Sabu jacob even added that when Kitex USA turns profitable he might remove KCL as its co owner and make it 100 percent KGL owned.

He expects kitex usa to become profitable in a couple of years as majority costs r fixed. Kitex usa has hired a 8 man management team and is paying heavy salaries to them right now. He has some very experienced and senior people in the team.

I also asked him regarding the increasing spend on CSR.he said he will take loan in personal capacity and do it from next year onwards.

From what i understood from the locals is that CSR spending is actually required in states like kerala to garner local support in order to run business smoothly.kerala is typically a tough place to do business with severe labor problems and political goons. Hence the need for kitex to get into gram panchayat and stuff… these reports of sabu jacob having political ambitions are completely baseless.

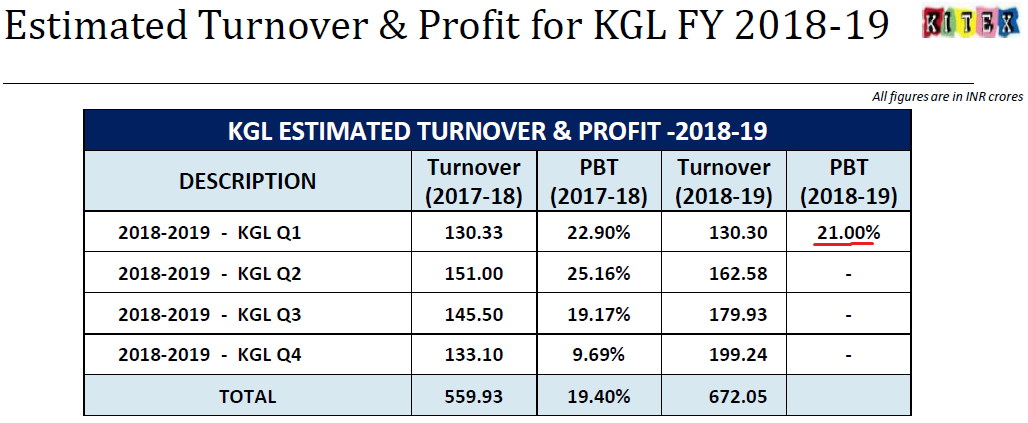

Seems like company has accidently revealed Q1 results in AGM presentation by giving margin % numbers…works out to be 27cr PBT…Lets see ;)(Q1 results are on 13th Aug)

results for this quarter

turnover of - 132.22 cr ( other income - 9.41 cr)

PBT - 30.16 cr

Kitex gave decent numbers for Q1FY19.

- EBITDA Margins declined yoy from 28.19% to 22.82%. EBITDA Margins improved qoq from 14.46% to 22.82%.

- Current qrtr working was supported by Rs. 9.4 cr Other income.

- Appointment of Mr. Krishnaraj S. as CFO from 01.10.2018. Mr. Krishnaraj S. has a good background.

- Setting up unit in Infopark SEZ in Kochi with project cost of Rs. 3 cr.

Board Meeting outcome.

Regards

Harshit

Is there any impact of flood on production?

Sabu M Jacob and kitex story in andhra pradesh news paper sunday edition … inspiring

The prices are going steeply up since Wednesday 29th Aug 2018. Despite looking around, I fail to see any reason for this. The unaudited quarterly results were declared on 13th Aug (18 days ago), and since then it only went down slightly after trading flat. Anyone can shed any light on this?

Disclaimer: I’m relatively new to investing world, so kindly excuse me if this is a stupid question. I’m interested in Kitex as have small holding that were purchased about 8-10 years ago by my father and I’m now trying to get to the bottom of this.

Latest interview…

Rgds

RR

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=f487c7e2-dd00-4acd-a3bb-9178af746717

incorporation of wholly owned subsidiary in the name of ‘Kitex Littlewear Limited’. How different is it from the current line of business?

As per the BSE shareholding pattern, Valuequest moat fund reduced its holding in Q1 2018 and exited completely in Q2 2018. Could it be indicating deeper troubles with governance? I guess VQ moat fund would have exited taking a loss…

Yes, as per the latest shareholding pattern, Valuequest Moat Fund has exited.

Regarding governance, various issues have already been discussed extensively on the forum. It would be prudent for members to pay attention to them.

On the business side - all the subsidiaries have been incorporated as per the AGM presentation. Personally I am not sure of the logic of so many subsidiaries though.

New CFO appointment is a definite positive.

Would be good if they restart the investor conf calls. Would be great if we could get updates on the business side of things:

- Have new clients been tied up for the large capex plans?

- Who are those clients? I am assuming there would be a lengthy approval process and if so at what stage are those approval plans now?

- Little Star and Lamaze performance and future plans on the brand. How active would be the marketing for these brands?

- Capex related details - Has the land been finalized?

- Health of other US brick and mortar retailers and how much can we increase supply to existing clients with new capex plans?

