I would refrain from commenting on the Medical College business until after a couple of years of normal operation. As of now, I estimate that the IRR from it is good enough to not worry about it for at least that long.

If I remember correctly, Chennai expansion also had a similar budget (Somewhere around Rs. 500 Crores). So that project has been scrapped in favor of the Medical College (Which is a little north of Rs. 600 Crores).

Personally, I think it was good that they scrapped Chennai expansion. Tier-I cities are not easy to compete in and they will have to let go of a some of the Margins just to remain Competitive. I would be more happy if they continued to expand in Tier-II or Tier-III cities, because that’s where I think the penetration is low and opportunity for inclusion into healthcare is very high.

350 beds for the Medical College. 350 are regular beds. But both will produce Revenues, of course.

It’s precautions and effects of COVID19, especially focusing on re-infections. The person being interviewed is the Infectious Diseases Expert at KMCH, Dr. Varun Sundaramoorthy.

The main hospitals/competition in coimbatore are GKNM Hospital, PSG hospital and Ramakrishna Hospital. A hospital named Royal Care was established 2-3 years ago. However, KMCH does have a solid reputation. Both their cardiology and oncology departments are one of the best options in Coimbatore. Some or the other construction is going on regularly in their campus. Also, a senior level medical rep who frequently goes to this hospital said they keep their equipment updated with the latest that can be found anywhere in India. Might be good to find out how good they are in paying the suppliers.

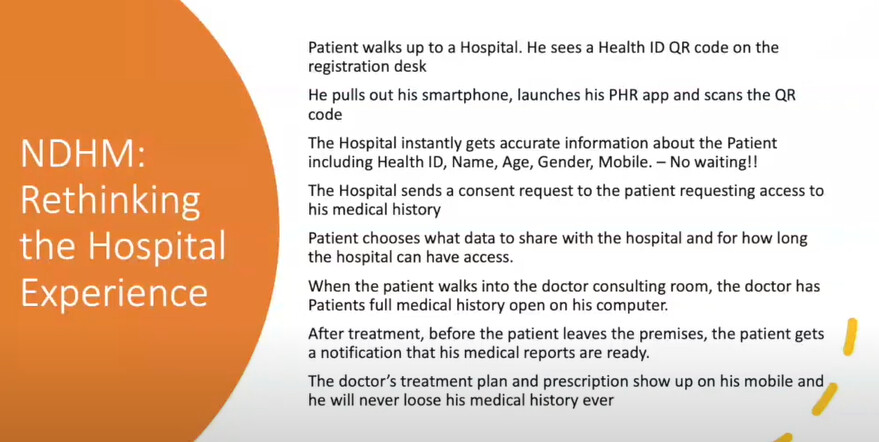

A webinar on the National Digital Health Mission ecosystem which will work similar to the RBI’s Account Aggregator framework. 5 years from now, hospitals will have more efficiency with the help of data and patients will have better experience.

Account Aggregator is already live, thanks to RBI’s initiatives. I am not sure about this Healthcare Record ecosystem since we do not know if Govt is interested enough to push hospitals to implement it.

One possibility is that usually NEET exams for admission to medical courses take place post board exams between april to june and sessions start between july-sept.

This year entrance exams took place in November due to COVID.

So possible admissions have got delayed so hopefully these revenues will move to q4.

Hope this helps.

My guess is after having undergraduates (MBBS) for few years (at least 5), they will try to get the license for post graduate seats in various specialties. This will add massively to the revenue compared to undergraduate seats. But even if this happens…it is quite a few years away.

Consider 75 seats after 5 years for PG I.e. 50% of MBBS. Meanwhile expect MBBS to increase to maximum I.e.250. Then PG to 125. This way medical college is growing business. It will take 10 years for full potential.

As the audited financial statement has come out here are some of the highlights and my opinion.

Income statement:

FY2021 (cr)

FY2020 (cr)

% Change

Revenue from Operation

690.36

711.73

-3.00%

Profit Before tax

105.74

111.91

-5.51%

Profit after tax

77.69

94.59

-17.87%

Fiannce Cost

31.31

14.62

114.16%

Depreciation

68.03

52.12

30.53%

Revenue has dropped by 3% compared to last year. It is difficult to come to the conclusion why Considering covid situation. Hope we get more information in AR.

The significant drop in PAT can be attributed to three things.

