Any update on the Singapore case since March? Also, have the Chinese competitors started manufacturing again? Any news?

Big news and a windfall gain for Kiri as had been anticipated. Now it needs to be seen how and when do they value DyeStar and how much will accrue to Kiri.

2 Likes

I don’t remember the exact numbers but if my memory serves me right, even at prudent valuation, the gain from stake sale will be more than the market cap of Kiri. Also interesting is that the Company has already repaid almost 600 of the 780cr of borrowing over the last 4 years. The profits have been rising steadily and the current P/E ratio is the lowest in the industry.

HDFC, in its report dated August 2017, notes:

KIL in its consolidated books shows a sum of Rs.702.4 Crs receivable on account of investment in the Dystar JV (mainly representing its share in the past profits calculated on conservative basis). Even If KIL does not succeed to get its stake liquidated this is the bare minimum receivable by it from the JV.

This is the share of profits which is over and above the value of the stake.

1 Like

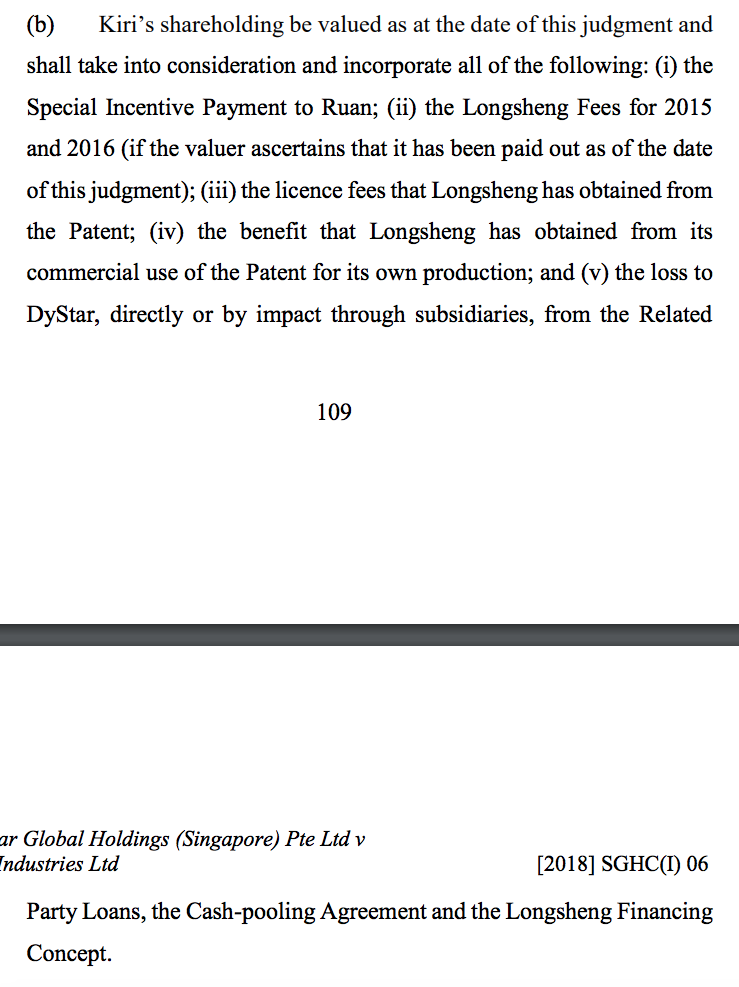

BSE filing by the company giving the gist of case verdict in Singapore high court

The judgement makes for interesting reading.

If Kiri has to sell its Dystar holdings of 38%, only revenues from KIL and LKCIL will remain going forward. This means that Kiri has to be valued for its profits of KIL at 100 Cr and LKCIL with profits of 24 Cr. At a P/E of 10, that’s about 1240 Cr.

Now Dystar has made profits of 230 Cr. At 10 P/E that’s about 2300 Cr of which Kiri’s 38% should be Rs.874 Cr. So at a conservative valuation Kiri should be about 2100 Cr (currently at a discount).

But the interesting thing in the verdict is this.

If these are written back to Dystar, its valuation should be higher and my conservative valuation might be too conservative. Kiri already trades at a discount to its peers. If the valuation is done by the court, going by the language of the verdict which is strongly in favour of Kiri, I suspect Dystar might receive a healthy valuation and Kiri consequently could benefit well. There is also the Euro 1.7 million and SGD 445000 or so which Kiri will have to pay back but this overall should be around 20 Cr INR so shouldn’t be bad considering what Kiri will receive in return for Dystar stake.

Has anyone else tried to value what Dystar stake might be worth and how long it might take? Considering this is Singapore and the way the hearing and judgement and the clarity in the verdict, I think this may not drag for too long like in Indian courts.

Disc: Curious and Interested

5 Likes

You have miscalculated Dystar’s valuation in your post above. 230 cr is Kiri’s share of Dystar’s profit which is roughly 40% of total profit already. You are again taking 40% of this value which is incorrect so instead it should be 230 * 10 = 2300 cr +1240 cr = 3500 cr approx.

So Kiri is quite undervalued even by conservative estimates. Now what promotors decide to do with this windfall once they get it? Would they share it with minority shareholders?

I think that is the question which will drive Kiri’s share price further.

5 Likes

Definitely, I was coming to this. Kiri has little debt to repay so what will they do with this gain? With the Dystar experience, will they want to try another global takeover? Or could they invest in some pollution controlling technology which has been the talk of the town for dye and chemical industry, especially in China which controls significant global market.

