Thanks Ayush for your time and effort

Thanks Ayush for taking the trouble to create detailed notes and sharing them with the community. Enjoyed going through them.

Wish more & more folks would do the same.

Positives:

1.Team US/Hiring decisions

Really good to see few key people joining. Ex-Gerber VP level person is a very senior person in the industry - so marketing challenge to top retailers in US is under control. Similarly the senior design person ex Levis/Gap tells us again that the Design challenge may be under control. Licencing “Lamaze” brand should take of the customer acceptance challenge too.

2.Product acceptance by existing Retail customers

If Gerber and ToysRus - the 2 biggest existing retail customers have accepted Lamaze products and placed orders, thats a good sign and confirmation of Mgmt’s claim that there really will not be any conflict of interest with existing retail customers (professional environment)

Its early days, but the zeal to make things happen in uncharted territory, hiring the few key people to propel the business solidly forward, product meeting acceptance - are all very good signs.

Concerns:

- Existing customers do seem to have a choice to walk away - unlike the earlier claims by the Management. Some have chosen not to come back, and reportedly some have. Management seems clear in its intent that they will not agree to discounts, price cuts demand from Customers.

Another friend who attended the AGM indicates that on the query about existing customer relationships not scaling - the company shared that the extent of cutbacks (in the face of Kitex not meeting discount/pricing demands) in some cases had been as severe as 80%, though some have come back with more business.

2.Inflexible attitude/misplaced(?) belief we-are-the-best/ nobody-can-be-like-us/ they-have-to-come-back - echo @ashwinidamani comment on the same

While the Management truly believes in this paradigm, the reality is “telling” otherwise. Gone is the earlier bluster of doubling capacity to 1.1 million pieces from existing 5.5 - instead the commentary has toned down to 60% growth in 3 years (not to forget this is factoring in Lamaze, which should actually have been the extra kicker). If you hear the Concalls, the capex plans also do not mirror the earlier ambitions. Contrast this with 100% plus augmentation of Capacity (already underway) by Jay Jay Mills, and 100% capacity expansion (completed) by First-Step.

One can sense this “attitude” is probably at the heart of slow growth of existing business. According to this friend, the Management let slip (in not so many words) it wants all customers to come to them and give them business at their terms - they do not want to go and actively seek growth from customers, as customers would then 'know" (the order-book situation?).

Contrary to Management claims of order-booking is not a problem now, and Lamaze business is anyways growing - all above would indicate, while Kitex is not able to scale up existing business at a decent clip, Competition is doing just that - Sourcing targets of Mothercare and Carter and others haven’t degrown, have they? Time to focus on this crucial aspect?

Disc: Invested; No transactions in last 30days

22 Likes

I am slowly coming to the conclusion (still work to be done/industry facts to be collected) - that my Investment Thesis for Kitex business has materially changed. Whether I am comfortable with the changed thesis - should be the correct way to think forward on this.

Earlier Thesis:

- Extremely efficient player in infant-wear with world-class facilities, led by a truly passionate, over-achieving entrepreneur

- With captive customers, track record on quality and timely delivery, and the manic focus on efficiency - business can easily achieve stated claim of doubling capacity from 5.5 Mn pieces to 1.1 Mn pieces - and become the No#1 Infant-wear manufacturer in the world

- Business can easily grow at 25% CAGR for next 3 years. It will become much stronger putting a lot of distance with the next competitor with half the capacity.

- Infant-wear is after-all a commodity business. But it will be really difficult for others to snatch away business from Kitex - as they are the most profitable - enjoying a 10% plus operating margin superiority over most competing players - because of the manic incremental focus on technology/efficiency/productivity and business scale of each customer

- The US business ambition - if it plays out well - is a great Optionality to have. Could lay the foundation for disproportionate future gains.

Changes (that we need to do more work on to establish):

- Competition is able to snatch away business - not because of any execution goof-up, but the inflexible attitude of Mgmt towards volume/pricing discount.

- If a business enjoys a 10% superiority on costs, why wouldn’t it be willing to pass on a couple of percentage points to the customers for significant scale-up in volumes. Isn’t this proving counter-productive. Instead of protecting the turf and racing away, competitive positioning may have significantly weakened.

- Some of the competition - like Jay Jay Mills and First-Step may already be at a scale - reaching or bettering KGL capacities

- Mgmt is looking at Lamaze business to fill in the shortfall in orders

Altered Thesis ( I am contemplating on)

RISKS of earlier thesis not getting achieved have significantly increased

- Existing business may only grow at 10-15% CAGR, for next 2-3 years?

- What is much easier to grow and scale - existing business where Mgmt has proven skills, OR the fledgling US retail business where everything has to be done from scratch?

- Only half of Lamaze business accrues to KGL - the other half goes to KCL, right?

- Instead of being the icing on the cake, unfortunately Lamaze business is being called on to fill in the shortfall. Too much focus on growing Lamaze business with an attendant couldn’t-care-less attitude to genuine demands of existing/new customers, can prove detrimental to continued success of this enterprise.

- Competitive position may have significantly weakened

It may well be that Lamaze business turns out to be an extra-ordinary success, and makes all above redundant by over-achieving all mentioned targets. Its possible, yes.

But as a Capital Allocator, do I think that the RISKS in the business/my investment thesis increased significantly? Probably yes.

To establish this further we need to come up with a fresh Infant-wear Industry Map

a) Buyers annual budgets b) Significant players, their capacities, and customers they are serving

Am meeting a senior industry person soon, so hope to update more on this front.

