why do you think so Santosh. Please justify the cash issue. Please do share your views or any such experience witnessed by you in past. It will help us. Thanks.

Hi Santosh,

I have always found the cash issue to be a relevant question. Especially in the light of Mgmt’s response. I don’t think any of us would mind them holding onto cash provided a logical justification for the same is given.

I would personally write to them to get an answer on the pledge issue as well. I was surprised to see that questions about the pledge were not raised along with the cash issue. 'Coz of this cash issue I would like to understand that for what purpose are the funds against the pledge going to be utilsed for. I don’t want the pledge money to land up as the USD converted money in the accounts or to be utilised to shore up valuations of the pvt. entity (maybe thinking too much; but none the less I find cash issue to be valid and mgmt. justification given unsatisfactory).

Regards.

Its not even over analysis but hyper analysis. Same points, same arguments and clearly this thread is on path of getting closed again!!

My points:

-

Cash Issue

Yes, timing the exchange rate is extremely difficult. It seems management is wasting time trying to find the right rate to transfer. However, those who think that they should just transfer are also guilty of the same crime which is wasting their own precious time. If if seems so obvious that any USD should be converted to INR because of interest differential, your obviousness contradicts a host of global fund managers head on. Everyone in the world today wants to just buy USD and sell all other currencies including high yielding emerging market once. Interest rate parity is what should be considered and not the interest rate differential. Based on interest rate parity, the rate differential should be compensated by currency movements in long run. -

Merger

I think this is the best move by the management to get KCL listed first. As they said, any valuations given to KCL would have been treated as cheating to minority shareholders unless it was free of cost. Best to let market discover it.Other way to think about this is trust should be mutual. Management would probably have given better then fair valuations to the minority shareholders, but because people have started questioning their every small move, they stopped trusting the market and have decided to list it focusing more on transparency ( intangible benefit) than giving a tangible benefit. To me, (with my presumption that management is brilliant), this has been a negative news today and the benefits would go to management as well as the KCL Ipo applicants. -

Growth

One thing which is not clear is whether the guidance is to double volumes or the value in next 3-4 years. I thought it was to double the production, which translates to higher sales growth and margin growth if branded business is successful. But today, they mentioned 525 crores getting doubled to 1050 which seems a tab bit lower growth for the company trading at slightly richer valuations.And yes, I too feel the valuations are bit richer. -

Corp Governance

With a history of growing sales by approx 5 times, profits by approx 20 times and dividends by 10 times in last 10 years without raising a Rupee from the market, I do not have reasons to doubt management integrity. Just that the management is not very polished, and gets carried away by the analysts who try to extract too much information. To me transparency is good, but it seems there would be lesser questions on corporate governance if they stopped disclosing or explaining things… -

Some Fun

Just to give something to discuss for the Kitex’s critics. How about a conspiracy theory that they have cooked all the books for so many years and given the dividends etc. to make KCL ipo successful. There was no ENY advice, no three alternatives, the end goal was always KCL listing!!

Admin: Sorry for the taunt, could not resist myself after reading so many repetitive posts. No intention of being disrespectful to the points raised by anyone, but to the fact that same points are being discussed again and again.

Disclosure: Invested less then 5% of portfolio.

9 Likes

There is no harm in dissecting an issue and discussing if it brings out better clarity which is what VP is known for. Here people have real money at stake and people are not playing paper cricket. Truth will come out only through proactive analysis.

If the management does NOT reply to concerns in a straight forward manner there bound to be questions asked and repeatedly.

When management knows that investor community is uneasy and if they are not doing anything wrong, what stops them in clarifying their position in a crystal clear manner -

- We have cash of X amount in Y Bank with Z a/c number (if can be disclosed) and we are hoarding this cash because of W, U, V reasons. If W, U,V are not logical then investors will take appropriate decision to be part of the business or not though equity stake.

Please don’t taunt as real money is at stake here. Some could have made this as a part of core holding and IF there is any issue exiting will be difficult and could lead to financial loss.