2 Likes

At current levels, around 4-5 P/E, with small debt, RoE at 35% and RoCE at 28%, 3 year profit growth at 90%, it looks like there is enough margin of safety, considering the DyStar stake and case verdict in favour. I see good tailwinds in the dyes/dye intermediates sector. Other than the question that’s hanging over what the management will do with the large cash from DyStar stake, are there other concerns? I personally don’t think this cyclical has peaked as I see Dye exports still going on an uptrend and China’s pollution control measures still in place. What am I missing? Is the market reluctant to price this higher worrying that China might build non-polluting dye capacities soon? I am looking solely for the negatives that I am certain I am overlooking. I haven’t done deep research on this sector before so looking for pointers. Thanks!

Disc: Started building a position today

3 Likes

Is there a possibility of Dystar taking this case to the any higher court like Court of Appeals or international tribunals etc? If so, it would prolong the legal dispute.

I found out following when it comes to appealing the judgment from Singapore International Commercial Court

Quote

Appellate Body

A judgment of SICC may be appealed to the Court of Appeal. However, the parties while contracting may limit or completely exclude/waive such right of appeal. The judges of the Court of Appeal would also come from the SICC Panel which would include International Judges.

Unquote

2 Likes

Exactly what are we missing, a mere 4-5 PE for

a company with such growth. Has there been any issues with regards to management quality? If someone could enlighten on the management front would be helpful.

1 Like

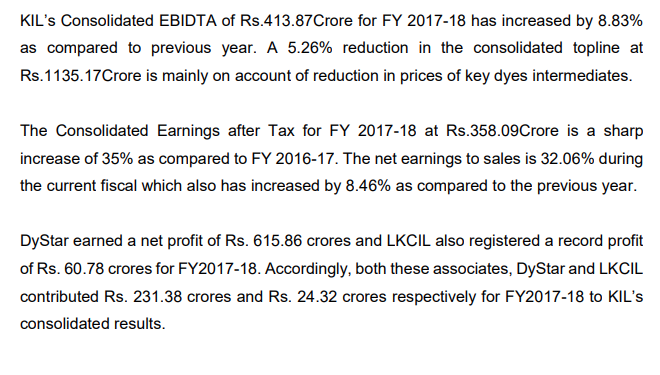

The P/E comes to 4.99 based on consolidated profit, if standalone profit is only considered then P/E comes to 17.4, which is not cheap. Consolidated profit can not be used any longer as Dystar is not going to be be part of Kiri industries as per the case outcome. But I agree the money from Dystar need to be valued as well. The exact amount and date when Kiri industries is going to get is not decided. Promoters haven’t come up with explanation what they will be doing with the amount, so with all uncertainties, current valuation seems to be in balance.Also regarding Kiri industries undervaluation there was an article covered by Moneylife link to it :https://www.moneylife.in/article/kiri-industries-highly-undervalued-but-why/50216.html

Disclosure: Not invested, waiting for q1 result to decide.

Can’t read the article, need to be subscriber. What’s the reasoning given in the article?

Also a few questions if somebody could address them would be helpful.

1)Everyone has spoken about valuations but I haven’t seen any discussion on the management quality so if someone can address that.

2)what is the PE for Kiri if we remove dystar revenue and profits, since this will be the business they are left with.

3)Kiri will receive an amount from stake sale in Dystar of 38%, apart from this amount is there any receivable of 700crs to Kiri for its share in the profits(this was mentioned in one of, above posts).

Moneylife is a paid service. You should not posting such articles here as per the forum guidelines.

Regards,

Suhag

I haven’t posted moneylife article neither I have summarized the article, it’s the link to article which any one can read if they have the subscription, so don’t see any issue on posting a link.

1 Like

-

It was Kiri’s management that insisted on acquiring DyeStar and turned it around. If things would’ve gone as planned, Kiri would have been the majority holder, not the Chinese partner. Also, they’ve reduced the debt, capitalized on Chinese supply and more. I don’t see any negative about the current management. Maybe not proactive towards shareholders but nothing wrong either.

-

Kiri didn’t receive anything from DyeStar until now. They have only included an estimated amount in their balance sheet as receivable I believe (could be wrong but accounting standards dont allow recognition of this revenue).

-

No, but the 38% stake will be adjusted for the value of patents that the Chinese partner exploited + any other funds they dwindled. So calculating the value of the minority stake is not A * B%. The valuation will get more clarity once the parties conduct the Conference as recommended by the court.

2 Likes

So you’re saying that all the revenue and profit numbers that are being posted by Kiri will continue even after stake sale in Dystar?

I thought Kiri includes revenue of Dystar in their statements proportionatily.

1 Like

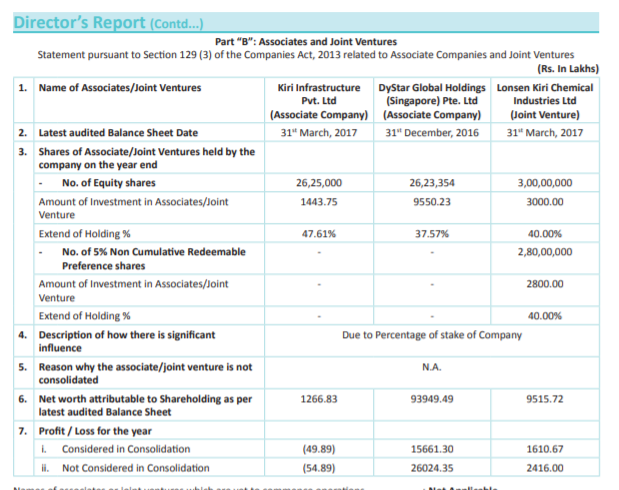

You’re right. Here’s the relevant extract from 2016-17 AR