Request everyone invested/tracking KItex to also focus attention on this aspect, and get us some solid info/facts to do more diligence.

Disc: Invested; No transactions in last 30days

36 Likes

It was nice to revisit this thread to refresh memory - copying posts made in Sep 2014 - to get more folks focused on unearthing the current competitive picture

Donald Donald Francis Admin, Top ContributorSep '14

Guys,

We have been maintaining that Management commentary will need to be cross-checked. There can be more to the Story than is being put out. Some salient data points from my industry contact:

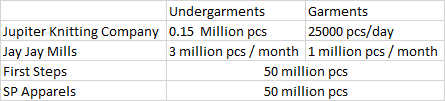

1). Atleast 7 players of comparable sizes to Kitex and supplying to common customers. Some are expanding in a big way too.

2). BEST Corp, SP Apparels, First Step, Jupiter Knitting, CMI, Jay Jay Mills, Kitex

3). First Step Bangalore has expanded recently and put up a new state-of-the-art facility near Bangalore

4). Quality being a big differentiator - NOT TRUE - too much of a drum is being beaten on the Quality front. Harping too much on the product. While it may be debatable that Kitex supplies fabric made of better quality yarn - that’s hardly the buying differentiator ever - as everyone meets the minimum standards needed. “Unnis-bees” ka difference doesn’t sway buyer order placement who are focused on profitability. At best it is a good selling point. Price and on-time delivery record sways buyer behaviour. Have you guys asked Vendors about their on-time delivery record?Ask about past 4 seasons - and you may get a better grip on the situation.

5). Atleast one of the big buyers mentioned by Kitex - sources 5x higher from BEST Corp and First-Step 2x higher than it sources from Kitex. All things being equal (read minimum specified quality), Price, On-time delivery record, and Relationship has more sway on the buyer order placement and scale-up from season to season

6). Almost all Buyers put a cap on max 30-40% exposure to a single vendor. It is safer for both parties. Some have expanded capacities in place now to scale up on relationships.

7). First-Step quality is like “Makkhan” - the exact words used. There is another player like Prime-Tex whose quality is the best - super premium - but his overheads are higher. Volumes for this particular vendor is at 65% of Kitex for that one player cited above.

8). Bangladesh is also scaling up in Infant-wear. Jay Jay Mills in particular is one audited facility (when quizzed about prevalent social ethical norms) as is Inter-Stop Bangladesh. Besides Bangladesh has the advantage of zero duty (LDP=0) even if say India could match competitive pricing

9). Baby Suit Realisation per Vendor : ~$1.1 on an average

10). Retail MRP in US is 3x average vendor realisation. However there are low-downs. On actuals, on an average there would be only a 20-40% mark-up on the vendor price depending on the player. Some like TESCO operate at lower markups but higher volumes.

Donald Donald Francis Admin, Top ContributorSep '14

http://www.bestcorp.in/products.html

http://www.s-p-apparels.com/about-us/

http://www.firststepsindia.com/infrastructure/

http://www.uk.crystal-martin.com/about-us.php

Please spend some time on these established manufacturers from India with significant infant wear presence. Lets collect more data-points for a more objective assessment than we have done so far

17 Likes

Wonderful write up Donald…I completely agree to your concerns…I agree to this that mgmt is much over confident.

Since I was also revisiting this counter after a long time…was trying to analyse the business with fresh frame of mind…what I thought was even after discounting all what was said by sabu…the business can be expected to grow at least at 12-15% CAGR…including the Lamaze and little star effect…They are doing all the correct things for their US expansion. And since all the negatives have been already priced in…the business expected to grow at 15% is available at a 20 PE…

But saying all this, I must factor in the competition impact…I need to re think on the existing business slow growth concern that you have highlighted mainly because the competition is heavily expanding…surprisingly SP apparels is going to come with an IPO in near future…It has already filed it with SEBI, waiting for approval…

Disc- not invested in last 6 months…was planning to re enter the counter, but I guess will have to do some more homework before I enter. Thanks lot Donald.

3 Likes

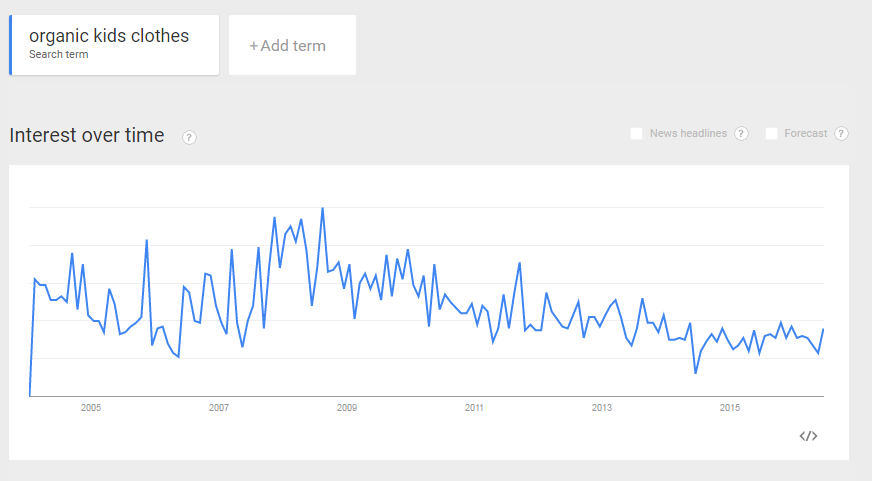

There is a lot of focus on Lamaze business, but when I check google trends, i do not see any growth in interest for organic kids clothes.