I absolutely have no stake here, so please don’t misunderstand my post. Even MPS has money of 178 crore and management AND investors know exactly why that much cash is there. People are not over analysing the cash with MPS right? There is clarity in MPS and that makes holding the stock comfortable. So when so many people are analysing, then there is some reason to it. Only in hindsight we can tell if this analysis was hyper or lower. I hold MPS. Sorry if I hurt any sentiments here.

Moderators: Delete the post if you felt this is over the board.

7 Likes

Hi Gaurav,

I agree with you on all point except Cash Issue. I have used all other points mentioned by you and some other points not mentioned by you as a counter balance against the cash issue and hence I have remained invested (as I said in my post above that i give mgmt. the benefit of doubt).

Your Interest rate point would have been valid if it was a conversion on the basis of prevalent interest rates in both countries. In this case however the comparison is between cost of funds (domestic interest payments on Loans) Vs the advantage of converting at a better conversion rate. hence I don’t think the example provided by you is valid. It would have been valid if one wants to convert to take benefit by investing the converted money into say a govt. bond. Going by the invesment mgr. logic the same investment mgrs. also withdraw money when the interest rates in US go up. In short I don’t think your example here is valid as the cost of holding onto this funds (domestic interest payments) is higher Vs. the benefits of converting it after another 3% upmove.

I have replied only 'coz I find the interest rate logic given above as flawed in this scenario.

I agree that same point shouldn’t be repeatedly discussed, but at the same time I think one should reserve the right to criticize a mgmt. if the response provided is not adequate.

With all due respect.

Regards.

Hi Richdreamz

I am perfectly interested in serious discussion and am able to digest discussion on most other threads. It is clear that management does not want to disclose the information in the manner ‘MPS’ does. So if one is uncomfortable about this point, he has a choice to avoid buying Kitex or to sell whatever he/she has. That would be a prudent decision and a more serious one than showing seriousness on a forum by writing something that doesnt add value anymore.

And if this problem is because one is negative but is unable to sell his holding as share prices have declined, it makes even more sense for him to further stop being negative. No harm trying to get more information from company and taking decision accordingly.

My problem is with people who want to do ‘‘class participation’’ 'for sake of it or with people who want to spread negative news and the real goal is to finally buy on panic.

4 Likes

Cash issue indicating corporate governance problem and cooked books is different from Cash issue indicating lack of financial understanding/ intelligence. I can answer the second one.

Based on Interest rate parity

INR Risk free return = USD Risk Free return + USD Appreciation + USD Risk Premium

They are taking Four way disadvantage due to which the issue looks overblown

- They have INR loans which is higher rate than INR risk free return

- They havent invested USD in govt bonds ( not sure, but seems so)

- INR hasnt depreciated last year. This is just in hindsight mainly because of Oil/Modi/Fed.

- They are in a way paying risk premium for being invested in a safe haven USD

Yes, the arrangement is not optimal, but this is true with many companies.Apple was criticized for many years as well as Infosys is still criticized for not being efficient in cash management.

Sorry for 3 posts in quick time, no intention of further carrying out as I have uttered all information i have on the subject

1 Like

Hi Abhishek,

Please go through this link for the latest on TPP…

This regulation is far from being implemented and there is a lot of opposition…Now going by what was said in the concall I understand that US infant wear is a multi-billion dollar opportunity and I feel that the size of the pie is large enough for Kitex to have it’s own share.

Yes true…Also if even it gets the accord - I read some lines in the article where the whole scheme developed is I think to compete with the Chinese low cost products. Keeping this in mind and our relations with the US and other countries in the world (thanks to Mr. Modi) - It will be easy for India to be a part of this TPP. Assuming we are a part of the TPP and China is not - we as well as Gimell (singapore) will have an advantage over China’s Wingloo…

This is all long term - 2-4 years…But this can be great for Kitex.

Market :

The US infant wear category is a niche market with a market size of about USD20b

with high entry barriers. As compared to India, consumption wise it is 10-15 times more in US. People will manage with the same dress for longer period in India, but in US they change once in two weeks or so. Global Market is much more . Kitex caters to 90% US and 10% ROW.

