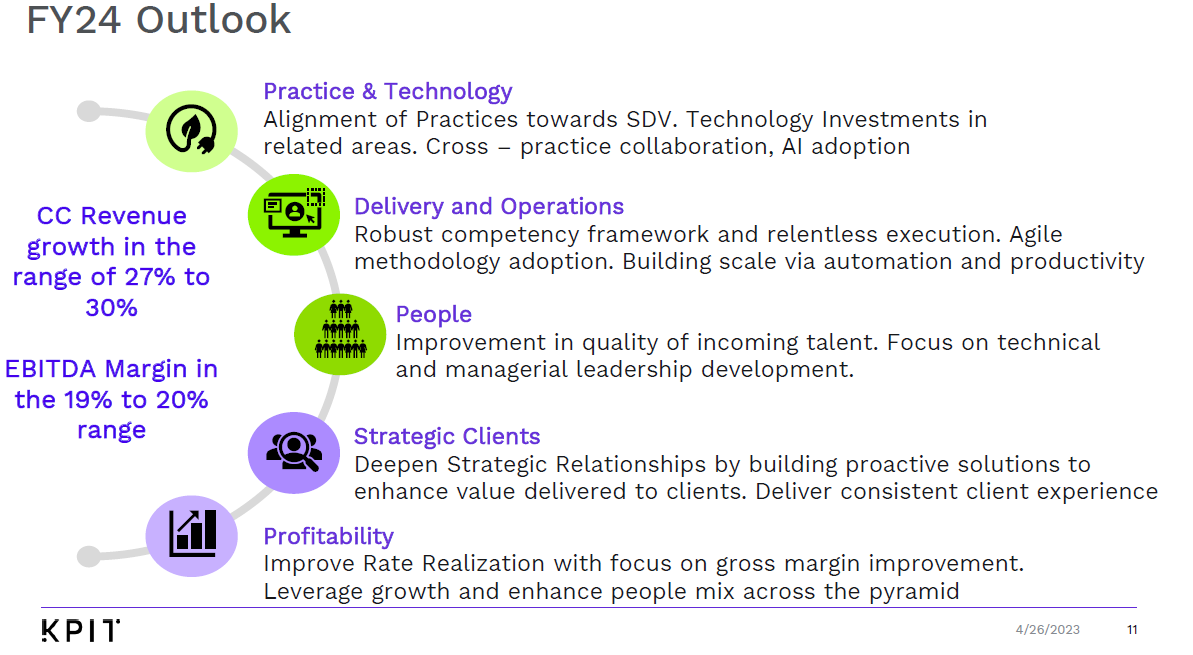

Very good guidance for FY 24

8 Likes

Wow .What a result…

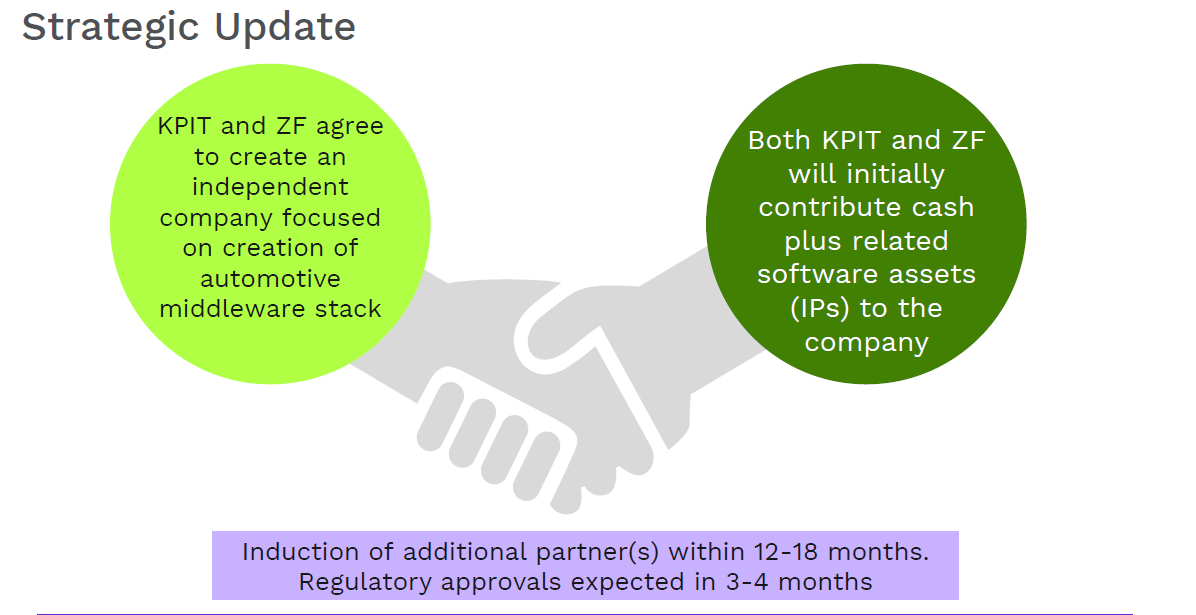

ZF agreement is something interesting to track for the future…

2 Likes

These 2 companies result confirm that ER&D space companies are able to buck trend compared to pure IT services companies

1 Like

4 Likes

I was reviewing the recent interview of Kishore Patil of KPIT, few highlights -

Credits: Comfortable With FY24 Guidance: KPIT Technologies | CNBC TV18 - YouTube

KPIT Tech is confident in meeting its outlook for the year, despite market inquiries about the growth guidance not being higher. Despite the slowdown, the client expressed the priority in the space of OEMs.

Mr. Patel clarifies that the company does not provide quarterly guidance, and any upgrades to the guidance will be considered at the end of quarter three.

The market has concerns about Honda diversifying its vendor base, potentially impacting KPIT Tech’s business, but Mr. Patel assures that the partnership remains strong and they are accelerating their engagement.

KPIT Tech’s partnership with Honda is not exclusive, as there are various projects and activities that each party works on independently.

The company’s business model focuses on growth, scalability, and strengthening relationships with all 25 clients, not solely relying on big announcements.

KPIT Tech sees potential for more opportunities and collaborations in the future with other global auto OEMs, indicating a positive outlook for further growth and expansion.

H1 will be strong and KPIT Mgm will review the guidance for the rest of the quarters in

Q3.

3 Likes

Finally i fully sold KPIT, one of the star performer in my PF. My investment average was close to just 60 rupees and exit average is Rs 1078 total holding time 3.5 years