1 Like

Thanks for giving some directions to work on. Will get back with my inputs.

Meanwhile shouldnt we also factor in the optionalities of a merger.

genious piece of notes … well appreciated …

Mr. Sabu has indicated it on con-call and at AGM that the listing of KCL and then merger will be considered in about 2018/19.

1 Like

For those who attended the AGM, was there a mention about TPP and its implication to business?

Thanks Donald for the comprehensive inputs.

While data related to competitors, customers etc. can be gleaned independently, one key input may be more difficult to access:

What is the current customer profile of KCL?

What revenues / profits is KCL making as of today?

What is the fundamental reason Mr. Jacob is encouraging continued opacity - by deferring KCL listing and merger “for consideration” to 2018-2019?

Regards,

Disc: Exited several months ago. Stock on watch list.

2 Likes

This is from the CARE Ratings Report on Jay Jay Mills

As per FY 13 Results - they had a turnover of Rs. 572 Crores and a Net profit of 29 Crores

As per FY 14 Results - they had a turnover of Rs. 746 Crores and a Net profit of 28 Crores

As per FY 15 Results - they had a turnover of Rs. 977 Crores and a Net profit of 66 Crores

For HY 16 Results - they had a turnover of Rs. 671 Crores

So Atleast they are snatching away sales much much faster

However , Im not sure if this is a right comparision, but rating of Long Term Facilities of Jay Jay Mills is Care BBB+ , whereas Kitex is rated ICRA A+

Care also mentions that their rating for Jay Jay is constrained because of

a. Exposure to Forex Risks

b. Geographic Concentration of Revenues

c. Large Debt Funded Expansion Programs

JJ’s promoters has three sons each managing one country of Jay Jay (India, Bangladesh and Nepal)

a. JJ sources fabrics from India

b. processing is done in Srilanka and Bangladesh

6 Likes

From Crisil Report on Jupiter Knitting

- For FY 16 Turnover of Jupiter was 102 Crore , margins at 11%

- Has a rating of BB-

1 Like

Thinking about KCL and KGL issue and eventual Merger, is pretty tricky (for me)

As and when it happens, its a bonus - better not to factor that in, in any valuation case.

Because this is completely an unknown (timing, valuations, swap ratios).

As we all are aware, Initially the reason for starting a separate entity in the same business was stated as the Debt/Equity situation was perilous and no bank was willing to lend to KGL - it had no money to execute orders. Mgmt then stepped in and put in personal collateral (staked everything, as per Mgmt) for a fresh outfit - so that could execute customer orders. “They are like my right and left hands. I don’t differentiate between the two. When the time is right, we will merge the two entities”.

When will be the right time?

Mgmt answered that as and KCL scales to a certain size, that will get good valuations, etc. Couple of years down the line, if valuations are right, was the tentative answer.

There were many senior folks who were not comfortable at this apparent conflict of interest situation. But we deemed it okay, given the circumstances under which the company was started, and the promoters need to make good on high risks taken. We know some seniors continued to stay away for just this reason - reasoning, that the “temptation” to massage/manage numbers in either direction (as the situation demands) can be very high. And one could not vouch for sure on what the Mgmt may or may not do, in future.

Subsequently, US operations structured as a 50:50 JV between KCL and KGL came as a complete surprise. It implied that whatever success/upsides came out of the US operations may not be enough to move the needle sufficiently for KGL (a friend shared, thus) as half would go to KCL.

If I have to speak for myself, I did not find that a fair structure for minority shareholders.

The jury is probably out on that (Many may not agree with me). I only go back to my Guru’s words on the same

…Once any businessman takes other people’s money- equity and debt, the meter starts, returns + accountability. Is he enriching himself at the cost of his financiers?

We all are looking out for promoters who can balance their ‘hunger’ with a sense of trusteeship of all resources available to them…

11 Likes

That’s a pertinent question.

And the answer should be obvious, isn’t it?

To get KCL to a stage that gets it as good a valuation as KGL, on listing. It should get viewed as an equal not the kid brother. Remember the Mgmt views them as equal - left & right hand.

I think it is safe to assume KCL has equally good customer base and assets as KGL.

KGL has the fabric processing plant - that’s extra. But then the ultra modern plant that you see and go ooh aah over, belongs to KCL. KGL plant is the older one (@ayushmit - please correct me, if that’s wrong)

KCL P&L BS details should be available from MCA website. Think others have shared before

1 Like

Donald,

I share your concerns on KCL and KGL - w.r.t. your response to Ashwini yesterday.

I however, respectfully disgaree with your response to me, the answer is in no way obvious, and managements statements should not be taken at face value.

Note that as per @ayushmit notes, Jacob’s inconsistencies continue.

At one point in the notes Jacob claims they aim to grow at “20%+” per year, whereas at another, he says turnover will grow 60% after 3 years (less than 17% CAGR).

One way to interprete this data could be that Jacob intends for Kitex as a group (KCL + KGL) to grow topline at 20%+ annually, but KGL will only grow at best at 16 - 17% CAGR so that he can shore up KCL performance. However, all “interpretations” are fantasies. (It could be that I am assigning too much meaning to the divergence due to the past historic lapses - Mr. Jacob may just have run a simple counter of 20 x 3 = and announced a 60% growth estimate.)

Management currently states KGL and KCL will eventually be “considered for merger” at some point - maybe 3 years from now.

To my mind it is even more important to understand KCL operations and numbers accurately.

