What is the logic behind your valuation here?I just want to know your logic too.Please feel free to share.

Personally i have been looking at this for a while and am thinking to make an investment.

What is the logic behind your valuation here?I just want to know your logic too.Please feel free to share.

Personally i have been looking at this for a while and am thinking to make an investment.

One can easily check the volumes in a quarter when the buying was done. The day volumes shot up around 130.

Also, he holds it still.

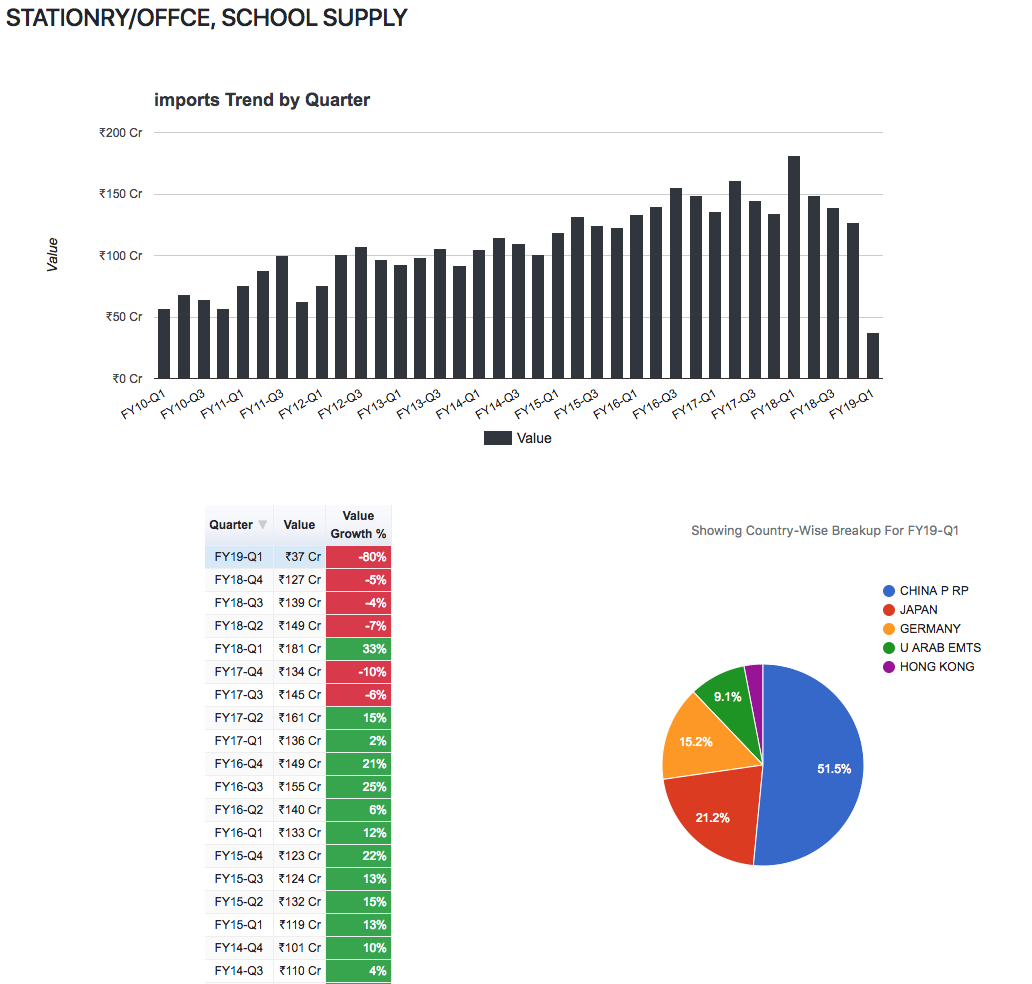

Stationary imports seem to be on a declining trend (Notice the main country of import - Over 50% from China and used to be close to 60% in preceding years). Please note that Q1 data is incomplete so the decline looks drastic while its not.

