Quote

I believe that depending too much on management meetings can lead one up the garden path. 'I tend to ignore all the signals that the management gives out consciously. I don’t want to pick up those signals. They can be doctored…. I am not a very qualitative, gut-feel kind of a guy. I mostly go by numbers and logic - Franklin’s Anand Radhakrishnan

3 Likes

This seems more like a discussion on broad governance issue and quoting of quotes. Many greats have said many things and if you want, you will always have somebody’s quote to back your view point but not their returns.

Kitex: key issues as per me:

a) very quick signing of results by auditors. Usually they take time and ask questions, in kitex case it was way too quick for comfort.

b) Mr Sabu falling short of promises way too often. Not the first time.

c) recent capex announced, which wasn’t required till quarter back.

d) presence of promoter owned entity in same business.

On Prof Bakshi, I am aware he raised stake last quarter, but he could be wrong in assessment of management (not that he is). Everyone gets it wrong once in a while. Also, he mentioned this business way back when workers were dying in factories in India and Bangladesh, while this guy was offering proper work times, AC and better work conditions. This he considered as a strong point, as no buyer would want a disaster and labour issue especially for kids clothing.

Sadly I don’t have a quote from buffet or lynch or munger!

Had a small position, which I exited after the results.

6 Likes

Dear All

On Oct 3 2014, Prof published a teaching note in which he outlined his investment thesis on Kitex with clarity. You could revisit his thesis and compare it with the situation now to see if anything has changed and maybe post your views so that everyone can learn.

Teaching-Note-on-Unconventionality.pdf (269.6 KB)

3 Likes

It doesn’t hurt to take notice when a good value investor invests in a company. That doesn’t mean that we intend to blindly go buy the company at any price. It is probably the next best thing to insiders buying shares of their company. The very act of a good value investor buying is signalling that there is probably some value there. If our curiosity is piqued, we should definitely dive deeper and see for ourselves whether we should invest or not. Why would one person tell another person that this line of enquiry is futile or a waste of time?

Also, all these issues raised by several investors might turn out to be a problem after all but how certain are we that these issues raised are 100% true? What if this very suspicion will cause the shares to get more undervalued in a few months time? Would we still ignore if Kitex were to trade at Rs 200 in two months time because we think we shouldn’t trade on “borrowed conviction”?

I disagree with the view that shareholding pattern never “interferes” with business decisions of value investors. Don’t buybacks, insider buys affect shareholding pattern of a company? Don’t value investors take note of that? Don’t value investors like it when the CEO has a chunk of his wealth tied up in the company? Hasn’t Warren himself stated in his letters that more than 90% of of his wealth is in Berkshire? What would be the reason for him to state that if it didn’t matter? Don’t value investors invest in Berkshire anymore?

I wish we could stop using words like “arrogant” to describe the other member’s intention. It just doesn’t do this thread a world of good.

If we are wrong in questioning the reasoning of the investors who have raised the issues regarding kitex, then I hope that the senior VP members can correct us. I won’t engage in this line of thinking if we are going off on a tangent that doesn’t conform with the guidelines of Valupickr.

@Bheeshma, thank you for the link.

2 Likes

@bheeshma Agree with every word you have said. On this forum, I always see healthy engagement with high learning quotient. Ideas rot if they are not shared with others. That is the premise for a discussion and creation of knowledge. If we start thinking of ourselves as omniscient and all pervasive, then the concept of community learning would be a waste. I would learn from even the newest member on this forum (read anyone) if there is anything to be learnt, and would share my views with the most senior member (could be Professor himself) if I have something worthwhile to contribute. Glad to be a part of this august forum.

Meanwhile, are we forgetting that investors have made excellent money on this stock? A CAGR of 50% in last 5 years to be precise. Stocks which go up with such velocity have a tendency to correct by 50-70% from their highs (reasons could be plenty). But when we question the integrity of the management, we must keep in mind that its the same management behind the phenomenal growth of the company. Yes there are doubts on certain actions but imho they are not conclusive enough to change the business potential and my investment rationale (Its a personal opinion. Feel free to disagree). I would give the management some more time to get their house in order and match the expectations set. If however, the performance continues to dwindle in coming quarters, I would be revisiting my investment thesis.

Agree with the valid points raised by the community… Lets use this forum to share our thinking process and build upon them by collaborative thinking.