- What is the Client profile of KCL

- What is the topline and bottomline growth for past 3 years of KCL

- It is also important to merge both results and look at the consolidated revenue and profit picture of both entities.

As an aside:

- Are auditors of KCL books / CFO - same as KGL?

- Are returns of KCL being filed with the same inconsistency as KGL?

Would be really good if someone could put up KCL P&L and B/S for the past 2 to 3 years.

Best regards,

1 Like

![]()

Thanks Aniket for your views. Not sure I have caught your main objection? If you have a different slant, please persist.

I am actually batting on your side. You didn’t catch the irony!!

If I am 100% owner of an unlisted entity and majority shareholder in listed entity, and I intend to list the unlisted entity down the line at a good valuation - what am I most likely to do?

Wouldn’t I make sure that the unlisted entity jogs along equally well? - in the run up to the listing.

At the same time because of the imperatives of the listed entity (oversight by other shareholders) - there remains scope of numbers being played up on one side.

if I buy that argument, then I wouldn’t lay much stress on dissecting KCL numbers, and the why’s and the how’s - unless the evidence shows that the unlisted entity is being blatantly beefed up - which from the numbers we know isn’t the case. (the Mgmt too knows that P&L & BS filed at MCA are open to public ![]() )

)

I would be bothered about whats being put up on the listed entity - and question the future of that entity and slightly discount Mgmt claims of putting the best customers & most profitable business in only KGL’s lap.

{Given the listing plans, I would hazard the game plan will be to - at an appropriate time - reveal that hey KCL has transformed into this lovely swan, that IPO investors would want to see (from if somewhat ugly duckling picture we may be presented today)}.

From a Numbers/Valuation/Allocation perspective, I wouldn’t do that

From a competitive positioning map of the industry, yes combined profile is what should be looked at.

Hope that helps.

2 Likes

Thanks for the clarification!

All clear, we are indeed on the same page

Take your point regarding KCL.

I do continue to feel it should be a good idea to check how the consolidated numbers are developing and evolve over the coming years.

All the best!