I am sure KPIT will continue doing good with reasonable growth. But the current valuation is only justified if it can maintain the same growth. I personally foresee following medium to long term risk, based on that i made my mind

- New OEM addition will be difficult for KPIT (All low hanging fruits are already in )

- Most of the big OEMs are tightening their wallet, switching integration activities in house which is KPITs core business.

- KPITs diversification and acquisition are not in their core expertize area ( In those domains there are better players globally).

7 Likes

Now it will be range bound till the valuation justify growth , although promoter is very focused on their domain but in case the R&D expenses by the OEM gets paused for a while it will hit the co hard bcoz it has a single vertical i,e Auto only

I agree that the valuation is quite rich. But that is the combination of a large TAM and KPIT’s consistent track record of meeting revenue and margin guidance. I think the stock price should keep up with the guided 30% growth over the next year, plus a potential bonus from margin improvement over the next year. Obviously, there is a downside risk of failing to meet these.

- New OEM addition will be difficult for KPIT (All low hanging fruits are already in )

They have 60 OEMs already as clients. They have repeatedly said that they want to focus on their top 25 clients. I doubt they are actively looking for new clients. Their focus is to widen and deepen existing relationships

- Most of the big OEMs are tightening their wallet, switching integration activities in house which is KPITs core business.

Most OEMs are still hardware companies at heart. Moving to producing software at scale will take years and they will rely on third parties. I don’t think many have got their act together. If you look at the first generation of electric cars from large OEMs (like Merc and VW) their in-car software usability is woeful as compared to Tesla.