- In the past Mr Sabu had mentioned that they had already started trials for Target, Walmart by sending them small samples and he expects big orders from them? Has there been any progress on those?

Recently when I searched for little star organic on Walmart website I found some products listed. See below

https://www.walmart.com/search/?query=little%20star%20organic&cat_id=0&typeahead=little%20star

However when I searched for the same on Target website, it doesn’t seem to be listed. - Any specific plans to engage with big online retailers like Amazon?

Disc: Holding

Thanks for your response. Good set of questions. WiIl wait for somebody to answer the same. Hoping for a good recovery.

Disclaimer -Holding.

good set of results

-revenue at 181 cr( includes other income of 13 cr ) as against 151 cr yoy

-PBT at 41.45 cr as against 38.3 cr last year.

- PBT margins at 23 % ; EBITDA margin at 27 %;

- turnover of the company has been slightly better than the projections given in the AGM for this quarter.

Disc- Invested

Decent P&L nos but important to look at the balance sheet as well. Important points to note are:

- Working capital has increased and this could be the new normal (similar to what we saw in March 18 balance sheet too). Need to understand how much of the sales are to Kitex USA and the corresponding receivables from Kitex USA compared to sales and receivables of other clients.

- Short term borrowings of 65Cr. After bringing it down to almost zero in the last year they have started taking short term loans again.

- Cash balance has increased to 129Cr from ~93Cr.

investor presentation

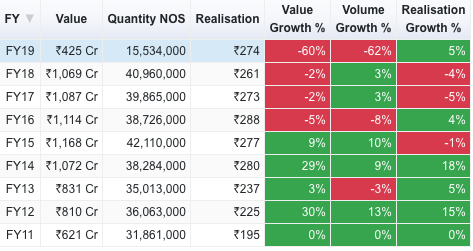

Export numbers for baby garments has pretty much mirrored Kitex’s topline. FY11 to FY15 showing value growth at different rates and stagnant/receding since (FY19 numbers are till Sept). Realisation per piece doesn’t seem to have even kept pace with inflation.

With cotton yarn prices inching up now, should affect gross margins further. They are passing on some of it going by the realisation increases in recent months but yarn prices seem to have gone up about 20% levels in Q2, so the pain seen in the about 1000 bps reduction in gross margins for kitex in Q2 as well is in line with these numbers.

Kitex Garment latest credit rating report by ICRA, rating is reaffirmed.

Key Points

- The Group is expected to record revenue growth of over 20% in the current fiscal, as reflected in its steady H1 FY2019 performance and strong order book position at the end of Q2 FY2019, driven by a combination of healthy growth in volumes and moderate improvement in realisations.

- Besides a modest revenue growth in FY2018, the operating margins fell sharply due to reduction in export incentives post implementation of the Goods and Services Tax (GST) coupled with rising operating costs.

- Operating margins over the medium term are expected to remain at around 25-27%, driven by its integrated manufacturing setup with a high level of automation and strong operating efficiencies.

- Addition of new customers and consistent growth in order inflow from existing large customers are likely to drive steady revenue growth of 15-20% over the medium term.

- The Group’s performance improved in H1 FY2019, driven primarily by growth in volumes. With the order book position remaining at healthy levels at the end of September 2018 coupled with recent addition of new customers, volumes are likely to witness a robust growth of 15-20% over the medium term.

- Top three customers of the Group continue to contribute to more than 90% of volumes.

- Capital expenditure plan of Rs. 910 crore for the period FY2019 to FY2025 towards significant addition of capacities across the value chain including knitting, processing and garmenting. The Group’s cash accruals are expected to remain more than Rs. 150 crore per annum during the same period, which would result in Total Debt to Tangible Net Worth (TD/TNW) and Total Debt to operating profits (TD/OPBDITA) not exceeding 0.4 times and 1.0 times, respectively.

Regards

Harshit

The rating is for the group. The financials presented show a marked improvement for KCL compared to KGL.

https://rss.acast.com/theeconomistmoneytalks

Listen to the second story in the above podcast about a company in China that is using indigenous automation to improve productivity in textiles.

https://www.lesouk.co/articles/tex-style-news/china-invests-in-robots-to-modernize-textile-factories

So, we need a big push in automation and robotics in India by the Indian Govt as well to compete with companies from China.

What about the unions in India? Will they be willing to modernize?

Is Kitex Garments Ltd where Berkshire Hathaway, the textile company was before Warren Buffet took over? Invest money to keep up or go out of business but won’t be able to stay ahead of the curve because everybody is doing the same?

Kitex Annual Report talks about automation and the difficulties it has faced in implementation. What kind of automation? Will they be competing with automation in the US markets implemented by the textile companies there? Or will Kitex still hold an advantage with the labor cost which will be still required? How long before the automation reaches a level where the manual labour cost is not a factor?

Disclosure: Invested, on Hold.