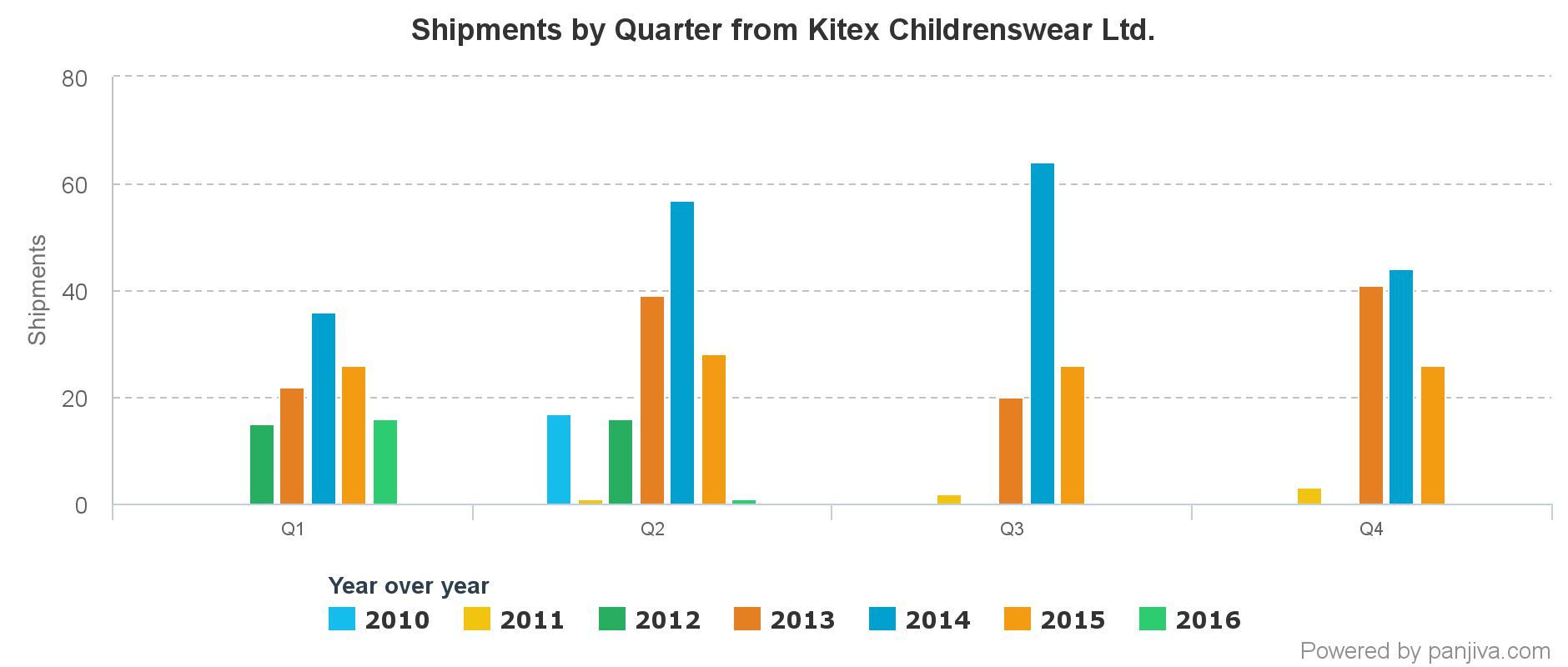

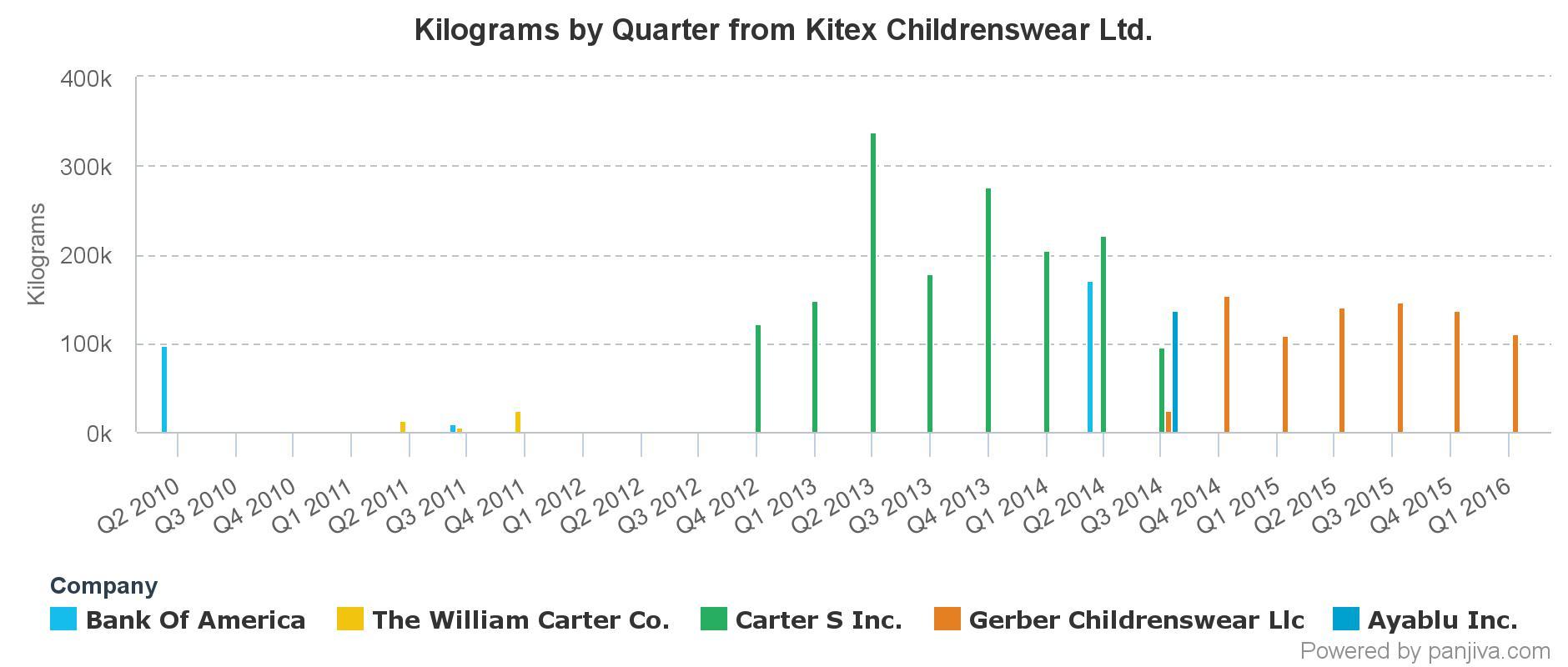

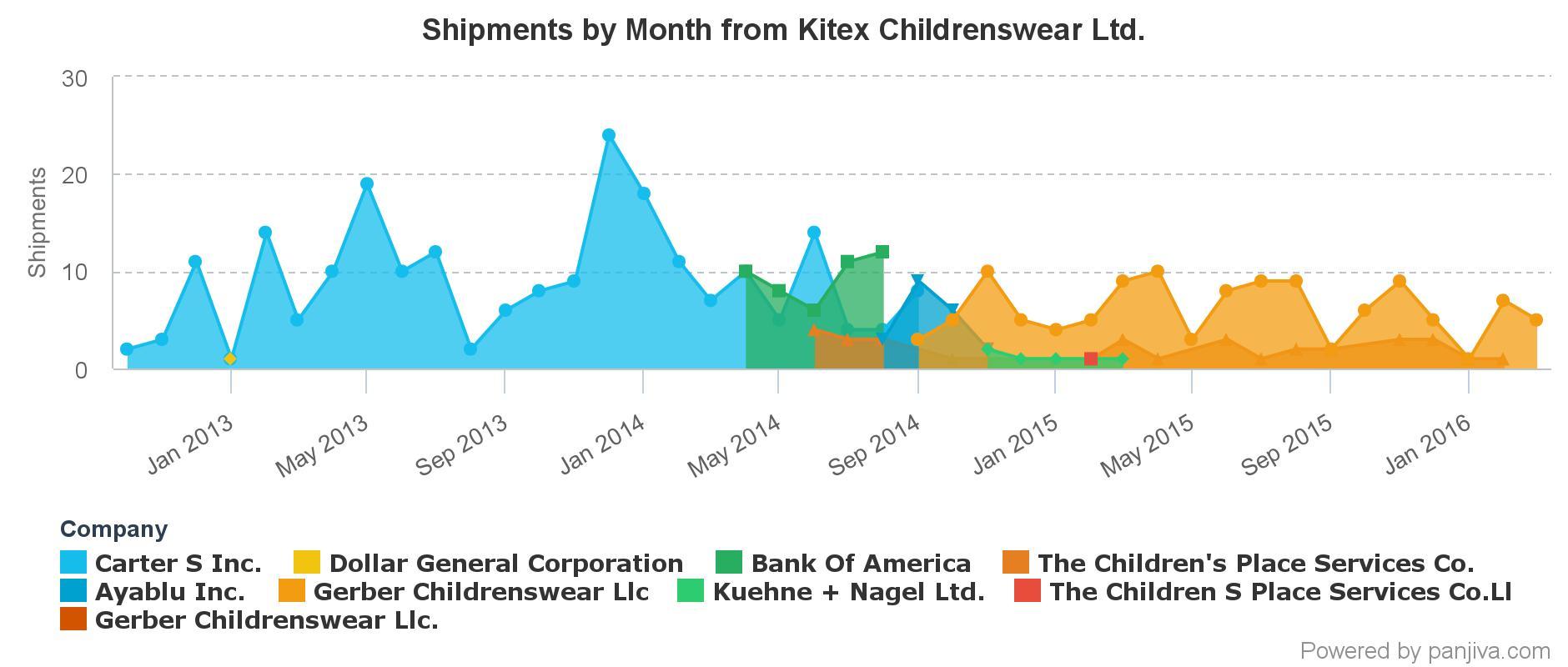

Hello Donald,

I was able to find a good source for answering the 2nd part of the exercise.

This is mainly for US imports.

This is a paid site, but provides a 7 day free trial, with the following restrictions -

One gets to visit only 5 company profiles and export the shipment search results for 5 companies.

So, one has to be prudent in how they use. Off course, if one can afford and feel they do get value addition they can pay for the $99/mth basic plan… ![]()

Anyways, as @Value_Seeker had rightly requested for more clarity on KCL customer base, i thought i would cover the low-hanging fruit.