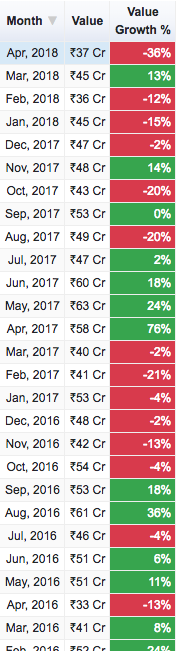

This is the actual month-on-month import data for Stationary and the big drop in Apr is a very encouraging sign. We don’t seem to have imports per month under 40 Cr in over two years (Apr '16) and before that one-off month, you have to go all the way back to FY13.

We have to follow if this is an emerging trend and if its sustainable and if there is some govt. policy behind it.

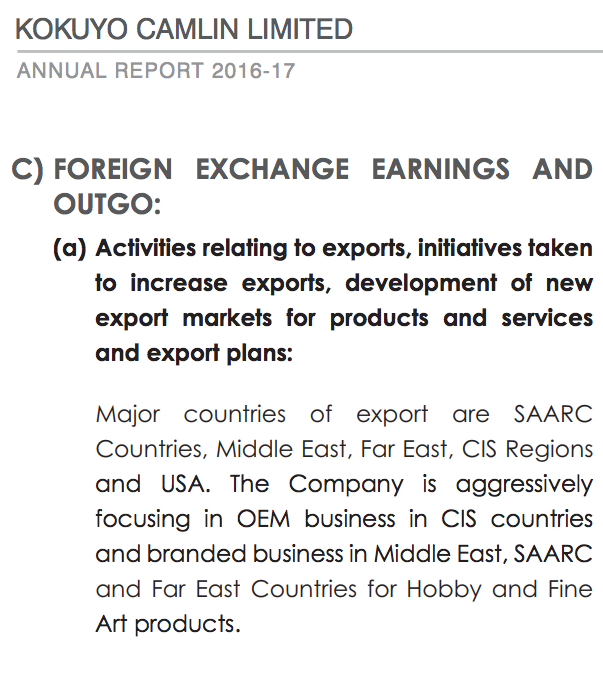

Then I found this in FY17 AR. Looks like they were looking to find export markets for their products.

Was this perhaps the reason for better numbers? Let’s look at export data for Stationary.