- KPITs diversification and acquisition are not in their core expertise area ( In those domains there are better players globally).

Which acquisition you don’t like? I thought the Technica acquisition was a masterstroke. Plus the advantage of trading at 70x multiples means they can buy other companies and still be earnings accretive.

In addition, there are economies of scale that can play out. For e.g. once you get expertise with integration with Android Automotive platform with one OEM, the tools, accelerators, and expertise developed will be valuable to other OEMs. Each OEM uses a lot of common third-party components from CPUs (silicon), sensors (lidar), subsystems such as steering. So I think there is space for an external company to provide expertise. Inhouse development teams would focus on the OEM platform.

Management commentary was very bullish.

3 Likes

I would like to add my 2 cents on this topic.

- Electric cars doesn’t add any additional software components except some BMS stuff. Major software development in cars is for infotainament and it has no bearing whether it is ICE or electric.

- All big OEM’s are spending heavily on Software and I can confidently say they are not going to stop anytime soon.

- Most OEM’s have their own strategy for Software defined vehicle such as MB.OS, VW.OS etc.

- All big OEM’s have opened their own software arms to focus entirely on software development, reusability and to reduce lead time to market. These sw arms are a competitor to companies like KPIT, LTTS.

- Tesla’s has first mover advantage w.r.t ADAS but everything else their european counterparts are up there.

More and more sw development from OEM’s are given to their daugther SW companies. As and when these companies are ready to take extra pie, companies like KPIT, LTTS are replaced and development happens inhouse. In Indian context, most of SW for JLR is developed by TCS, Tata Elxi, Tata technologies and JLR itself because it is easier for the OEM’s to work that way. Hence you don’t hear any company announcing they’re supplying major sw to JLR. Same is the case with Mercedes. I can say for a fact KPIT and LTTS should draw major revenue from BMW and Volvo respectively in their transportation vertical.

Having said all of this, SW providers like KPIT and LTTS should still get lot of work from OEM’s as there are scarcity of resources on their end and also in market for good SW developers.

KPIT should still continue to grow but I’m not certain if the growth rate will sustain. If KPIT’s gowth projection is faltered anytime then I think the it’ll be rerated ruthlessly in my opinion.

Disclosure:Not invested. I missed KPIT and Tejas networks back in 2019 when I didn’t hear good review from my friends who works there. Imagine my sadness when I opened my kite in 2023!.

1 Like

- Electric cars doesn’t add any additional software components except some BMS stuff. Major software development in cars is for infotainament and it has no bearing whether it is ICE or electric.

I would disagree there. New cars are now driven by central software OS from unlocking, to transmission, safety, driver assistance, infotainament etc, with OTA updates and connectivity. Previously there were multiple independent controllers doing cruise control, locking, infotainament all disconnected from each other.

1 Like

This short interview may give some idea of KPIT management thinking. I liked hence sharing.

5 Likes

Just jotting down my random thoughts on my journey with KPIT - Buying, Holding, and Selling (Zero).

I’ve made numerous investment blunders in the past, but fortunately, KPIT has been picture-perfect thus far. My foray into the market occurred during covid, and it was during this period that I stumbled upon KPIT, thanks to a valuable pointer from a VP. The timing couldn’t have been better.

My initial entry point was at Rs. 42, and over time, I progressively increased my exposure by meticulously monitoring its performance. The most recent significant addition to my portfolio was at Rs. 650, resulting in an average acquisition cost of Rs. 340. Notably, KPIT now constitutes a substantial 19% of my portfolio, making it my most prominent holding.

I’d like to extend my heartfelt gratitude to my VP friends for their invaluable insights, which have undoubtedly played a pivotal role in this journey. With fingers crossed, I’m hopeful for similar strokes of luck in the future.

Disc: Holding as indicated, hence views are biased.

14 Likes

Did you think of booking profits when the price reached ATH levels? Or do you keep trailing stop loss?

Even I am holding KPIT but have reduced my position over time and booked the gains. Would like to know how to handle multibaggers ![]()