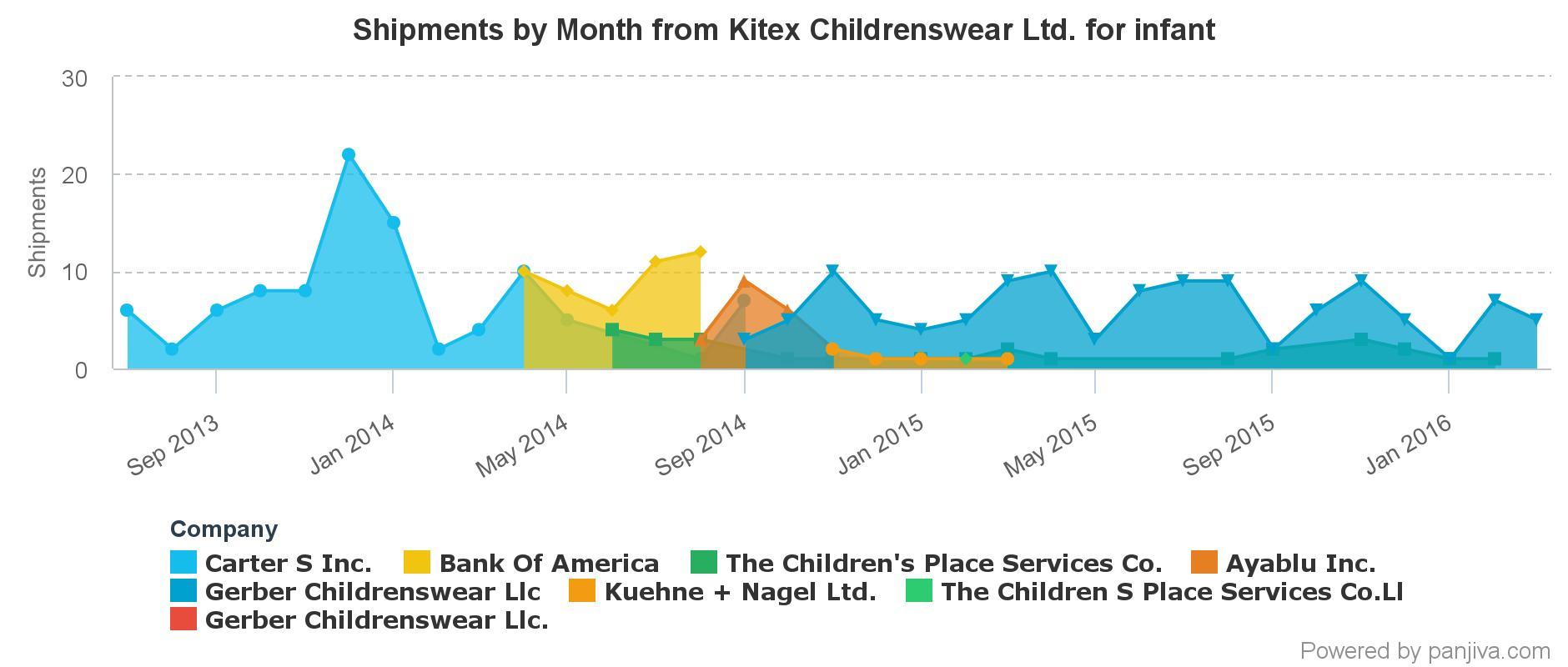

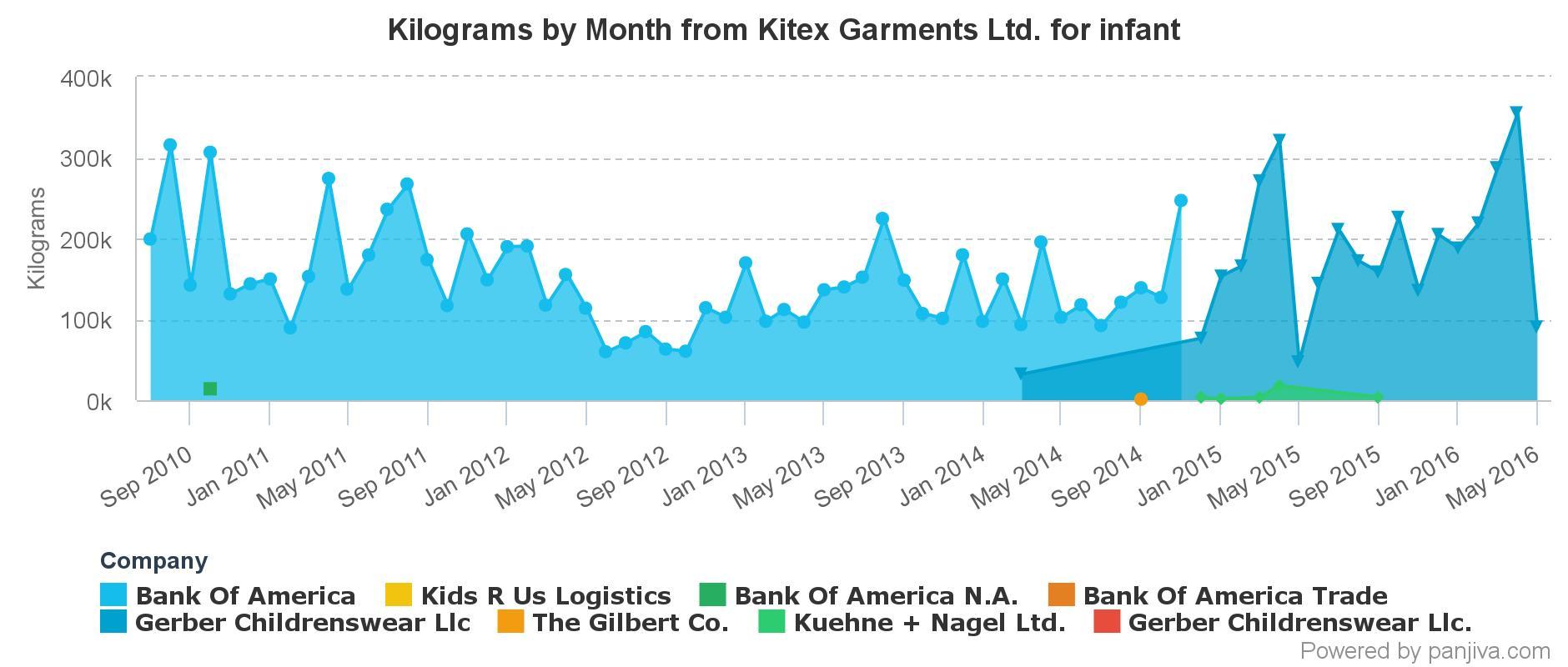

After adding the Infant filter

KGL

Couple of observations from above:

- Big-bang shipments from Q3CY10 where the scorching pace is maintained till Q3CY11.

- Similar growth rates resumed from Q4CY14 till Q2CY16.

After adding the filter for infant, we find that:

- Jockey is not available, as it should rightly be so.

Other observations:

- In both the charts, we find Fruit of the Loom and Carter’s is missing for KGL.

- Also, the new client Children’s Place seems to be catered to by KCL, as was Carter’s in 2013-14.

- Mystifying why Bank of America is listed as client from 2010-13. But it could explain for the missing Fruit of Loom data.

- Mothercare data is not available with panjiva portal.

- Kohl’s does not seem to have received any shipment yet from either KCL/KGL. (TBC)

Below excel contains the last 2 YTD data for both KCL and KGL.

Kitex Exports to US_Last 2 years.xlsx (95.5 KB)

Overall it looks a good source and can be used to validate the exports for other textile co.s and US exporting firms.

Best Corp does not seem to have any infant related shipments.

On Capacity of Players - http://www.tea-india.org/jayjaymills

From DRHP of SP Apparels: - http://www.sebi.gov.in/cms/sebi_data/attachdocs/1451449620283.pdf