This forum is something i take pride to be part of as the amount of knowledge one can learn is immense. Lets all be open minded and discuss points in a friendly manner.

About Kitex, as i am holding onto it for quite some years, my perception about management is as below:

Mr. Sabu has created an exceptional business. His ideas and thought process have taken Kitex to where it is now. State of the art facilities with automation to improve efficiency. Labor management in textile industry is tough, but his idea of labor management speaks a thousand words about his futuristic thinking capability. Slowly and steadily moving into private labels and own brands after completely understanding the business is to be taken note of. The return on capital which the business has given over the past several years is not a joke. We have to understand every business from time to time faces challenges. It is only capable leaders with great understanding of industry who can keep their boats still floating. I would still be with Mr. Sabu and wait out for more quarters before taking any strong decisions.

Lets keep the healthy discussions flowing. That’s what this forum is all about.

Disc : invested and not a reccommendation.

2 Likes

Do not clutter the thread with irrelevant posts. Let the fundamental discussion on Kitex take the center stage.

6 Likes

While i totally respect your views, i beg to differ on point a and c.

a. Kitex has changed its auditors an year back and currently its audited by a highly reputed mid size audit firm by name Varma and Varma(this firm was the lead auditors for State Bank of India for the year ended 31 March 2016) - and have look at the business of the company -

- they are only into manufacture and sale of garments - which is among the least risky revenue and cost to audit.

- they have traditionally maintained a very low debtors and inventory balance which makes the process of audit even easier and less risky.

- Fixed assets are consistent year over year.

- The rest of the balance sheet elements are kept at a very low level.

- They have recognized Rs.8 Crore loss from associate entity in US(while they are burning cash here, considering these are initial years of operations in US- we have to give credit to management for recognizing what money they actually lost - auditors will have lesser questions to ask when the management is ready to recognize the losses incurred by the associate.).

To be honest i don’t think this a difficult financial statement for the auditors to give an opinion.

c. I remember that Mr. Sabu clearly explained the reason for for additional investments during Q3 con-call(i know it’s a little difficult to follow him during these conversations, but the best part about him is that he always know what he is talking about and for sure he is not faffing!!) - as an investor we sometime have to trust the management on what/where they want to invest its money - see, they know the business better than all of us put together.

I agree with the rest of your points

Thank you.

Best regards,

Antony

Disclaimer: Invested in Kitex

5 Likes

Interesting observation from the Annual Report of Kitex for the year ended 31 March 2017 - The Company has charged 6.1 Crore to other expenses as CSR expenses while the they are legally required to transfer only 2.6 Crore. I hope management looks into this aspect seriously and ensure that only legally required funds are used for CSR in the future. This excess transfer to CSR has negatively impacted the EPS for the full year by Rs. 0.70. Hope someone raise this question at the AGM and make the management aware of it. While its wonderful for Kitex to contribute towards social welfare, the management should also be aware that it is a pubic entity and they are holding fiduciary responsibilities in safeguarding the interest of its shareholders. Any over commitment to social welfare should be from the personal kitty of interested parties.

8 Likes

It is mentioned in this thread that the promoter is connected with local politics. I am wondering if the high CSR expenditure is driven by that connection.

2 Likes

Seems to be a case where the promoter is using company’s resources to further his political cause.

Politics is a dirty game in India and water can muddy very quickly.

The business is strong, but I am beginning to get skeptical if value will be created for shareholders owing to the promoter’s political ambitions.

I am invested and wondering if the Boiling Frog Syndrome is affecting me!

Running a business in Kerala is impossible without having a connection in Politics. I think, may be we are a little over judging the promoters here. I would like to keep a close watch.

Disc: Invested (insignificant %ge of portfolio)

1 Like

You have a valid counter point. I have a few contacts from Kerala and they mentioned the same point about how tough it is to run a company in Kerala owing to Labour issues and incumbent political ideology.

My concern about Kitex promoter is a possible lack of focus on running the business once politics takes center stage, if it does. His overstatement of future growth plans doesn’t bother me as much (some people like to boast). But, going forward will need to monitor his business decisions a little more critically to ensure no/minimal political linkage.

As of now, I continue to hold and will pull trigger based on management’s actions.