Increase in Finance cost - which I think is due to moving the interest expense to the income statement (As previously it was capitalized under PPE)

Deferred tax benefit in FY2020, which reduced the total tax in FY2020.

Depreciation caused by the addition of CAPEX.

All these were expected and so to me, it looks like both the topline and bottom-line are more or less flat compared to last year.

It would be interesting to read the AR on these line items to get more details.

FY2021

FY2020

Interest coverage ratio

4.4

8.6

There is a significant reduction in the Interest coverage ratio. Again I think this is because of the Interest expense moved to the Income statement.

Balance sheet:

The one thing that is surprising to me is the increased long-term borrowing of 46cr and the Bank balance of 148 cr.

I presumed that all the Capex was completed for the college, but the borrowing and bank balance tell otherwise.

FY2021

FY2020

Net Fixed Asset Turnover

0.82

1.28

Receivables days

5

5

Inventory Turnover

59

62

Working capital cycle days

11

11

NFAT should improve to the historic level of 1.5 in a couple of years once we see additional revenue from the Education segment.

Cashflow:

FY2021 (cr)

CFO

186.38

CFI

-180.48

CFF

38.03

FCF

-21.72

(note: I have subtracted finance cost in calculating FCF as it gives a more conservative look at cash available for Shareholders)

FCF is negative and I think will continue to be negative next year. Hopefully from FY2023, we will start seeing positive free cash flow.

Segment wise Revenue, Results and Capital Employed

Reveneue

FY2021 (cr)

FY2020 (cr)

% Change

Healthcare

668.4

697.16

-4.13%

Education

21.96

14.57

50.72%

Profit Before Interest Tax

FY2021 (cr)

FY2020 (cr)

% Change

Healthcare

138.4

132.96

4.09%

Education

-1.36

-6.43

Revenue of Education segment has increased from 14.75 cr in 2020 to 21.96 Cr and the profit is still negative. We have to wait for a couple of years to see the benefit.

Conclusion:

I would consider this more or less a flat year for the company.

AR will be very interesting to read to correctly understand the

Reason for decline in revenue in the healthcare segment

Future planned Capex spending with the 148 cr in Bank balance.

Even he can’t bear his own hospital bill. How come common people will be able to bear. Purani( his daughter name) hospital supply is a clear way of siphoning 40+ cr money. At least they can siphon in much better way.

Almost, all promoter cheat minority shareholders. It’s not black or white… just a area of gray. We have to decide our shade of grey.

Recently, I shifted to Coimbatore. Being a doctor, I don’t think it’s a high capex and low return (akin to plane).

Hospitals capitalise on patients fear. So, they extort every penny of patients saving. Unlike air transport, where you can refrain

But it’s never reflected in any hospitals balance sheet. I think almost most hospitals like Apollo, kmch do siphoning.

One interesting thing to note is that although Kovai calls itself a super Speciality hospital, the revenue per occupied bed (ARPOB) is only 16k. This number is much much higher for other hospital chains.

For eg.

Narayana Hrudayala is at 22k

Shalby Hospitals is at 30k

Apollo at 32k

Fortis at 40k

I am trying to understand if KMCH is into low value operations/surgeries? Average billing for the hospital seems to be pretty low vs. others.

Can anyone throw some light on the average billing numbers for Fortis, Apollo and why they are so much higher ?

Some one need to see local news or govt bulletin to know how many bed got allocated for Covid in this hospital. If % is low, that would explain low revenue.

In my opinion, it can’t be compared in such a way. Perhaps we should look at a comparable hospital like KMC Specialty which operates in the same region (Tamil Nadu) as Kovai does.

Here is a link to the post that I had written in the past- Kovai Medical Center and Hospital - Health and Wealth - #281 by aga.ayush11

You can see in that table (although the data is a year old, but still relevant) that Kovai and KMC both have one of the highest margins in the industry despite the lowest ARPBO. While some of it may be true that Apollo and Fortis may do more surgeries but as I have highlighted in my AR20 notes and others who have visited the hospital in person have mentioned that Kovai has a top-notch infra in place. In fact, this gives me confidence that ARPBO can go up from here and growth can also come from the existing infrastructure.

This is an interesting metric and thanks for bringing it to attention. As a side note one of the highest ARPOB is reported by Artemis ( gurgaon ) of about 59k.