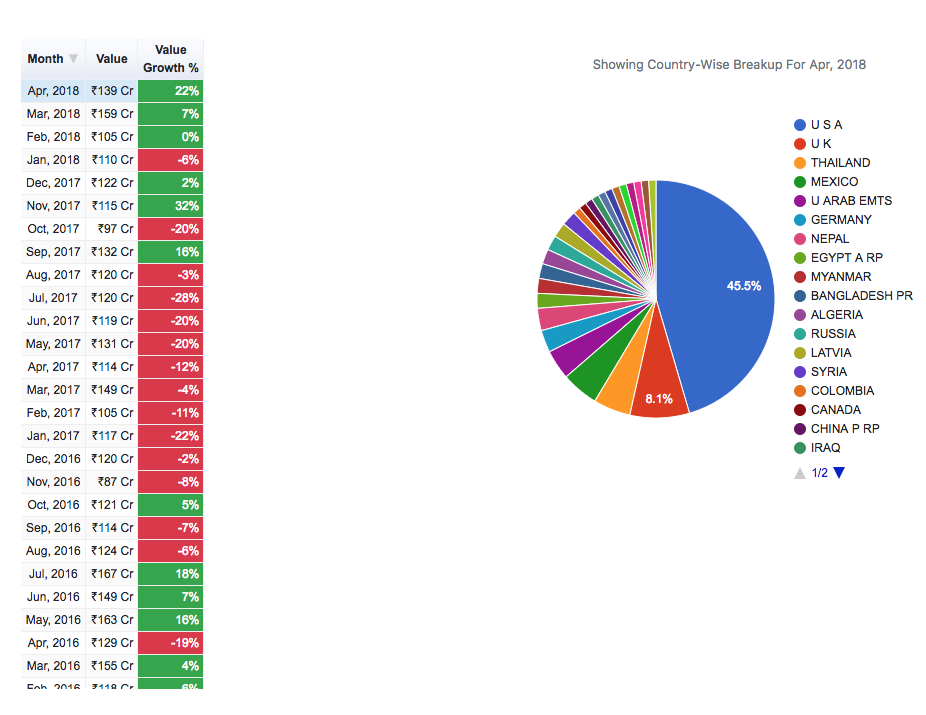

Q3 and Q4 months are showing some green and more importantly, Apr is showing a big growth. Maybe they have found some export market? USA contribution wasn’t this high in any of the previous years/months as it was in April. Not sure if this will be a one-off.

The Chinese imports reducing could have two effects

So overall it does look like there are some green shoots in this sector. Let’s see how it plays out.

Another thing I was wondering was if Kokuyo invested in Camlin so that they could use relatively cheaper manufacturing in India to export to other countries - sort of like a contract-manufacturer. This idea need to be explored to see what might be the reason Kokuyo invested in Camlin so that we can see if their vision aligns with our investment.

Risks:

I think only the AR can shed more light on what’s improving so we can make out if its sustainable or not. Until then we can only speculate.

Note: Take the export/import data with a pinch of salt. I might come across as a man with a hammer. Even if macro is improving, there a lot of other factors which will decide if this company makes a good investment or not.

First of all Thanks to @phreakv6 for developing website on exports and imports data.

Stationary Exports and Imports look like this:

Completely nailed it by @drvijaymalik

Excellent reply from Dr Malik… Must read for investors in this industry. Thanks for sharing.

This company needs serious intervention from the experts for the experienced investors present at the forum.

Promoters are just like jokers Dandekar brothers are spoiling the company…

Why the kokuyo Japan continue old chairman when they had 75% holding in the company.

Everything is in a favour of the company in spite that the old promoters literally ruined the company.

Whenever I hear it about kokuyo Camlin I feel it could be next 3M India.

Disc. Not invested

Both Kokuyo and Camlin are incredible brands - however, old promoters , now managers seem to be disconnected with the market. They are unable to position the company in a favorable environment. Innovate products from Kokuyo are marketed in a half minded manner or not marketed at all. Whats going on here!

Disc: invested

Kokuyo Japan is missing out the big opportunity in India. Single digit growth in Japan business is great, however a death warrant in Indian stationary and art space today. There are times when you really have to go full throttle, and the time is now. However Indian management has put the company on cruise control. Competitors are overtaking(Doms, Cello, Linc, HP, ITC, Pidilite etc) yet the parent company lacks proximity to Indian market. If focused well, Kokuyo can turn this India subsidiary into a $1B+ business in another 15 years. Tepid growth in Japanese market should not deter the parent to accelerate in a market like India. Art network is a good thing the current promoters have done, however there is more work needed in sales, channels, marketing and distribution.

Appointment of Mr. Masaharu Inoue may change the course. Demand pull is helping the company as of today, along with the softened raw material prices. The company has potential to double the sales in every 4 years, given the parent’s capabilities. Unfortunately, the company lacks the push as of today.

Key shareholder is missing from the action to fire up that ambition. Can Kokuyo and Mr.Masaharu Inoue correct it?

Disc: Invested.

A classical example for Principal-Agent problem. Competitors are raising so much money for aggressive expansion. Yet, Camlin is jogging in a sprinting track. It is upto the Kokuyo Japan board to act. Now that the company has steadied its operations and the parent has gained full control, the time is apt to unlock the next level of growth potential (new products, marketing, channels, sales and distribution) to replicate the success in the Japan market.

Disc:invested

Presentation made at the AGM.