It may be worthwhile to go through the VP Q&A done with Kitex Management in 2014.

http://www.valuepickr.com/q-and-a/kitex-garments-management-qa-aug-2014/

Best

Bheeshma

3 Likes

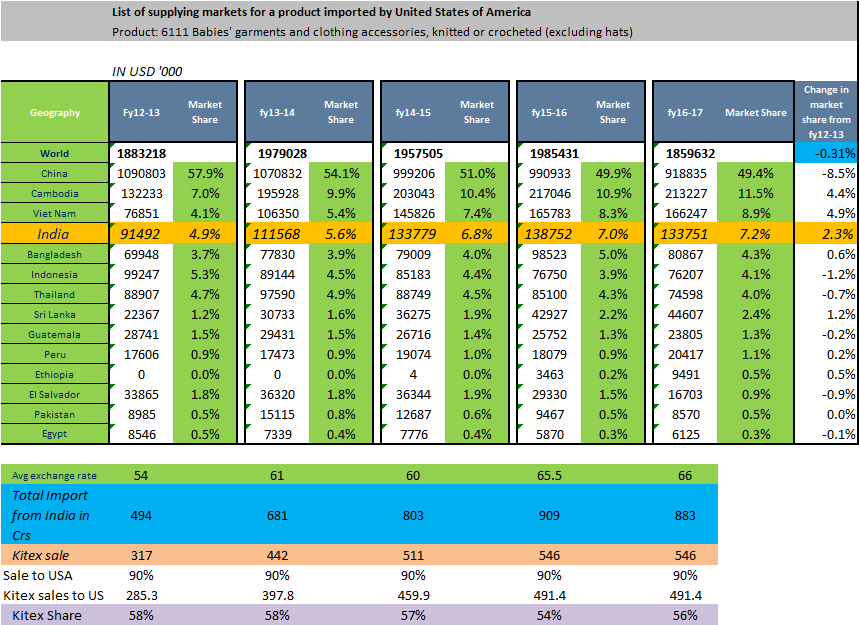

I have been doing some digging around to get a sense of the future growth prospects of the company (given the dramatic fall in share prices there is a case of it becoming more attractive). I have collected some facts and some of them don’t match with the information put out in the 2016AR.

Of particular note is this statement in its AR16

A casual reading of it would lead you to believe that Kitex has a 70% market share in all the imports of baby garments into US which of course is not true. I think a statement this important should be worded properly otherwise it comes across as a marketing gimmick. To me it certainly does. What they probably mean is that Kitex has 70% share in all the exports of baby garments to US from India ( more on this later). Given that that is what they mean it becomes important to understand the facts

The import of baby garments into US has remained flat in the last 5 years and has reduced in the last year

Kitex report mentions that birth rates have improved but one should also realise that it is the net addition of babies that matters. Just as babies are introduced into the world babies also move out of circulation as the grow. In any case that is not translating to an increase in demand for baby garments from the US. In fact there has been a major degrowth of 6% in the total value of imports compared to the last year.

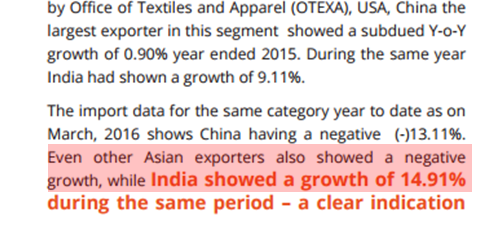

While Chinas share in total imports has reduced by 8.5% in the last 5 years it still remains a powerhouse accounting for ~50% of all imports to US.

China has been losing share ( as correctly pointed out in the Kitex AR) but it still dominates the import. India has a small share of 7.2% compared to 49.4% of China. This perspective is very important. Read in this context the positive feel communicated in the AR can quickly turn negative.

Indias share in imports has grown but the share of Vietnam and Cambodia has grown the fastest in the last 5 years and their market share is more than Indias.

Cambodia accounts for 11.5% and Vietnam accounts for 8.9% compared to Indias 7.2%. Cambodia has increased its share by 4.4% and Vietnam by 4.9% compared to Indias 2.3%. The biggest beneficiary of China losing share is not India its Vietnam and Cambodia. Bangladesh just has a share of 4.3% and its share has remained stable. So viewed in this context this statement in the AR is definitely not true in my opinion.