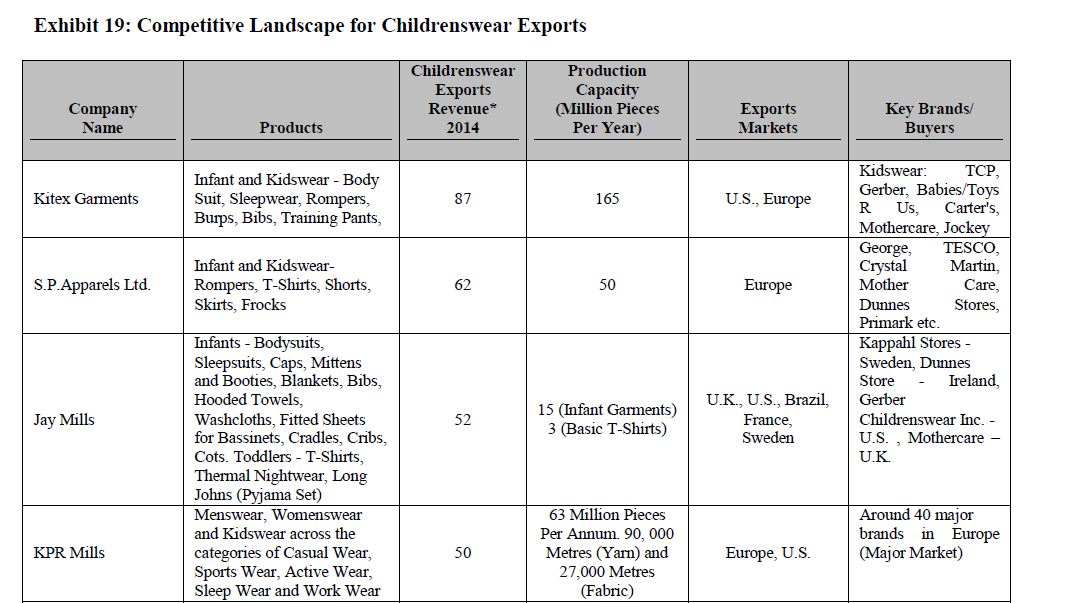

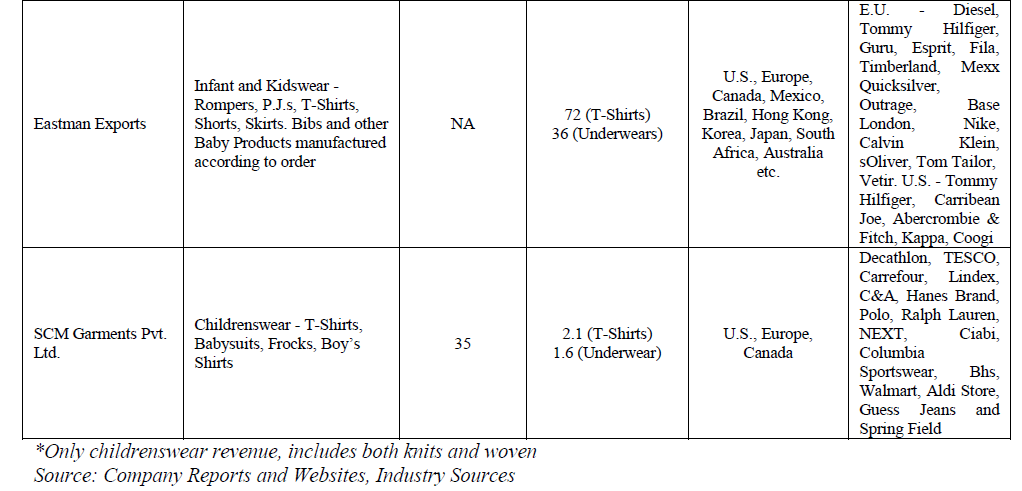

Key Players in Childrenswear Exports: Both Indian and international manufacturers compete in the exports market for childrenswear. Some of the key international exporters include Wingloo of China, Gimmel of Singapore, Kitex Garments and S.P. Apparels of India, Urmi Group, Divine Group, Textown etc. of Bangladesh. Wingloo has a production capacity of 225 million pieces per annum while the production capacity of Gimmel is 195 million pieces per annum (Source: Industry Reports). India based Kitex Garments and S.P. Apparels have production capacity of 165 million pieces and 50 million pieces respectively. Urmi Group of Bangladesh has a production capacity of 22 million pieces per annum and around 15% of the group’s exports revenue comes from childrenswear. Divine group has a production capacity of 18 million pieces per annum.

Kitex Garments and S.P. Apparels are leading childrenswear exporters of India: Kitex Garments is the largest childrenswear exporter of India followed by S.P. Apparels. The estimated share of S.P. Apparels in India’s knit childrenswear exports for the age group 0 to 8 years was around 8.5% in terms of value. Kitex Garments and S.P. Apparels are also the leading childrenswear manufacturers of India. The other key childrenswear exporters are: Jay Mills, Eastman Exports, SCM Garments, and KPR Mills. Product portfolios, production capacities, key markets and clients of these competitors are provided in Exhibit 19.

31 Likes

Thanks a lot Vishnu

Taking time to digest. This gives us a flavour of things.

At the same time would caution everyone not to take only this as the complete picture

for some reason, there are gaps

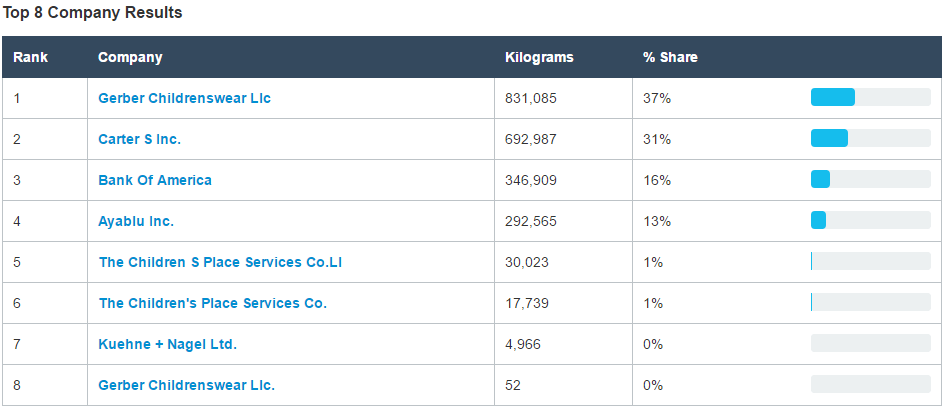

e.g. no Toys R Us share in KGL whereas they are the 2nd biggest customer probably at the moment with some $24Mn plus sales attributed to them

-

- it could be that the Bank of America imports are the ones routed to ToysRUs

1 Like