Interest Capitalization

Most of us are aware of the interest capitalization. So, when you calculate Book Interest % (Interest Paid / Debt), you are double-counting the capitalized interest. For instance, Debt has increased drastically only in the last 2 years. If you look at the Financing Cash Flow, you will see that the combined value for 2017 and 2018 is Rs. 220 Crores (Dividends not adjusted, but those are small anyway). But Book Value of Debt actually increased by Rs. 253 by the same period. Conceivably, the extra Rs. 33 Crores will probably be the capitalized part. So in a sense, actual interest paid will be ~Rs. 20-22 Crores (9-10% of Rs. 220 Crores), as opposed to the Rs. 12 Crores being shown right now. I’m personally against this twisted Accounting by KMCH, by the way.

But my point was, since there is no need for Debt anymore, it will be pared down once the Medical College starts producing cash flows. This has indeed been the case in the past. The 4 years leading up to this huge Capex (2014-2017) have been years where KMCH paid off a substantial amount of Debt on the books (Almost ~40% reduction).

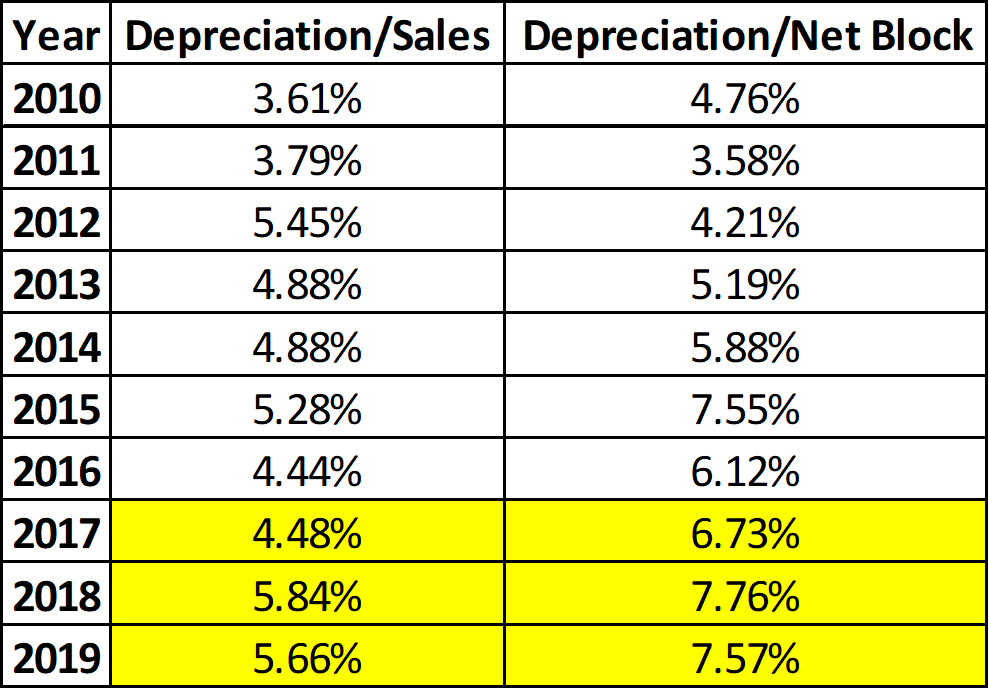

Depreciation Capitalization

In my very limited understanding of Accounting, ‘Capitalize’ means adding something to the B/S and ‘Depreciate’ means reducing something from the B/S. So I don’t think ‘Capitalizing Depreciation’ makes sense. KMCH does not have any accounting policies indicating the same. If you are aware of any, please enlighten me.

Once again, if you look at the “Depreciation / Net Block” or “Depreciation / Sales” Ratio, there has been a pronounced increase in the last 2-3 years. I don’t see any reason why it should increase even further. In fact, some PP&E were revalued last year and increased in value. So it is highly unlikely that Depreciation will be even higher in the coming years (Unless, of course, some new Capex is in the cards).