Major Clients are Carters ( commands 20% of US Mkt), Gerber, Mothercare,Jockey and Toys R US. Revenue distribution among these people is more or less the same. In addition, they are approved by NASA which speaks about the quality and safety of the infant wear. Here , one mistake the whole market is wiped out for KITEX.

Birthrate in US: http://www.npr.org/sections/thetwo-way/2015/06/17/415227138/baby-bump-u-s-birth-rate-rises

http://www.wsj.com/articles/u-s-birthrate-hits-turning-point-1434513662

Production :

80 lines @ 5500 produces 4.4 lacs per day or 13.2 mln per month. Adding another 64 lines by 2018 which will make 24 mln per month. ( Mgmt claims 33 mln per month). Fabric proceessed will rise from present 48 tons per day to 1440 tons per day.

Now about Gimmill or Ramatex ( everywhere it is said Gimmell). Start from Raw Cotton unlike Kitex which I think start from fabric or knitting. Please somebody help me in getting this right for KITEX from fabric stage or whatever stage , the entire process. I think they don’t do any spinning ( no mention of spinning mills anywhere). What is there capability in every stage from Knitting. I have read robots but we need to see the use of technology and software at every stage as it is very labour intensive.

Gimmell have two spinning and fabric facilities under the Ramatex name. These mills are located in Malaysia and China. The combined production of both facilities produces 5 million kgs of fabric per month. From these facilities the fabric is sent to the apparel manufacturing facilities located in Cambodia, China, Indonesia, Malaysia and also Singapore. The combined production of these facilities is 10.5 millions units per month.

Gimmill have factories in Malaysia, Indonesia, Cambodia and China.

3 factories in China:

Kiwi China – 3 million units per month

Ramatex Industrial China – 800,000 units per month

Ramatex Apparel China – 800,000 units per month

Ramatex / Gimmill Malaysia (Yarn, knit fabrics prod 1.3 mil. units/month)

Tai Wah (Gimmill) Malaysia (Knitwear - 800,000 units per month)

Tai Wah Gimmill Indonesia (Knit apparel - 500,000 units / month)

Berry Cambodia (Knit apparel - 2 million units / month)

Violet Cambodia (Knit apparel - 2.6 millions units / month)

Gimmell Singapore could not get as it looks confidential.

Customers:

US & Canada: Carters, Osh Kosh, Nike, Target, Aeropostlale, Gap, Old Navy, Macys, Under Armour, Sears, K-Mart .In the EU: Fruit of the Loom, H&M, Next, Nike, Matalan, Under Armour, B&C.In Japan: Nike, H&M & Uniqlo

Gimmill is not specialized in infant wear like Kitex . They are also into Mens , Womens and Children. Infant wear is how much , we don’t kow.

Compare the capacities and draw conclusion whether KITEX has a clear game plan. If KITEX can displace Gimmil, it is easy to displace Wingloo as the space between Wingloo and Gimmill is not much. I think it is about 1 lac pieces per day.

For 2004, Gimmill total turnover is USD 300 mln, 30000 people for the entire operation starting from raw cotton.

Other strong points:

- In 2007 d/e ratio 5:1. What is the d/e now. Lets also see what is the d/e for both KGL and KCL put together.

- Labour is about 8000 and more than 50% are women. Such a labour intensive unit, no issues on account of labour or trade union till today. That too in Kerala which is not a business friendly state.

- Kitex is now trying to eliminate middle men and sell directly to Walmart/e-com thereby improving margins. It is also starting a new brand which we can ignore as it is a long drawn process. This is also a risk as the clients are well known and established ( I think Carter is more than 100 years old). I hope it does not upset the apple cart. Only time can tell this. Whereas Gimmell is just tagging along with Nike, Carter’s, etc. Management should have thought about this.

- P/e 5 year average is about 7 and 10 year average is about 5 until 2014 where it was re rated . Hence, guys who have re rated and bought the stock should have done enough home work.

In terms valuation, if I take 25 times EPS FY 16 24.89, it comes to 625 and this ignores the future plans like listing KCL, brand, capacity expansion. Technically, it has a strong support around Rs 700/- which I said in earlier post (study the price action after this post).