Kitex share is not 70% and its share has remained stable since the last 5 years

As per my calculation its share is somewhere b/w 54% to 58% ( refer to pasted sheet). This of course reiterates the leadership status of Kitex but It has remained like that in the last 5 years clearly indicating that customers are sticky but are unwilling to part with a greater share of business to Kitex. China losing share and a part of it coming to India is the main reason for the growth in Kitex sales along with weakening rupee. If you look at the period between fy12-13 & fy14-15 , the indian share increased the maximum from 4.9% to 6.8% which is also the period where Kitex sales skyrocketed in the shortest time possible and the rupee went from an avg of 54 in 12-13 to 65 in 15-16. The current scenario of a strengthening rupee, China share stabilizing and Vietnam/Cambodia gaining strength doesn’t invite a growth oriented future for Kitex.

The absolute limit to market size of baby garments to US from India is 900 cr ( at the current avg exchange rate) as things stand currently

Unless there is a dramatic improvement in the US imports of baby garments OR/AND China loses even more share OR/AND other Asian countries lose share or their shares remain stable OR/AND rupee starts weakening again, the theoretical limit to the baby garment industry is ~900cr of which Kitex accounts 546 crore.

So valuation wise, at worst Kitex may enter a phase of negative growth in the future or in the most optimistic scenario growth will happen but at a very benign rate. Assigning a growth rate of more than 5% to kitex would be irrational and very optimistic in my opinion UNLESS Kitex acquires a rival/moves into a different geography/expands its product portfolio/expands domestically etc

In sum, Kitex remains a great company with super cash flows but growth prospects are not encouraging unless Kitex expands its footprint in a major way

Views Invited

Bheeshma

32 Likes

Excellent information !! My bet on Kitex wouldn’t be from the growth of their sales which they claim they can grow inspite of other cheap and quality exporter available in other Asian country. I will bet on their direct selling through e-comm channels with their own brands.

Their sale price is less than 30% of what it get retailed in the US market. Now thats a big chunk of value which is lying at the table. Lets see how much they could capture that.

Rest growth in actual sales number and price competitiveness would be dud thing to look for in the global context.

2 Likes

To me the main attraction are its super cash flows. When a companies growth stalls but its cash flows remain intact it suddenly transitions from a growth buy to a value buy. Also i believe that the market cap of kitex is an indicator of the opportunity size that is prevalent for kitex. And as we all know the market cap has been falling.

Going forward i think cash is going to pile up as the business fundamentally has hit its growth limit and some time needs to pass before investors adjust to this new reality.

There are many companies with increasing cash balances but limited growth options. Cash cows require a different mgt mindset and the role of mgt in deploying this cash will be very critical in establishing a new investment thesis.

The margin of safety that was previously existing in the growth prospects will morph itself into the margin of safety in the growing free cash balances. Will being the operative word. There is,in my opinion, no margin of safety at current levels either from the growth perspective or the cash perspective.

A typical value buy profile is generally a 10 - 15 type PE company with zero debt, good dividend yield, nice cash flows and a stable topline peppered with a good quarter here & there. I think this is the profile that Kitex will be slotted in eventually.

Either ways i think one should wear multiple hats while looking at this fascinating company and its eccentric owner.

Best

Bheeshma

11 Likes

Thanks all for your inputs. This is very informative and good disciplined investment approach.

I actually have a few questions.

As with ecommerce, I think the company is concentrating on its US arm, especially given recently announced Capex. Any idea what exactly are they planning to do there? And is Kitex brand recognised there?

On the other point where we see Kitex as a cash cow, a few concerns float there. Assume nil growth, especially since inflation in US is low, how sustainable is the pricing in the long run. While I agree that we still have a long runway here, this will still mean PAT may decline slowly if company doesn’t hike prices (due to labour cost hikes). Even assuming stable PAT, one wouldn’t pay 20x earnings? Even if they payout all profits as dividends that will make a 5% yield Perpetual instrument. So I think assuming nil growth, prices should be tamed.

I have a specific question on capacity utilisation. Does any one have a rough estimate of their capacity as pieces per day. And their average utilisation. Would be helpful if we have KGL and KCL numbers separately. If there is some spare capacity then I think there will be a possibility of growth opportunity.

Discl invested at CMP due to recent correction

Hi Bheeshma,

Hope you are comparing Kitex with 0 -2 yrs baby Segment (Body Suits , etc ) . There are lot of companies who do much broader things within this space. As per last conf call closest competition is Jay jay Mills. There is sales is also growing .