Rgds,

8 Likes

As per World Bank, 0-14 population in USA 66 mln. Just to give idea of the market size. No data on 0-2 or 0-5.

Rgds

I think India decided not to be a part of TPP due to certain conditions around IP related issues. I remeber reading this somewhere.

Regards.

Kitex promoted twenty20 party wrests control of Kizhakkambalam panchayat from Congress party who were against the company especially in environment issues. They won 13 seats out of 19

This report says 12 out of 19 http://www.thenewsminute.com/article/real-story-kerala-local-polls-how-private-company-won-panchayat-35777

I take this positively…the losing party is always going to spread news which can help them gain some votes by confusing people whom to choose…this is what rahul and Sonia Gandhi have been coming doing…i feel mgmt is positive and I feel impressed…salute to Mr. Sabu M Jacob for doing this…

interesting article on kitex http://indianexpress.com/article/india/india-news-india/kerala-civic-polls-how-a-company-won-a-panchayat/

Outlook article…

Can anyone share some thoughts on …how exactly the announcement of interest subsidy of 3% to export units wef 1/4/2015 for 5 years will benefit Kitex ?

No impact on kitex…kitex is not msme in first place…investment in plant and machinery is more than 10crores…

Jay Jay mills is also not a msme…jay jay mills exports the rest of the demand…

But a nice move by govt.

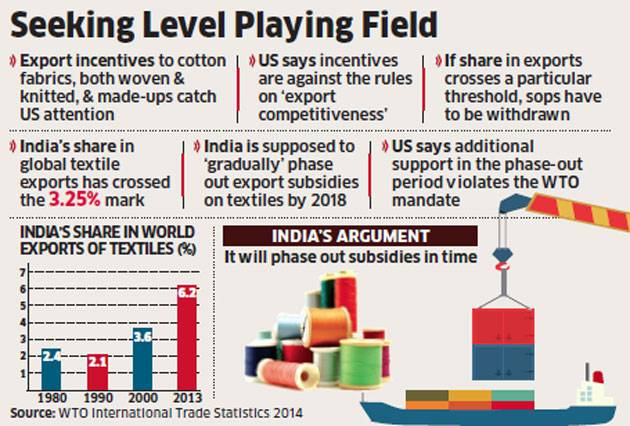

US opposes India’s latest round of incentives to boost textile exports

By ET Bureau | 20 Nov, 2015, 04.00AM ISTPost a Comment

NEW DELHI: The United States has opposed India’s latest round of incentives to provide a fillip to exports, alleging violation of a global trade rule for export competitiveness in textiles.

Commerce department officials said the US raised this issue more than a week ago, after India increased support for exports of several products including textiles while expanding the scope of the Merchandise Exports from India Scheme (MEIS) on October 30.

The government included exports of cotton fabrics, both woven and knitted, and made-ups to leading markets including African countries under the MEIS. Under the World Trade Organisation’s agreement on subsidies and countervailing measures, when the export share of a developing country with per capita income below $1,000 a year touches 3.25% in any product category for two consecutive calendar years it is deemed to have gained “export competitiveness”.

US opposes India’s latest round of incentives to boost textile exports

Such a country is then required to phase out export subsidies for the items for eight years from the second year of breach. The WTO mandates developing countries to phase out the export subsidies within the eight-year period, preferably in a progressive manner. The WTO had in 2010 asked India to consider phasing out the subsidies for textiles and clothing.

“However, a developing country member shall not increase the level of its export subsidies, and shall eliminate them within a period shorter…when the use of such export subsidies is inconsistent with its development needs,” the agreement says.

The US has flagged the issue of export competitiveness in textiles and said that India cannot give additional subsidy during the phase-out period, said an official, requesting not to be identified. Another official, in the Cotton Textiles Export Promotion Council, said India has crossed the export limit and the government is aware of this but the market is moving slow.

“As for the removal of subsidies, we can either gradually phase them out or immediately stop them in 2018 on a pre-decided date,” he said.

he government included exports of cotton fabrics, both woven and knitted, and made-ups to leading markets including African countries under the MEIS.

Read more at:

1 Like